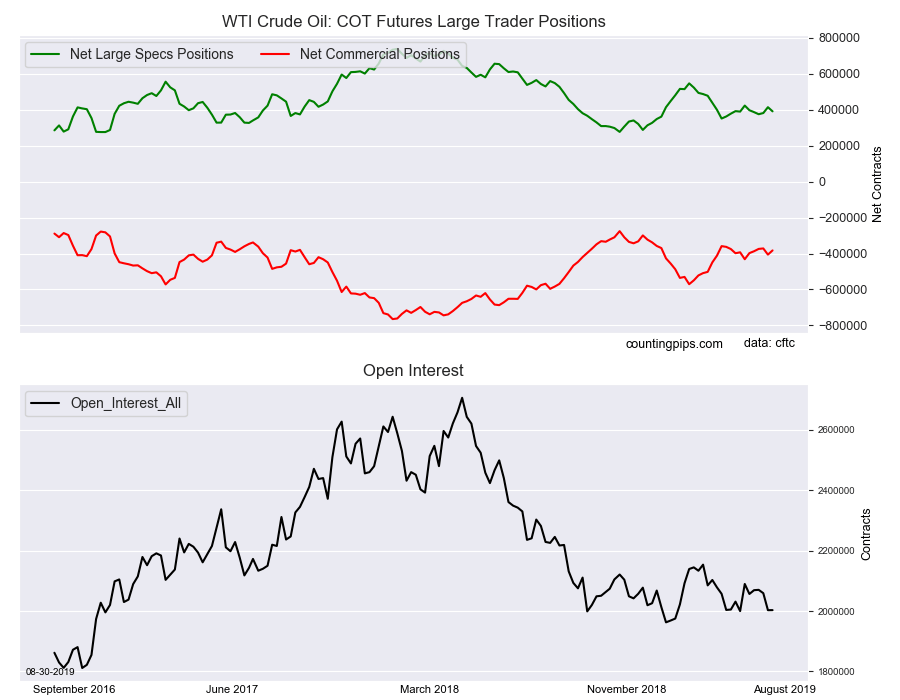

Large energy speculators cut back on their bullish net positions in the WTI Crude Oil futures markets this week, according to the latest Commitment of Traders (COT) data released by the Commodity Futures Trading Commission (CFTC) on Friday.

The non-commercial futures contracts of WTI Crude Oil futures, traded by large speculators and hedge funds, totaled a net position of 391,650 contracts in the data reported through Tuesday August 27th. This was a weekly lowering of -22,985 net contracts from the previous week which had a total of 414,635 net contracts.

The week’s net position was the result of the gross bullish position (longs) declining by -15,504 contracts (to a weekly total of 513,465 contracts) while the gross bearish position (shorts) advanced by 7,481 contracts for the week (to a total of 121,815 contracts).

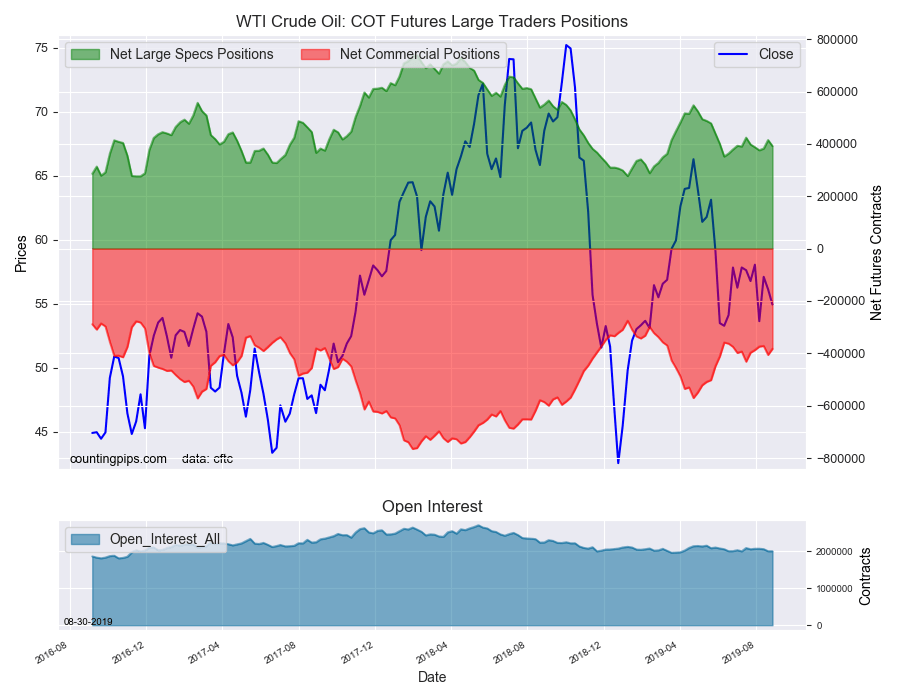

Large crude oil speculators reduced their bullish bets for the first time in three weeks through Tuesday. Previously speculators had been pushing their bets higher by a total of +38,994 contracts over those previous two weeks. The current standing is back under the +400,000 net contract level this week for fifth time out of the past six weeks.

WTI Crude Oil Commercial Positions:

The commercial traders position, hedgers or traders engaged in buying and selling for business purposes, totaled a net position of -382,445 contracts on the week. This was a weekly gain of 23,368 contracts from the total net of -405,813 contracts reported the previous week.

WTI Crude Oil Futures:

Over the same weekly reporting time-frame, from Tuesday to Tuesday, the WTI Crude Oil Futures (Front Month) closed at approximately $54.93 which was a fall of $-1.20 from the previous close of $56.13, according to unofficial market data.

*COT Report: The COT data, released weekly to the public each Friday, is updated through the most recent Tuesday (data is 3 days old) and shows a quick view of how large speculators or non-commercials (for-profit traders) as well as the commercial traders (hedgers & traders for business purposes) were positioned in the futures markets.

The CFTC categorizes trader positions according to commercial hedgers (traders who use futures contracts for hedging as part of the business), non-commercials (large traders who speculate to realize trading profits) and nonreportable traders (usually small traders/speculators).

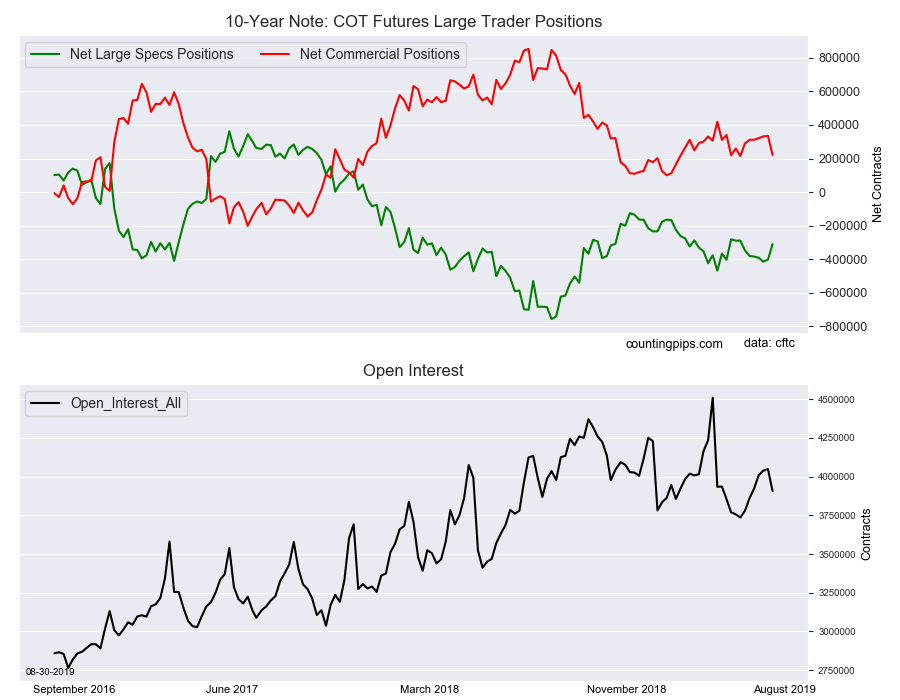

Large bond speculators cut back on their bearish net positions in the 10-Year Note futures markets this week, according to the latest Commitment of Traders (COT) data released by the Commodity Futures Trading Commission (CFTC) on Friday.

