The US dollar does not change a lot relative to the basket of major currencies. The dollar index (#DX) closed yesterday’s trading session with a slight increase (+0.09%). Investors expect additional drivers. Now, financial market participants hope to receive at least some signals regarding progress in US-China trade relations, as well as the Brexit process.

The Euro has been declining after the release of weak data on economic activity in Germany and the Eurozone. Thus, German manufacturing PMI counted to 41.4 in September and was worse than the expected value of 44.0. Markit composite PMI in the Eurozone counted to 50.4 in September instead of 51.9. Investors are concerned about the development of the recession in the Eurozone economy. Additional support for the US currency was provided by the US Manufacturing PMI released yesterday, which reached 51.0 in September instead of 49.6.

The “black gold” prices have been declining. Currently, futures for the WTI crude oil are testing the $58.10 mark per barrel. At 23:30, API weekly crude oil stock will be published.

Market Indicators

Yesterday, there was a variety of trends in the US stock markets: #SPY (-0.02%), #DIA (+ 0.04%), #QQQ (-0.16%).

The 10-year US government bonds yield has moved away from local lows. At the moment, the indicator is at the level of 1.71-1.72%.

The Economic News Feed for 24.09.2019:

– German IFO business climate index at 11:00 (GMT+3:00);

– US consumer confidence Index at 17:00 (GMT+3:00).

Boris Johnson was dealt a heavy blow on Tuesday after the Supreme Court ruled his suspension of Parliament ‘unlawful, void and to no effect’.

Appetite towards the Pound instantly brightened on this news as the currency jumped over 50 pips against the Dollar to trade above 1.2485. However, gains were later surrendered as investors refocused on the bigger picture and what it meant for Brexit. Given how opposition leaders are already calling for the prime minister to resign, political uncertainty is set to mount as the clock ticks down.

Fundamentally, the Supreme Court ruling does not change anything as the United Kingdom is still on course to leave the European Union on October 31st without a deal. What happens after today remains open to question and certainly compounds to the uncertainty over Brexit. Does the Prime minister have a plan B? Will he resign? Will there be a general election?

This sentiment is being reflected in the British Pound which is trading around 1.2440 as of writing. Given how the currency remains extremely sensitive to Brexit related developments, market players should fasten their seatbelts and prepare for more volatility ahead of the Brexit deadline.

One key question on the mind of many investors after today’s ruling is when MPs will return to Parliament.

In regards to the technical picture, the GBPUSD remains bullish on the 4 hourly timeframe with support found around 1.2400. An intraday breakout above 1.2460 should encourage a move towards 1.2485 and 1.2500.

Zooming out on the weekly charts, the trend remains bearish. However, a solid week close above 1.2500 will open the doors towards 1.2700.

Disclaimer: The content in this article comprises personal opinions and should not be construed as containing personal and/or other investment advice and/or an offer of and/or solicitation for any transactions in financial instruments and/or a guarantee and/or prediction of future performance. ForexTime (FXTM), its affiliates, agents, directors, officers or employees do not guarantee the accuracy, validity, timeliness or completeness, of any information or data made available and assume no liability as to any loss arising from any investment based on the same.

On Monday the 23rd of September, trading on the EURUSD pair closed down. The pair keeps trading within the range formed on the 12th of September following the ECB meeting and Mario Draghi’s press conference. The bulls managed to recover from an intraday drop to 1.0966. The euro was boosted by mixed US data, restoring the pair to 1.10.

The US manufacturing PMI exceeded expectations, while the services PMI fell short. This is the first time in 9 years that the service industry has seen a drop in activity. US10Y bond yields took a dive, taking the US dollar index with it.

Day’s news (GMT+3):

11:00 Germany: IFO – business climate (Sep), IFO – current assessment (Sep), IFO – expectations (Sep).

11:30 UK: public sector net borrowing (Aug).

16:00 US: S&P/Case-Shiller home price indices (Jul).

17:00 US: consumer confidence, Richmond Fed manufacturing index (Sep).

Current situation:

At the time of writing, the euro is trading at 1.0990. Judging by the formation drawn from the 1.1073 top, it seems that the pair is set to continue downwards. Following a sharp drop to 1.0966, it’s possible that the pair will continue to consolidate below the balance line.

If the bears don’t hit fresh lows, the pair could at least return to 1.0966 if the euro crosses decline. In our forecast, we’re predicting a drop to 1.0970. Even a pullback to 1.0975 will fulfill the conditions for a correction.

ECB President Draghi said yesterday that there are no signs of either recovery or decline in the Eurozone’s manufacturing sector. This could have a negative effect on the wider economy. Draghi’s remarks are likely to hold the bulls back this week.