The non-commercial futures contracts of 10-Year Note futures, traded by large speculators and hedge funds, totaled a net position of -309,904 contracts in the data reported through Tuesday August 27th. This was a weekly change of 91,900 net contracts from the previous week which had a total of -401,804 net contracts.

The week’s net position was the result of the gross bullish position (longs) lowering by -16,513 contracts (to a weekly total of 603,950 contracts) while the gross bearish position (shorts) fell strongly by -108,413 contracts for the week (to a total of 913,854 contracts).

The large speculators sharply reduced their bearish bets by the most in nine weeks this week and marked a second straight weekly decrease. Previously, speculators had raised their bearish positions for five straight weeks and for seven out of the previous nine weeks.

Speculators have been consistently bearish this market this year despite the strong rally in 10-year bond market. This week’s pullback, however, brings the current position to the least bearish level since July 9th.

10-Year Note Commercial Positions:

The commercial traders position, hedgers or traders engaged in buying and selling for business purposes, totaled a net position of 221,938 contracts on the week. This was a weekly loss of -113,061 contracts from the total net of 334,999 contracts reported the previous week.

10-Year Note Futures:

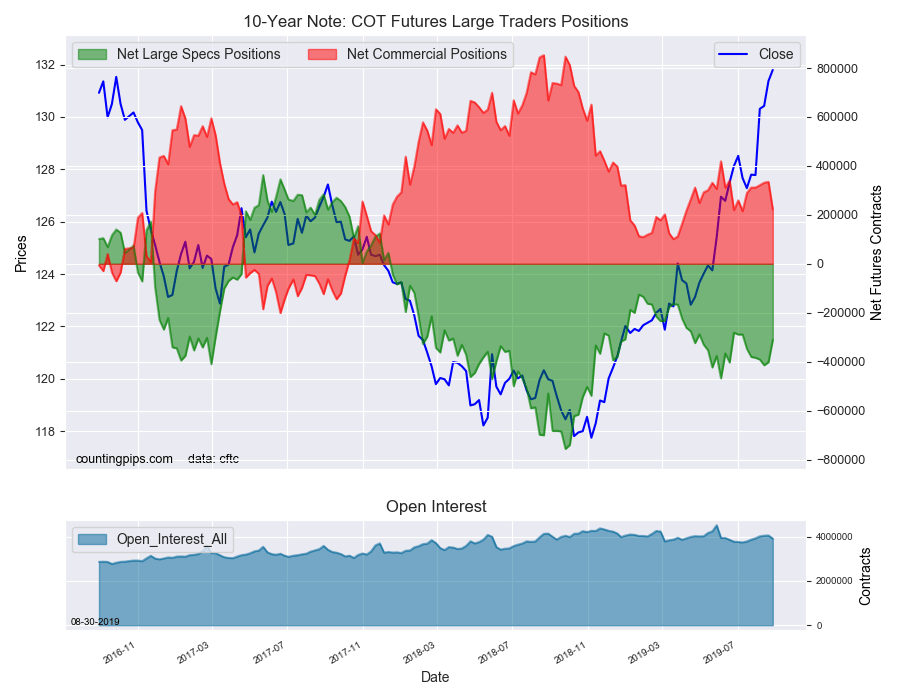

Over the same weekly reporting time-frame, from Tuesday to Tuesday, the 10-Year Note Futures (Front Month) closed at approximately $131.79 which was a rise of $0.42 from the previous close of $131.37, according to unofficial market data.

*COT Report: The COT data, released weekly to the public each Friday, is updated through the most recent Tuesday (data is 3 days old) and shows a quick view of how large speculators or non-commercials (for-profit traders) as well as the commercial traders (hedgers & traders for business purposes) were positioned in the futures markets.

The CFTC categorizes trader positions according to commercial hedgers (traders who use futures contracts for hedging as part of the business), non-commercials (large traders who speculate to realize trading profits) and nonreportable traders (usually small traders/speculators).

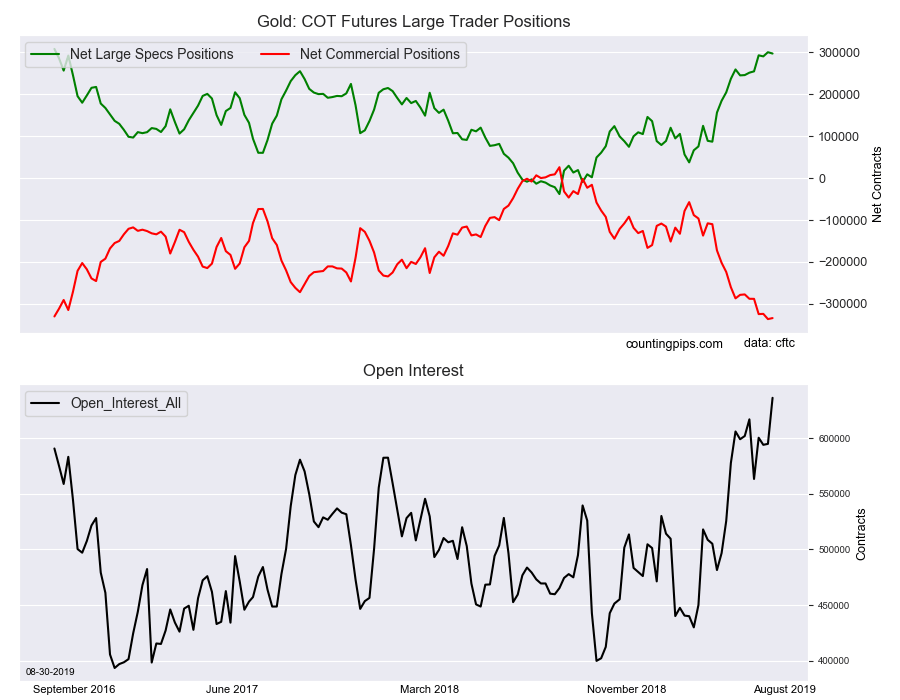

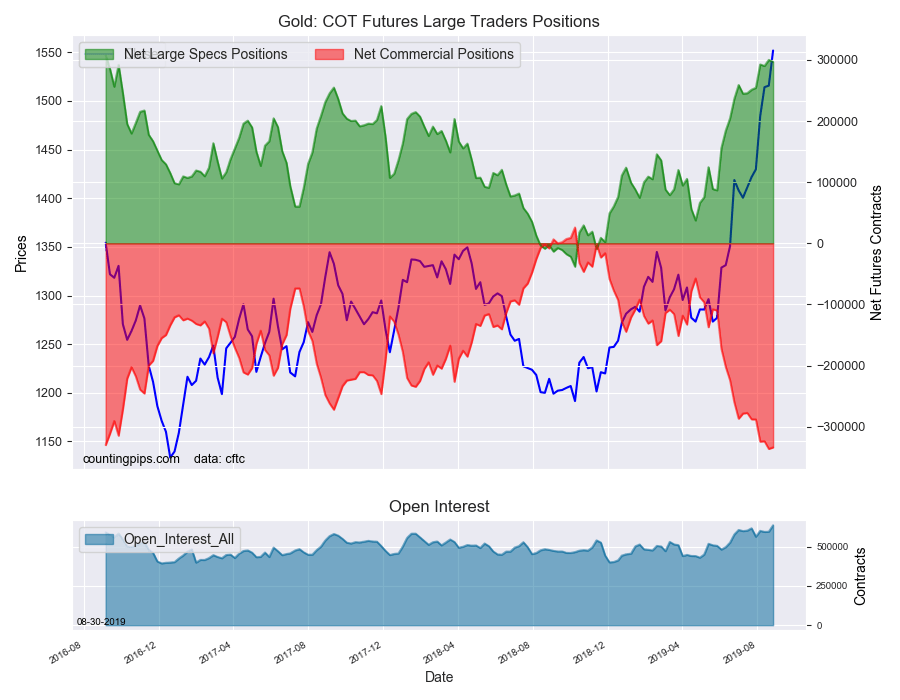

Large precious metals speculators decreased their existing bullish net positions in the Gold futures markets this week, according to the latest Commitment of Traders (COT) data released by the Commodity Futures Trading Commission (CFTC) on Friday.

The non-commercial futures contracts of Gold futures, traded by large speculators and hedge funds, totaled a net position of 296,838 contracts in the data reported through Tuesday August 27th. This was a weekly decline of -3,155 net contracts from the previous week which had a total of 299,993 net contracts.

The week’s net position was the result of the gross bullish position (longs) advancing by 10,315 contracts (to a weekly total of 362,609 contracts) while the gross bearish position (shorts) increased by a larger amount of 13,470 contracts for the week (to a total of 65,771 contracts).

Gold positions edged very slightly lower for the second time in the past three weeks. Despite the pull back, speculator sentiment has been on fire for gold over the past few months as bullish bets have risen by a total of +210,150 contracts just since June 4th. The current bullish standing (+296,838 contracts) remains very close to the +300,000 net contract level which has not been reached since September 6th of 2016 (a span of 155 weeks).

Gold Commercial Positions:

The commercial traders position, hedgers or traders engaged in buying and selling for business purposes, totaled a net position of -333,806 contracts on the week. This was a weekly gain of 2,444 contracts from the total net of -336,250 contracts reported the previous week.

Gold Futures:

Over the same weekly reporting time-frame, from Tuesday to Tuesday, the Gold Futures (Front Month) closed at approximately $1551.80 which was an increase of $36.10 from the previous close of $1515.70, according to unofficial market data.

*COT Report: The COT data, released weekly to the public each Friday, is updated through the most recent Tuesday (data is 3 days old) and shows a quick view of how large speculators or non-commercials (for-profit traders) as well as the commercial traders (hedgers & traders for business purposes) were positioned in the futures markets.

The CFTC categorizes trader positions according to commercial hedgers (traders who use futures contracts for hedging as part of the business), non-commercials (large traders who speculate to realize trading profits) and nonreportable traders (usually small traders/speculators).

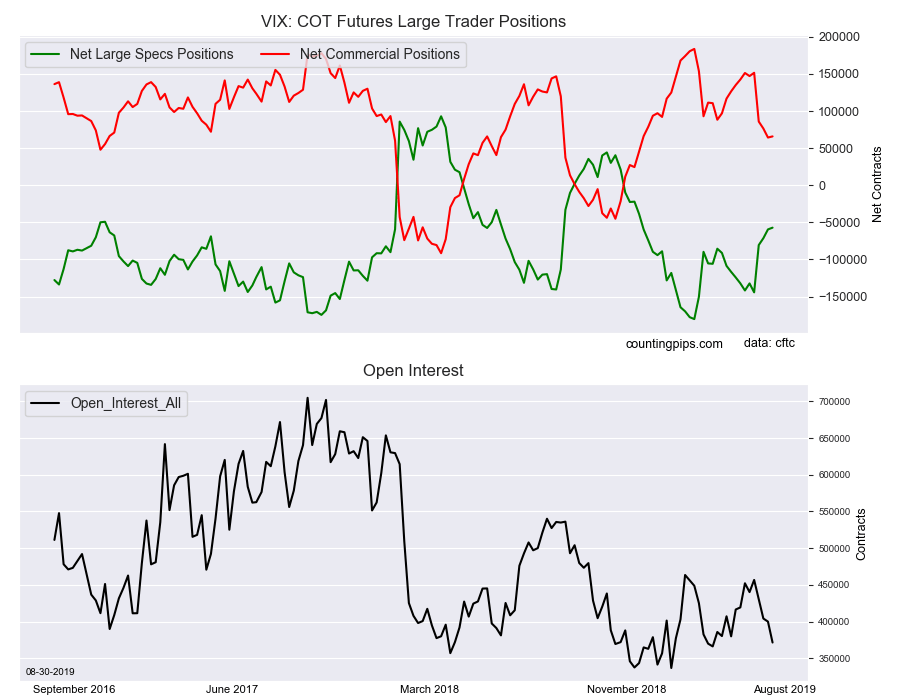

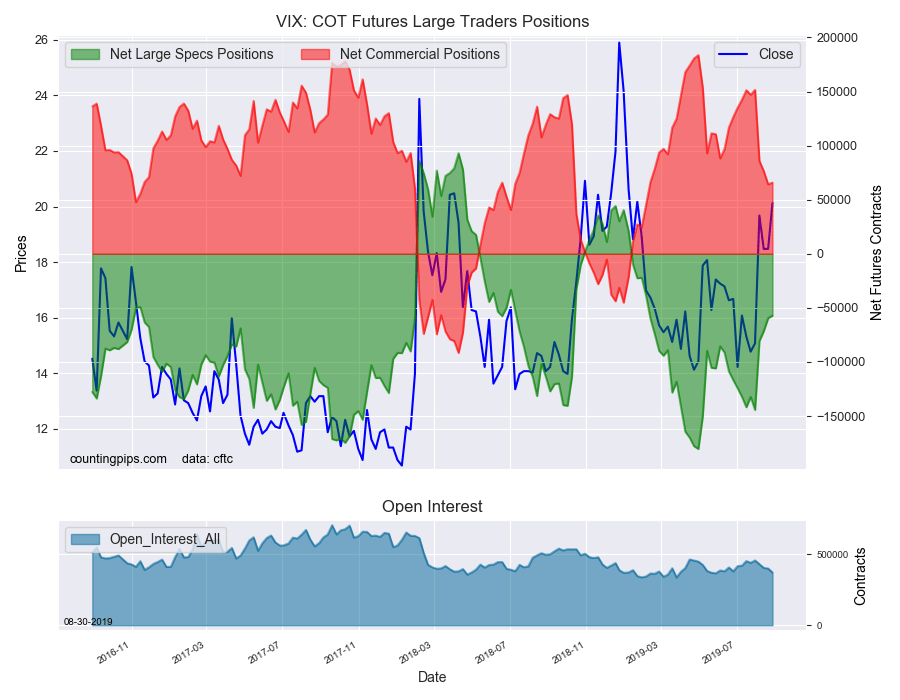

Large volatility speculators decreased their bearish net positions in the VIX futures markets this week, according to the latest Commitment of Traders (COT) data released by the Commodity Futures Trading Commission (CFTC) on Friday.

The non-commercial futures contracts of VIX futures, traded by large speculators and hedge funds, totaled a net position of -57,153 contracts in the data reported through Tuesday August 27th. This was a weekly change of 2,345 net contracts from the previous week which had a total of -59,498 net contracts.

The week’s net position was the result of the gross bullish position (longs) declining by -9,132 contracts (to a weekly total of 116,331 contracts) while the gross bearish position (shorts) dropped by a larger amount of -11,477 contracts for the week (to a total of 173,484 contracts).

Large VIX speculators cut back on their bearish bets for a fourth consecutive week this week. Speculators had been consistently raising their bearish bets since the beginning of the year as net bearish positions rose in twenty-three out of thirty weeks through July 30th (before the last 4 weeks cool off).