If the price moves as forecasted, we could get a double base with a target of 1.1040.

Asian markets are pushing tepidly higher after the S&P closed flat, as investors are being fed more woeful signs about the global economy. Germany’s September manufacturing PMI fell further into contraction territory, while France’s industrial sector recorded scant expansion during the same month.

The world’s economic growth momentum has stuttered amid heightened global trade tensions, prompting investors to keep safe haven assets at elevated levels. Gold remains near its 2-week high and is trading above $1520, the Japanese Yen is holding above the key 107.5 level versus the US Dollar, while yields on 10-year Treasuries are testing the 1.70 support level. Any sudden spike in geopolitical or trade tensions, along with a rapid deterioration in the global economy’s projected path forward, is expected to return safe haven assets to 2019 highs.

Euro pushed below psychological 1.10 mark against Dollar amid pronounced EU economic woes

The Euro is still trading below the psychological 1.10 level versus the US Dollar, following the dismal PMI figures out of Germany and France. With EURUSD having fallen by more than four percent so far in 2019, there’s scant reason to think that the bloc’s currency can see a rebound anytime soon.

Even with the support measures rolled out by the European Central Bank as well as the limited fiscal stimulus in Germany, investors are not entirely convinced that will be enough to offset the challenges that beset the EU economy. Until there is a meaningful resolution to both US-China trade tensions as well as the Brexit impasse, the EU economy is expected to remain mired in its current dismal state. Such a dreary economic outlook for the EU will only serve to keep the Euro pinned down around the 1.10 mark.

Dollar remains steadfast despite market expectations for one more Fed rate cut in 2019

The Dollar index (DXY) is still trading above the 98.6 level, even as Federal Reserve Bank of St. Louis President James Bullard continues to telegraph the potential need for more “insurance” interest rate cuts. The Fed Funds Futures currently price in one more 25-basis point cut in October, before leaving the benchmark interest rate unchanged through January.

Despite the dovish bias shown by the Federal Reserve, the Dollar remains buoyed by the US economy’s outperformance relative to its major, developed peers. The Greenback’s safe haven status is fueling its resilience, amid the swirling concerns over the deteriorating state of the global economy.

Disclaimer: The content in this article comprises personal opinions and should not be construed as containing personal and/or other investment advice and/or an offer of and/or solicitation for any transactions in financial instruments and/or a guarantee and/or prediction of future performance. ForexTime (FXTM), its affiliates, agents, directors, officers or employees do not guarantee the accuracy, validity, timeliness or completeness, of any information or data made available and assume no liability as to any loss arising from any investment based on the same.

Paraguay’s central bank lowered its policy rate for the fifth time this year, noting the downward risk in the growth prospects for the global economy, negative domestic growth and the absence of inflationary pressure.

The Central Bank of Paraguay (BCP) cut its policy rate by another 25 basis points to 4.0 percent and has now cut it by 125 basis points this year following cuts in February, March, July and August.

BCP said its monetary policy committee, CEOMA, was unanimous in its decision.

In South America the economic scenario remains complex, especially with regard to Argentina, and domestic economic activity and demand has improved marginally but cumulative growth rates remain negative.

Headline and underlying inflation also remain in the lower zone of BCP’s target range and according to the bank’s forecasts, there will not be any inflationary pressures in coming months.

“In this context, the Committee considers it appropriate to adopt an even more accommodative monetary policy profile that is compatible with the convergence of inflation to the annual 4.0% target in the forecast horizon,” BCP said.

Paraguay’s headline inflation rate declined to 2.8 percent in August from 3.1 percent in July while gross domestic product contracted by 2.0 percent year-on-year in the first quarter of this year after growth of 1.0 percent in the fourth quarter of last year.

BCP has forecast 2019 growth of 1.5 percent, down from 3.7 percent in 2018.

Dollar strengthening continues on strong Markit data

US stocks ended marginally lower on Monday underpinned by positive data and news Chinese importers bought about 10 boatloads of US soybeans totaling 600,000 tons. The S&P 500 finished 0.01% lower at 2991.77. Dow Jones industrial added 0.1% to 26949.99. The Nasdaq composite fell 0.1% to 8112.46. The dollar strengthening was intact as Markit’s manufacturing index rose to a five-month high of 51 in August: the live dollar index data show the ICE US Dollar index, a measure of the dollar’s strength against a basket of six rival currencies, rose 0.2% to 98.62 and is higher currently. Stock index futures point to higher openings today.