The current speculator standing is now at the least bearish level since February 5th of this year as speculators have become more cautious in the past month.

VIX Commercial Positions:

The commercial traders position, hedgers or traders engaged in buying and selling for business purposes, totaled a net position of 65,848 contracts on the week. This was a weekly rise of 1,554 contracts from the total net of 64,294 contracts reported the previous week.

VIX Futures:

Over the same weekly reporting time-frame, from Tuesday to Tuesday, the VIX Futures (Front Month) closed at approximately $20.12 which was an advance of $1.65 from the previous close of $18.47, according to unofficial market data.

*COT Report: The COT data, released weekly to the public each Friday, is updated through the most recent Tuesday (data is 3 days old) and shows a quick view of how large speculators or non-commercials (for-profit traders) as well as the commercial traders (hedgers & traders for business purposes) were positioned in the futures markets.

The CFTC categorizes trader positions according to commercial hedgers (traders who use futures contracts for hedging as part of the business), non-commercials (large traders who speculate to realize trading profits) and nonreportable traders (usually small traders/speculators).

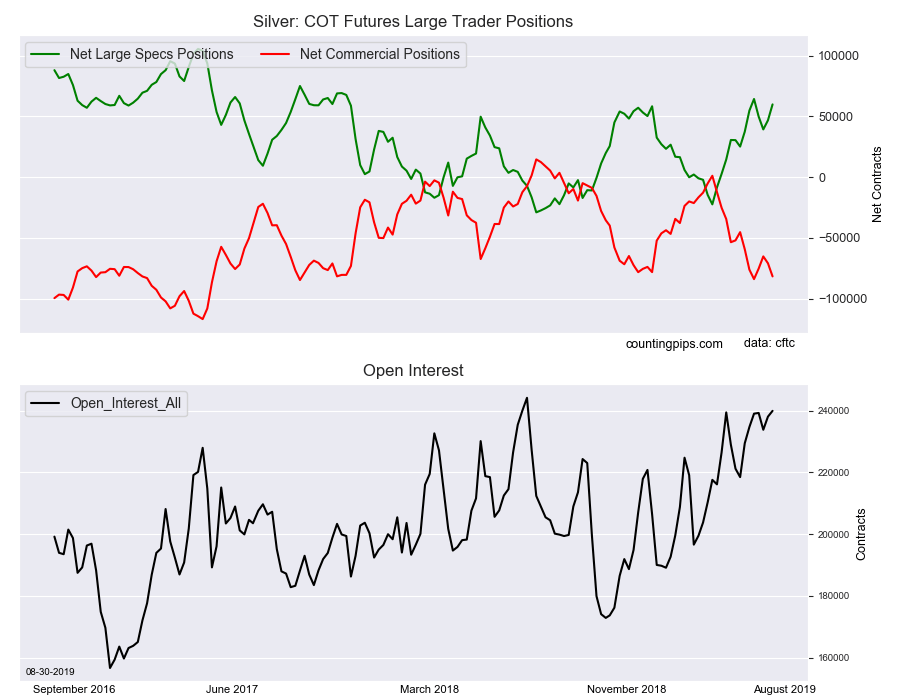

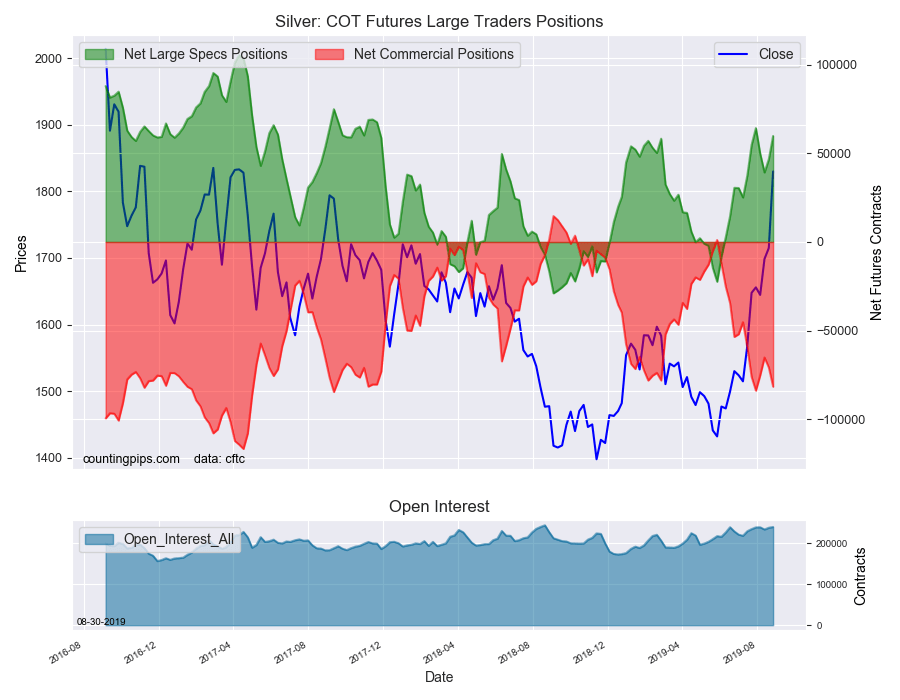

Large precious metals speculators once again raised their bullish net positions in the Silver futures markets this week, according to the latest Commitment of Traders (COT) data released by the Commodity Futures Trading Commission (CFTC) on Friday.

The non-commercial futures contracts of Silver futures, traded by large speculators and hedge funds, totaled a net position of 59,852 contracts in the data reported through Tuesday August 27th. This was a weekly gain of 13,138 net contracts from the previous week which had a total of 46,714 net contracts.

The week’s net position was the result of the gross bullish position (longs) growing by 7,501 contracts (to a weekly total of 103,488 contracts) while the gross bearish position (shorts) lowering by -5,637 contracts for the week (to a total of 43,636 contracts).

Silver speculator bets rose strongly for a second consecutive week after having fallen in the previous two weeks. Speculative positions have now gained in nine out of the past thirteen weeks as sentiment continues to remain strong. The silver net position has advanced from a total of -8,443 contracts on June 4th to a total of +59,852 contracts this week which is a gain of +68,295 contracts over the past thirteen weeks.

Silver Commercial Positions:

The commercial traders position, hedgers or traders engaged in buying and selling for business purposes, totaled a net position of -81,681 contracts on the week. This was a weekly fall of -10,818 contracts from the total net of -70,863 contracts reported the previous week.

Silver Futures:

Over the same weekly reporting time-frame, from Tuesday to Tuesday, the Silver Futures (Front Month) closed at approximately $1829.80 which was an uptick of $115.00 from the previous close of $1714.80, according to unofficial market data.

*COT Report: The COT data, released weekly to the public each Friday, is updated through the most recent Tuesday (data is 3 days old) and shows a quick view of how large speculators or non-commercials (for-profit traders) as well as the commercial traders (hedgers & traders for business purposes) were positioned in the futures markets.

The CFTC categorizes trader positions according to commercial hedgers (traders who use futures contracts for hedging as part of the business), non-commercials (large traders who speculate to realize trading profits) and nonreportable traders (usually small traders/speculators).

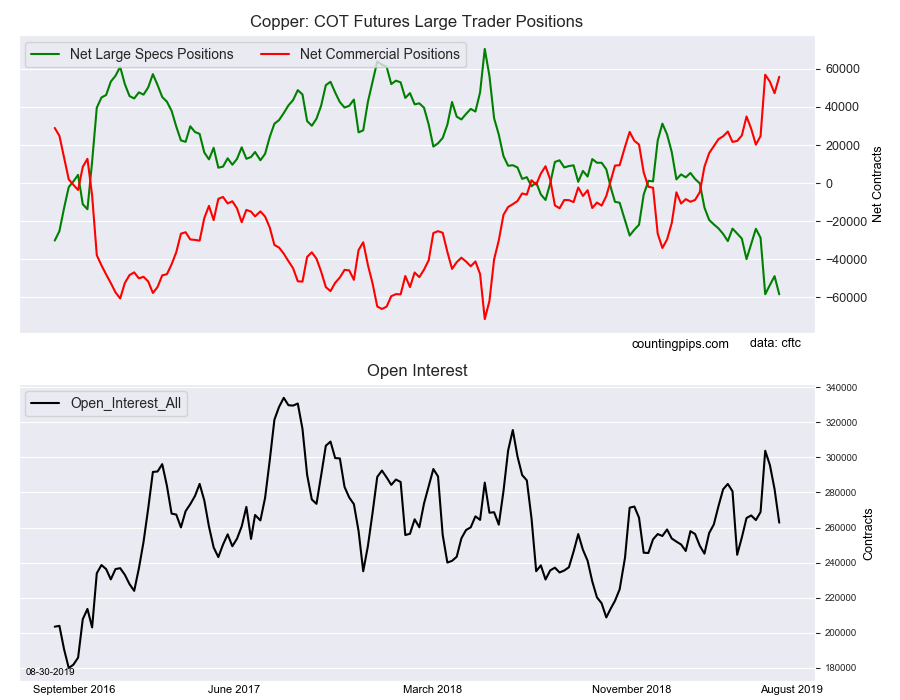

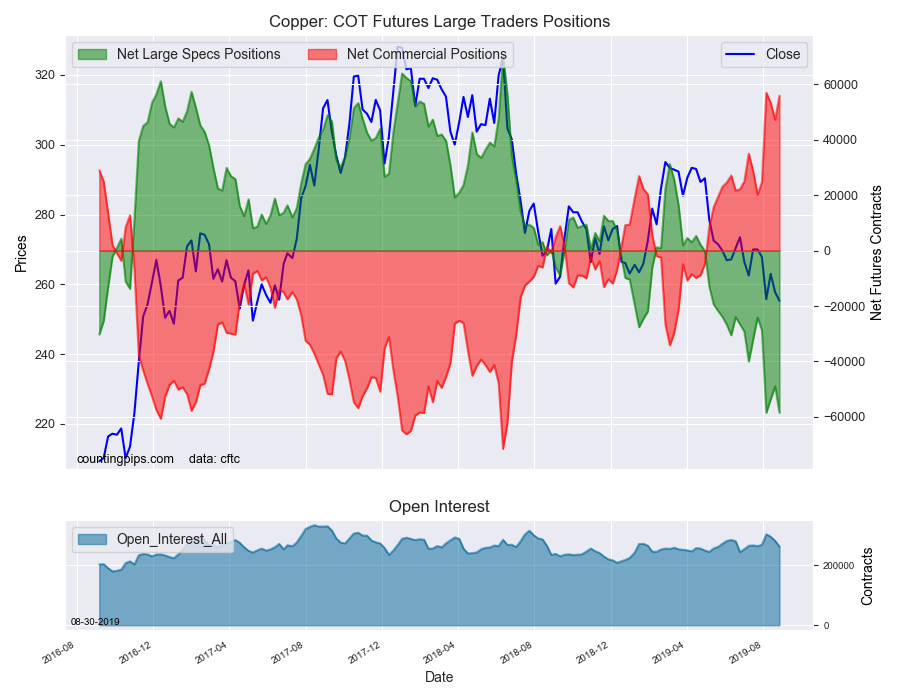

Large precious metals speculators sharply boosted their bearish net positions in the Copper futures markets this week, according to the latest Commitment of Traders (COT) data released by the Commodity Futures Trading Commission (CFTC) on Friday.

The non-commercial futures contracts of Copper futures, traded by large speculators and hedge funds, totaled a net position of -58,480 contracts in the data reported through Tuesday August 27th. This was a weekly change of -9,535 net contracts from the previous week which had a total of -48,945 net contracts.

The week’s net position was the result of the gross bullish position (longs) sliding by -2,694 contracts (to a weekly total of 72,795 contracts) while the gross bearish position (shorts) rose by 6,841 contracts for the week (to a total of 131,275 contracts).

The copper speculative position is now at the most bearish level on record, just surpassing the previous record that was recorded three weeks ago. Following the previous record high on August 6th, speculators had reduced their bearish positions for two straight weeks before this week’s resurgence. Copper speculator positions have now been in bearish territory for eighteen straight weeks dating back to April 30th.

Copper Commercial Positions:

The commercial traders position, hedgers or traders engaged in buying and selling for business purposes, totaled a net position of 55,885 contracts on the week. This was a weekly advance of 8,648 contracts from the total net of 47,237 contracts reported the previous week.

Copper Futures:

Over the same weekly reporting time-frame, from Tuesday to Tuesday, the Copper Futures (Front Month) closed at approximately $255.30 which was a decrease of $-2.50 from the previous close of $257.80, according to unofficial market data.

*COT Report: The COT data, released weekly to the public each Friday, is updated through the most recent Tuesday (data is 3 days old) and shows a quick view of how large speculators or non-commercials (for-profit traders) as well as the commercial traders (hedgers & traders for business purposes) were positioned in the futures markets.

The CFTC categorizes trader positions according to commercial hedgers (traders who use futures contracts for hedging as part of the business), non-commercials (large traders who speculate to realize trading profits) and nonreportable traders (usually small traders/speculators).

Welcome to this week’s Market Wrap Podcast, I’m Mike Gleason.

Coming up Gerald Celente, top trends forecaster and publisher of the Trends Journal joins me for an explosive conversation on the state of the markets, gold, the upcoming presidential election, and why he believes the next recession will be one for the ages. Gerald also reveals what you should be doing right now to prepare for it. So, don’t miss my conversation with Gerald Celente, coming up after this week’s market update.

As markets close out the month of August, precious metals investors are scoring some big summer gains. The standout performer has been silver, surging over 15% during the month.

On Thursday, the white metal spiked to nearly $18.70 an ounce before pulling back in afternoon trading. As of this Friday recording, silver prices come in $18.43, up 5.4% for the week.

Silver has vastly outperformed gold since early July. That’s a healthy sign for the broader precious metals bull market. The gold to silver ratio is coming down from a quarter century high and likely has much further to fall as the bull market progresses.

For the week, gold is essentially unchanged to bring spot prices to $1,530 an ounce.

And speaking of ratios, the gold-to-platinum ratio is also coming down from extreme heights as the automotive metal finally kicks into gear. This week, the platinum market broke out to a new high for the year. It is up a whopping 8.8% since last Friday’s close to trade at $937 per ounce.

And finally, palladium is surging here today and is up 5.3% now for the week to trade at $1,543.

Looking ahead to next month, metals investors will await a near-certain rate cut from the Federal Reserve. There is an outside chance the Fed could cut by 50 basis points instead of the usual 25.

Everybody knows that President Donald Trump favors larger scale reductions in interest rates. He wants to stimulate the economy and stock market ahead of next year’s election.

Fed policymakers are supposed to stay out of politics and make their decisions based solely on the economic data before them. But it would be naïve to believe they don’t harbor political biases.

They have been under relentless attack by President Trump. They see his attacks as posing a threat to the so-called “independence” of the Federal Reserve. They may even fear that if he is re-elected he will threaten the existence of the Fed as an institution.

Could the Federal Reserve be deliberately withholding stimulus to try to get Trump defeated? It may sound like just another baseless conspiracy theory. But, in fact, there is some basis for believing Fed officials have the motive and opportunity to sabotage the Trump economy.