CAC 40 posts biggest loss among European indexes

European stocks pulled back on Monday on disappointing euro-zone data. Both GBP/USD and EUR/USD kept sliding yesterday with Pound turning higher while euro still lower against dollar currently. The Stoxx Europe 600 index ended 0.8% lower as Markit reported manufacturing activity in the eurozone contracted more sharply in September, with manufacturing PMI falling to lowest reading in nearly seven years. The DAX 30 lost 1% to 12342.35 as Markit data showed Germany’s manufacturing PMI fell to 41.4 in September, its worst reading in a decade and composite PMI came in at 49.1 down from 51.7 in the previous month. France’s CAC 40 dropped 1.1% as expansion slowed in both manufacturing and services sectors. UK’s FTSE 100 slid 0.3% to 7326.08.

Hang Seng leads Asian indexes gains

Asian stock indices are recovering today. Nikkei rose 0.1% to 22098.84 as yen slide against the dollar resumed after Markit report factory activity slowed in Japan in August. Markets in China are rising as the governor of People’s Bank of China said PBOC won’t ease monetary policy as aggressively as other global central banks, as the economy is still performing within expectations: the Shanghai Composite Index is up 0.3% and Hong Kong’s Hang Seng Index is 0.4% higher. Australia’s All Ordinaries Index turned lower 0.01% despite Australian dollar slide against the greenback.

Brent futures prices are edging lower today after gains Monday on continued tensions in Middle East. Prices rose yesterday: November Brent crude closed 0.8% higher at $64.77 a barrel on Monday.

Note: This overview has an informative and tutorial character and is published for free. All the data, included in the overview, are received from public sources, recognized as more or less reliable. Moreover, there is no guarantee that the indicated information is full and precise. Overviews are not updated. The whole information in each overview, including opinion, indicators, charts and anything else, is provided only for familiarization purposes and is not financial advice or а recommendation. The whole text and its any part, as well as the charts cannot be considered as an offer to make a deal with any asset. IFC Markets and its employees under any circumstances are not liable for any action taken by someone else during or after reading the overview.

JPMorgan Chase and other bullion banks spent most of a decade screwing clients and investors who were naive enough to expect a fair shake in the precious metals futures markets. It was a solid racket.

Yet claims of price rigging were simply dismissed by financial journalists and regulators as conspiracy theory. The banks’ defenders were bolstered by a 5-year-long investigation by the compromised Commodity Futures Trading Commission (CFTC) which ended without a single banker being prosecuted.

Many goldbugs wondered if the racket would continue forever. Fortunately, much has changed over the past three years. Department of Justice prosecutors were able to secure a guilty plea from Deutsche Bank in late 2016.

The bank turned over 350,000 pages of documents and dozens of voice recordings as part of their agreement to cooperate with the investigation. The trove of evidence was a testament to the monumental failure of the CFTC. It shed light on a pervasive, long-running and well organized fraud which should have been difficult to overlook.

Despite CFTC assurances to the contrary, there are, in fact, plenty of bankers to prosecute.

The Justice Department has since secured guilty pleas from several traders working at Bank of America, JPMorgan Chase and elsewhere. Three more bankers were indicted in the past couple of weeks. And it appears investigators are a long way from done.

Bloomberg reported last week that prosecutors consider the trading operations at JPMorgan as a “conspiracy to conduct the affairs of an enterprise involved in interstate or foreign commerce through a pattern of racketeering activity.”

That language is purposely intended to evoke RICO, or Racketeer Influenced and Corrupt Organization, laws. JPMorgan may be prosecuted using the same laws designed to take down mobsters!

CFTC officials have not acknowledged the Commission’s abject failure to do its primary job. Many have pointed out how compromised the CFTC is. A remarkable number of CFTC officials wind up with lucrative jobs on Wall Street.

Now these conflicts of interest are on full display thanks to Craig Hemke with TF Metals Report.

Hemke, who has chronicled price rigging and the failure of the CFTC for years, made a remarkable connection after reading news coverage of Michael Nowak, JPMorgan’s head of global trading for precious metals and commodities.

Nowak is one of three former JPMorgan traders recently indicted.

Nowak’s attorney is David Meister. Meister led the CFTC’s enforcement division during its failed 5-year investigation of price rigging. He and his team managed somehow to overlook what we now know to be a massive criminal “enterprise” at the banks.

One week after concluding that investigation in 2013, Meister decided to leave for greener pastures. He joined the law firm Skadden, Arps, Slate, Meagher & Flom LLP and has been representing Wall Street firms and bankers ever since. He will now put his insider knowledge of regulations and the CFTC’s enforcement weaknesses to work defending Michael Nowak.

These people truly know no shame.

The Money Metals News Service provides market news and crisp commentary for investors following the precious metals markets.

Bill Powers of Mining Stock Education interviewed Greg Crowe, president and CEO of Silver One Resources, at the recent Beaver Creek Precious Metals Summit, and got an overview of the company’s two Nevada silver projects and their potential upside for investors.

Bill Powers: For about three years you’ve been the CEO of Silver One Resources Inc. (SVE:TSX.V; BRK1:FSE; SLVRF:OTC). You’re focused in Nevada. I didn’t really pay attention to this until you alerted me to the fact that Nevada is not the Gold State, it’s actually the Silver State. Talk to us a little about how Nevada is a good silver mining state.

Greg Crowe: Well, essentially, it’s a silver mining state because California stole the name the Golden State. But I must admit that in the early days, back in the mid-1800s, silver was the dominant mineral being mined in Nevada. And one of the reasons that Nevada entered the Union was because silver was used to pay down the Civil War debt. And it became known as the Silver State, [with] lots of silver production, big mines like Comstock. The one that we are about to finish acquiring, called Candelaria, which was the richest producing silver mine in Nevada. That changed in the 1980s actually, which was interesting, with the discovery of gold and Barrick Gold Corp.’s (ABX:TSX; GOLD:NYSE) big discovery up in northern Nevada. And since then everybody’s been looking for gold, gold, gold.

But we like silver. And we took that to our advantage. And we found a very good prospect, in addition to our Candelaria project, that we actually staked. And I can tell you a bit about that down the road too.

Bill Powers: Give us an overview of the Candelaria project and what is the upside here for investors?

Greg Crowe: Yeah, Candelaria is an interesting project. As I said, [it was] the richest producer from the mid-1800s up until mid-1900s and produced, on average, 1,250 grams per ton silver, from near surface high-grade veins. Then essentially it turned into an open-pit situation, mined up until 19971998. The last producer was Kinross Gold Corp. (K:TSX; KGC:NYSE). And the reason they shut the mine down was not because they exhausted the mine or the heaps. They only shut down because of the collapse of silver prices.

Silver prices touched, I think, $2.50 per ounce, and stayed under $5 per ounce until 2003 and thereafter. So in the meantime they shuttered the mine. Started reclamation and sold it off to Silver Standard Resources Inc. in 2001. Silver Standard did a big drill program, outlined a very sizeable resource, and moved forward with the idea of bringing it back in production. They couldn’t think about it in the $3 to $4 per ounce silver range, so they put it on the shelf. We came along in 2016 and structured a deal with Silver Standard (now SSR Mining Inc. [SSRM:NASDAQ]) to purchase a 100% interest with no royalties.

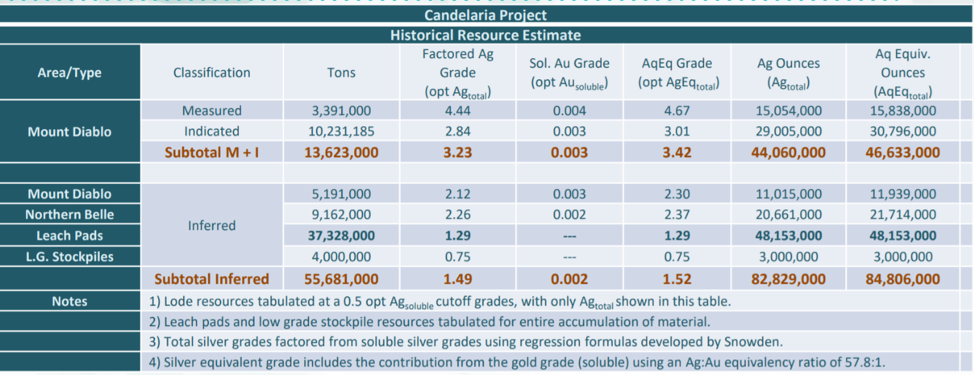

Bill Powers: So there’s a large historical resource there. What exactly is that historical resource, and also talk to us about the exploration upside at this project.

Greg Crowe: The historical resource, which we’re aiming to drill and become current, is Measured and Indicated resources of about 46 million ounces of silver, and additional Inferred resources of about 83 million ounces of silver. In the Inferred category, of that 83 million ounces, 48 million ounces still sits on the old leach pads. And we’ve done some good metallurgical testing. We’re continuing with that metallurgical testing with the [question]: Can we bring those heaps back into production? Our metallurgical testing will take another few months, but everything is looking very, very optimistic, particularly in this current upticking silver market.

Bill Powers: So you’d be looking at potentially a lower capex because there is a resource right there at surface. Best case scenario, when could that possibly come into production?