Don’t take it from me. Take it from former New York Fed President Bill Dudley. On Wednesday, he penned an article for Bloomberg titled “The Fed Shouldn’t Enable Donald Trump.” Dudley argued that the central bank should refuse to support the economy while the Trump administration is waging trade wars. Instead, he claimed, the Fed should force President Trump to “bear the risks – including the risk of losing the next election.” Dudley went so far as to suggest that “the election itself falls within the Fed’s purview.”

Those are things anyone who has held a senior position at the Fed simply doesn’t say – at least not publicly. Former U.S. Treasury Secretary Larry Summers, a Democrat, was aghast.

CNBC Anchor: Former New York Fed president, Bill Dudley, is arguing that the Fed should not cut interest rates further in response to president Trump’s trade war with China. Strong’s sharp criticism from foreign Treasury Secretary Larry Summers, who called it quote, “The worst case of Trump derangement syndrome in the financial world.”

Larry Summers: For a trusted former official of the Fed, whose thinking is inevitably going to be tied to the Fed, to recommend that they raise interest rates so as to subvert the economy and influence a presidential election is grossly irresponsible, and is an abuse of the privilege of being a former Fed official. So, it was the taking of the economic dialogue out of the realm of economics, and the putting it in a realm of politics and suggesting that the Fed was there, and was acting politically, or might act politically, that was empowering the Fed’s critics, and I thought, was profoundly disloyal.

Pay no attention to that disloyal man behind the curtain, Summers tells us. The powers that be don’t want the public to believe there’s an anti-Trump resistance movement operating inside the Federal Reserve.

But if there were, and the people leading it were smart, they too would denounce Dudley. They would swear up and down in their public pronouncements that they aren’t motivated by politics.

If we had a sound monetary system based on an objective standard of value with interest rates determined by the free market, then there would be no possibility of election meddling by central bankers. The opinions of Bill Dudley and Jerome Powell would carry no more weight than those of any number of other economic commentators.

Perhaps President Trump will come to regret not more fully embracing sound money principles. On the 2016 campaign trail, he railed against Barack Obama’s Fed chair Janet Yellen for being politically motivated.

Once he became President, Trump became singularly focused on low interest rates. He appointed Fed insider Jerome Powell to chairman. He thought Powell was his guy. But Powell soon revealed that his true loyalty was to the Fed itself – an institution that arguably wields more power than any government agency.

President Trump now faces an uphill battle for re-election. He can expect no help from Democrats in Congress or the Fed in stimulating the economy.

His Treasury Department does have some stimulus cards of its own to play, such as administrative changes that would lower capital gains tax burdens.

Treasury Secretary Steven Mnuchin said he is also considering the issuance of 50-year and 100-year Treasury bonds. It would be an opportune time to do so. Long-term bonds are being gobbled up with record-low yields attached to them. The global appetite for sovereign debt has proven to be insatiable even as yields sink below zero in many countries.

Eventually, it will all end badly for bondholders as inflation eats away at the real value of the bonds and yields rise to more sensible levels. In the meantime, savvy investors are diversifying into precious metals as a more promising alternative to negative real yields on paper. And as a hedge against the risk of a Fed-induced recession and stock market crash ahead of the 2020 election.

Well now, without further delay, let’s get right to this week’s exclusive interview.

Mike Gleason: It is my privilege now to welcome back, the one and the only, Gerald Celente, publisher of the renowned Trends Journal. Mr. Celente is a frequent guest here on the Money Metals Podcast and is perhaps the most well-known trends forecaster in the world, and it’s always a real joy to have him on. Gerald, thanks for the time again today and welcome back.

Gerald Celente: Yeah, thanks for having me on, Mike.

Mike Gleason: Well, Gerald, there’s a lot to talk about today, but I’d like to discuss first the trend of people losing faith in our government institutions. Frankly, they have lots of good reasons for that. The Jeffrey Epstein affair, for example, revealed something which has been going on for a long time – there are two justice systems, one which prosecutes the crimes of regular people and another which protects the well-connected from accountability. The Federal Reserve, which is always marketed as a benevolent organization, is actually the protector and defender of the crooked Wall Street banks, which it owns.

These are of course, just two examples of corruption and failure. Yet, while confidence may be fading, we aren’t yet seeing here in the States the sort of social unrest that is happening in Hong Kong and with the yellow vest movement in France for instance, we view the lack of violence here as a good thing obviously, but there has been very little progress toward draining the swamp. At this point, do you see a coherent reform movement in America. And what are you expecting, do things still have to get worse before people wake up and start making them better?

Gerald Celente: Yeah, they’re going to have to get worse. And it’s not a lack of violence. I mean, when you’re looking at the protests in France with the yellow vests, and the movement in Hong Kong, it’s very few people, and that’s who gets the media. Let’s take a look at Hong Kong for a second. This is a place of what? About 7.4 million people. And last Sunday, what? 1.7 million people came out, 1.4 million people. I mean that’s a lot of people. Oh and it was raining, so they’re out there in umbrellas. In America, you have, people put on… One day they put on pink pussy hats and it’s a big deal, a million people show up around the country. We don’t have the fight here in America. Same thing with the yellow vests.

And I want to make another one very clear that people forgot about. Battle of Seattle, back in the late 1990s, hundreds of thousands of people protested against the meeting going on because of the World Trade Organization, under slick Willie Clinton. And when you mentioned that Einstein, what’s his name? Eisenberg. Is it Eisenberg?

Mike Gleason: Epstein.

Gerald Celente: Epstein. Epstein. Epstein, Eisenberg. Iceberg, Greenberg. What’s the difference anyway? Bill Clinton was what, on his plane, what? 26 times or something. This is the Bill Clinton were talking about.

They were protesting the World Trade Organization. A couple of people, agents, provocateurs dressed in black, nobody can see their face, started smashing windows. That’s what got all the press, not the hundreds of thousands of peaceful demonstrators. So, going back to America, the fight is gone here. There’s no fight. A matter of fact, you’re not allowed to fight. We need a no bullying zone. And can you imagine this, they’re making it up, you need a no bullying zone. “Don’t fight. Don’t learn how to fight. We’ll protect you.” Yeah, the militarized police state of America.

You learn how to fight. What are you kidding? And by the way, I used to have my own close combat school for many years, and been at it for many, many years and that’s why I speak out. I’m not here to take orders from anybody. I don’t give them, I don’t take them. In America, you don’t have the fight anymore. That’s why you’re not seeing a new movement going on. As you pointed out, the polls show what some 70% of the people disgusted with the system, 71%. And you don’t see any backlash. “I’m voting Democrat, I’m voting Republican.” Grow up. The Democraps and the Repulsivecans. So, no, you don’t see it here. And I don’t think it’s going to happen until the greatest depression hits. And that’s going to be as we see it now in 2021, and because when people lose everything and they have nothing left to lose, they lose it. And that’s what it’s going to take.

Mike Gleason: Here we are again, volatility is creeping back into the stock market. The trade dispute with China has been a big driver in the markets over the past year and a half. It’s currently weighing on the equity markets again. There’s lots of talk about the inversion in bond yields signaling that a recession is on the way. What are you expecting in the financial markets between now and year end? Are we going to have a bloody fourth quarter like we did last year, Gerald?

Gerald Celente: It’s hard to tell, but what we’re saying at the Trends Journal is that the markets have peaked, and the downward pressure is great. You mentioned the trade war, the markets hit new highs this year. They’ve been hitting new highs since Trump got elected. We were the first people, by the way, two weeks after he got elected in 2016, to call the Trump rally. And I was the first to say it was over. And I believe it’s over now. And so it could crash. There’s a lot of wildcards out there and there’s no wilder card than the Trump card. But I make this point because this trade war talk has been going on continually. It’s not a trade war that’s slowing down the global economy. It’s the monetary methadone that the Federal Reserve and the other central banksters injected into the system, just to enrich the 1%. The facts are there.

When you look at the sanctions that Trump has put on China, the last report that I saw was that it effected 0.6% of China’s GDP. That’s nothing. Take a look what’s going on in India. Oh yeah, their NIFTY 50, their equity market, it’s down over 10%. Oh, I wonder why? It’s not a trade war with them. They’re not doing a lot of trade with China. No, the global economy is slowing down. Same thing with Argentina. How about Brazil? They keep using this excuse of the trade war with China, when it’s much bigger than that. It’s a global slow down. The monetary methadone only keeps the bull running, the addicted bull running for so long, so it’s ready to crash. But again, what I learned over the years after it crashes, they come up with a new drug, and they artificially pump it up again. Will they have enough to do it this time, is the question.

Mike Gleason: Expanding the point here. We’ve seen volatility come and go in the equity markets, but there are some real differences which make us wonder if this time it’s different. Bond yields are inverted, which is an indication that investors want to park some capital indefinitely in longer term bonds, and they want that badly enough that they’re willing to accept returns even lower than for short term bonds. And precious metals prices are starting to move. Both are a sign that investors are looking for safety. Are the wheels getting ready to come off the equity markets for real this time?

Gerald Celente: Yes, they’re getting ready, absolutely. But again, they’re going to do everything they can to pump it up. You’re looking at the United States, they only could lower interest rates 2%. When the last recession hit, the interest rates could come down 5.5%. You go to Europe, they’re in negative rates already, minus 0.4. They’re going to bring it down to minus 0.5, and dump another $60 billion a month into corporate and government bond buybacks. So, going back to the inverted yield curve, I mean who in their right mind would buy a 30 year bond, a German bond, and get less back in 30 years than what you bought it for? And not a lot of people. But yes, a lot of people, the German bond, they had to buy $2 billion worth when they launched that last week, and there was 16 to $17 trillion in negative yield global bonds now that had been sold.

So, that’s why people are going into gold. They are looking for the safe haven asset and gold is the ultimate one. And just for the record, I call this identically on the point where gold was going to go for the last six years. I said it had a break over the $1,450 mark for it to gain strength. And on June 6th, we sent a Trend Alert out to our subscribers, when gold was $200 cheaper than it is now, $1,332 an ounce. And the headline of the Trend Alert was the Gold Bull Run. Gold which solidified over the $1,325 mark, and our next breakout from that was $1,385. It flew past that and flew past $1,450, so the downside risk we see now for gold is at the very worst about $1,390.

Mike Gleason: Yeah, stealing my thunder, I was actually about to lay all that out. We spoke last in May, and you said the same thing that you’ve been saying for the last several years, $1,385, we need to take that out. Then we go to $1,450, and then once we get $1,450 taken out, we make a runs towards $2,000. Are you still sticking with that, and thinking that we’re going to see gold up towards that $2,000 level at some point?

Gerald Celente: Absolutely, absolutely. And you can see the strength of it. And even when the markets go up, gold isn’t going down much. And again, there will be something to bring it down. It always is, whether it’s real or manipulated. Just like the markets for example. You go back to the night before Christmas, and Dow is having its worst December since the Great Depression, and the worst two weeks since the panic of ’08. And all of a sudden, our Treasury Secretary gets on the phone with six banksters, Mnuchin calls up, and when the markets reopened on the day after Christmas, all of a sudden, the next two days the markets are up over a thousand points. You think it’s the Plunge Protection Team? Go back a few weeks ago. Same thing happened. Dow down 800 points, Trump gets on the phone, calls the banksters, next day up, up goes to the market. So, when I talk about where’s gold going, there’s going to be a lot of pressure from the banksters to keep gold prices low. But again, on the other hand, the central banksters also bought more gold in 2018 than they have in 50 years.

Mike Gleason: Yeah, it’s definitely very interesting to kind of watch them say one thing and do another. The central banks are buying gold hand over fist.

We’re just now a year out from the 2020 election and things appear to be taking shape in terms of who will be running against Trump in next year’s general election. For now anyway, the Democrat front runners appear to be Elizabeth Warren, Bernie Sanders and Joe Biden. Now two of those three in that group are known socialists, which is obviously a very interesting commentary on where we are with respect to the political preferences of many Americans these days. So, handicap the field here for us, Gerald… do you still see whoever the Dems do nominate performing well in those key battleground states that will be so important in determining the winner next November? Let’s hear your comments on the Presidential Reality Show as you like to call it.

Gerald Celente: When Clinton was running for president in 1992, in their campaign offices, they used to have a sign to keep the people focused on the important issue, “it’s the economy, stupid.” And that’s all it’s going to be about. We just heard former New York Fed president encourage the Federal Reserve not to lower interest rates, so Trump wouldn’t win. And that’s what it’s going to come down to. It’s going to be determined on how the economy is doing.

And at this point, by the way, we see Trump getting reelected. And Elizabeth Warren is going to have a very difficult time, as will Bernie Sanders in the swing states. Biden has a better shot in the swing states, particularly Pennsylvania. As we see it now, it’s Trump. But again, it’s way too early and it’s going to depend… “It’s the economy, stupid.” By the way, one of the things, two things, we also see that Trump is going to do to help support his reelection. We believe there will be a peace treaty with North Korea and Afghanistan by then.

Mike Gleason: Yeah. Interesting. We’ll be watching for that there. There is kind of this talk about maybe how the deep state will try to torpedo Trump a little bit, and let the market correct before the election next year, which as you said, the economy is really what drives a lot of voters’ decisions. Do you have any credence to that type of theory, that the deep state could be out to a sink Trump there a year from now?

Gerald Celente: If they do… and he’s part of the deep state. I mean, look at a lot of things that he’s doing. They’re all in the club. “It’s one big club and we’re not in it,” as George Carlin said. But no, they’re not going to sink the markets. They don’t want to lose money. They wouldn’t do anything like that at all. They want to keep that money flow going.

Mike Gleason: Well finally, Gerald, as we begin to wrap up, give us any final thoughts on anything that we may not have touched on, on either the financial front or in the geopolitical realm. Give us a sense of some of the stories or the trends you’re going to be following most closely as we head into this final stretch of the year?

Gerald Celente: Well, what’s going on, very important to watch is what’s going on in Hong Kong, and what’s going on with India, and now ripping up the 1947 agreement and saying that Kashmir is theirs, they have no autonomy. And now you have two nuclear states, Pakistan and India in conflict. Because Pakistan says, “No, no, Kashmir is ours,” or whatever they keep fighting about and have been fighting about. And some 50,000 people were killed over the last 10 years over a dispute like that.

When all else fails, they take you to war. And right now the Indian economy’s failing. The NIFTY 50 is down over 10% since Modi got reelected, and he won by a landslide. The people’s minds are off the issues. You look at car sales, you look at their GDP, worst GDP in five years, in the first quarter. Car sales plummeting. (It) has nothing to do again with trade wars, the whole thing is going down.

When all else fails, they take you to war. Same thing with Israel. Netanyahu won the election. Cannot put together a coalition government because he wants part of the coalition government to write in a statement that he will not be able to be prosecuted on charges he’s being brought up on. So, now what’s happening? In the last few days, boom, a drone attack in Lebanon. Airstrikes, missile strikes in Iraq, where Iranian troops were, and in Syria.

Again, we have to watch these areas. They’re very important because if it explodes in the Middle East against Iran, it’s the beginning of World War III. You’re going to see oil prices skyrocket to over a hundred dollars a barrel, that’ll crash economies and it will crash equity markets. And by the way, the reason that Trump did not retaliate against Iran when they shot down that very sophisticated, $100 million, $200 million drone, was because it would have been Pearl Harbor in the Straits of Hormuz. Iran is not Libya. They’re not Syria, they’re not Iraq. They’re not Afghanistan. They’re the Persians. They’re not going anywhere. And they have the sophistication to fight back.

So, if war breaks out against any of those countries, against Iran, that’s a big one to watch. We’re urging people to stay tuned to follow the trends that are going to make a big difference, particularly going into the greatest depression.

Mike Gleason: Well excellent, we’ll leave it there. Before we go, let’s have you tell people about how they can follow the tremendous Trends Journal information, and anything else that you want them to know about you and your organization. You guys are multimedia. You do lots of things to keep people informed. Let’s hear about that.

Gerald Celente: Well, yeah, we have the magazine. We’re going to be making a new announcement. It’s a monthly, it’s going to increase from that in September. We do Trends in the News broadcasts, three nights a week. We send out Trend Alerts, weekly and more. And it’s the only magazine in the world where you’re going to read history before it happens. You tune into the news, you find out what happened. You tune into Trends in the News, you find out what’s going to happen. And again, we’re urging people to prepare now so they could prevail and prosper when the greatest depression hits. They could go to TrendsJournal.com and read history before it happens.

Mike Gleason: Well thanks again, Mr. Celente. We always enjoy the conversation and I can’t wait to get your comments the next time around, and I wish you the best. Take care and have a great weekend.

Gerald Celente: You too. Thank you.

Mike Gleason: Well, that will do it for this week. Thanks, again to Gerald Celente, publisher of the renowned Trends Journal. For more information, the website again is TrendsJournal.com, be sure to check that out.

And check back here next Friday for our next Weekly Market Wrap Podcast. Until then, this has been Mike Gleason with Money Metals Exchange. Thanks for listening and have a great weekend everybody.

Mike Gleason: And don’t forget to check back here next Friday for our next Weekly Market Wrap Podcast. Until then, this has been Mike Gleason with Money Metals Exchange, thanks for listening and have a great weekend, everybody.

The Money Metals News Service provides market news and crisp commentary for investors following the precious metals markets.

By Jameel Ahmad, Global Head of Currency Strategy and Market Research at FXTM, ForexTime

The Euro has broke below 1.10 against the Dollar, representing the lowest level in the EURUSD since May 2017 in a move that we have been anticipating since the beginning of the second half of 2019.

As written here between the threats of tariffs being imposed on Europe from the United States, fears of an upcoming recession to strike the world economy, the German economy already contracting in Q2 plus a host of other reasons there has been no motive to consider becoming a long-term purchaser of the Euro.

And if you are, this is likely because of the understanding that the patience of President Trump towards a weaker Euro, and in turn, a stronger USD has worn thin (check out his twitter for more). Essentially the President is calling for a weaker Dollar and if the Greenback turns weaker, this promotes strength in the Euro.

In the meantime and while the EURUSD stays below 1.10, expect for expectations to rise substantially that the Euro can decline all the way towards 1.06 over the coming months for as long as the pair does not cross back above 1.10 (invalidating this outlook)

Near-term opportunities include exploring bearish positions on both the EURGBP and EURJPY, where the EURJPY is down more than 100 pips today at time of writing.

Disclaimer: The content in this article comprises personal opinions and should not be construed as containing personal and/or other investment advice and/or an offer of and/or solicitation for any transactions in financial instruments and/or a guarantee and/or prediction of future performance. ForexTime (FXTM), its affiliates, agents, directors, officers or employees do not guarantee the accuracy, validity, timeliness or completeness, of any information or data made available and assume no liability as to any loss arising from any investment based on the same.

Risk off remains the ‘base case’ of my FX thinking.

Volatility is the highest it’s been in 2019 as the sporadic nature of geo-politics coupled with a backdrop of a slowing global economy has created a perfect FX risk caldron and one that has us looking at XAU and crosses that are long JPY.

EURJPY remains the cross of choice as risk off coupled with the ECB’s September policy changes should see the cross continuing its 45-degree slide to a consensus view of ¥111.00 by year end.

What is also apparent in this market is there are trades that one should try to avoid despite how ‘appealing’ they might seem. In my opinion Cable is a prime example Brexit is creating a very difficult and unknown lever in GBP/USD which has only amplified since the election of populist Prime Minster Boris Johnson.

His gambit to suspend Parliament by the end of this week to force the House to find a Brexit deal is creating a constitutional crisis of the highest order. It has been attacked by all side of the Parliament and his own Speaker has made it clear how ‘unprecedented’ this move is. In short – this event is as negative as negative could be.

Yet, when you look at the trading in Cable this event has actually seen the pair appreciated, not what one would expect.

If you look at some of the Fibonacci retracement levels there is clear support sub-$1.215. Again, if an event like the Prime Minster dissolving Parliament and pushing a no Brexit deal to the front of the cue of possibilities doesn’t cause GBP/USD fall then what will?

Thus, the clear take out of the global set up currently is choose your opportunity. There is enough volatility to find trades that provide returns, but it also means you need to find trades that have some structure based in either technical or fundamental or both to have confidence event risk wont wipe the trade out.

Over the weekend and on Monday we have a couple of important economic events coming out of the Far East.

The Purchasing Managers’ Index (PMI) is a survey of company executives, asking how they see the current business situation and how they expect it to be in the next three months. This helps us understand what their purchasing trends (among other things) will be.

In the case of China, as the world’s largest importer of commodities, what its companies are thinking is especially relevant to commodity currencies. Australia, New Zealand and Japan all have China as their largest trade partner. The current economic doldrums in Japan are largely attributed to the drop in demand for machinery and cars from China. So, even if you don’t trade the CNY, what happens in China is likely relevant to a large number of currencies.

The Upcoming Surveys

We get the official Manufacturing and Non-manufacturing PMIs early on Sunday while the markets are closed. This means that we don’t get a reaction to the data until later in the day. Then we get the private Caixin survey for manufacturing on Monday. Both have a habit of moving the markets since while they measure the same thing, the difference in the methodology of the survey provides extra insight for the market.

The NBS PMI survey has considered a smaller number of businesses, with a focus on large, state-owned enterprises. They tend to be less agile in responding to market changes. And, often, their policies reflect the government’s interests more than even their own profitability.

The Caixin survey goes out to a much larger number of companies, with a preponderance of small, privately held companies. They are said to be more domestically oriented, and able to handle market distortions. We could explain the difference between the two surveys by the effects of the trade war.

What We Are Expecting

Projections indicate that the official NBS Manufacturing PMI will return further into contraction at 49.2. This is compared to 49.7 in the previous survey. Last month, there was a surprise improvement. So a drop of a few decimals is not likely to spook the market. Also, it’s still in the range where it could be seen as a technical contraction.

Expectations are for the NBS Non-Manufacturing PMI to remain comfortably in expansion territory at 54.3. This would also be an improvement over the 53.7 reported in the prior month. A result like this would be something of a relief to analysts since this indicator has taken a bit of a dive since March. This could be because of the effects of the trade war domestically, as well as a broader impact on the Chinese consumer.

On Monday, we can also expect the Caixin Manufacturing PMI to slip further into contraction at 49.6. This would be down from the borderline 49.9 in the prior month. Smaller companies have seemingly been better at weathering the effects of the trade war. A return to growth (if, again, just technically by a decimal point or two) would be positive for the markets. However, it would not necessarily be a blow-out.

The Effects

There has been a lot of uncertainty about trade talks over the survey period. This is likely to depress the results, even though over the last week or so, sentiment has somewhat improved. Trade talks have stalled and resumed so many times since the tensions began, that uncertainty is clouding all optimism.

In the meantime, the Chinese government hasn’t been as forthcoming with stimulus. But, also during this period, the yuan broke below the psychologically important 7.0 level. This level would facilitate exports and support profits for Chinese firms. On the other hand, that diminishes purchasing capacity for imports and is not good news for commodity currencies.