Greg Crowe: Best case scenario, it would be two years, and it all depends on what are the results of this metallurgical testing, which are going to take another few months, and then the permitting process. But one of the good things is because it was a disturbed site, and not completely 100% reclaimed, then it would, with a solid plan, of course, be much easier to facilitate permitting.

Bill Powers: And you have some solid financiers that have backed the project, including, most notably recently, Eric Sprott. How did that investment by Eric Sprott come about?

Greg Crowe: Well, in essence, the original investors in the company were affiliated with First Mining Finance, First Majestic Silver Corp. (FR:TSX; AG:NYSE; FMV:FSE) and Keith Neumeyer. Eric and Keith work together, and Eric became aware of Silver One. Interesting enough, when I met with Eric in Toronto, he showed me that Silver One was actually on his list for acquisition, and we announced a financing in June prior to the uptick in the silver markets. We put it out there that we would do a financing and try to raise about $2 million. Within three weeks, we had $5 million, with Eric Sprott coming in as our largest single shareholder.

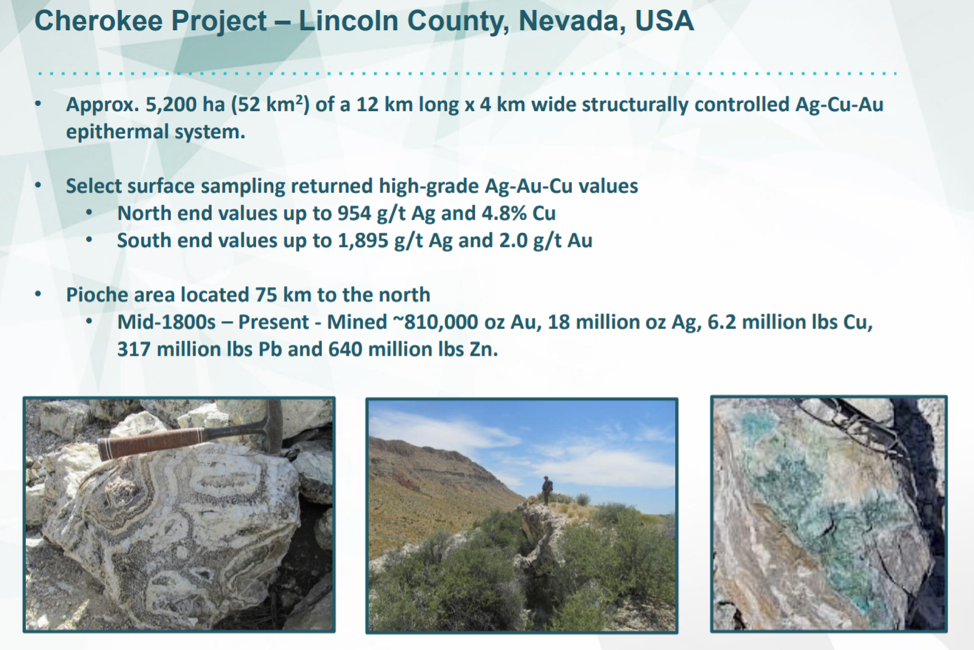

Bill Powers: So there’s a lot of fundamental value in the company in the historical resource of silver ounces in the ground. There’s exploration upside at the Candelaria project. And you’re also working at your Cherokee project. Talked to us about the exploration upside at the Cherokee project.

Greg Crowe: Yeah. Cherokee’s interesting. And it goes back to the premise that Nevada’s the Silver State. But most of the exploration has been focused on gold. There has been some silver exploration, but we saw a reference to an old historic mine that, in the 1800s, produced in the thousands of grams per ton silver. So we said we better go look at this. And we went and looked at it. And low and behold, [we found] beautiful, what are referred to as epithermal-style boiling point textures. Good indications of copper mineralization on surface, affiliated with some very sizable veins. [We] started walking the veins and we traced them for 12 kilometers, or nine miles, along strike and the ground was completely open.

So we staked the whole thing. And then we bought five of the patents. We now have 100% interest. [When we] started detailed sampling at the north end, where the old Cherokee mine is, we started getting values as high as a thousand grams per ton silver and 4.8% copper. In the south end, where the veins kind of come together, copper seems to disappear, but we’re starting to see two grams of gold creep in, and we’re still getting strong silver values. This time up to 1,800 grams per ton silver. This is on surface, select grabbed samples. The veins to our knowledge have never had a drill on them.

So our plan is to. . .we’re out there right now sampling and mapping, finding more and more veins, and then we’re going to be doing a property-wide airborne geophysical survey. With that information, we hope to be able to identify drill targets for the new year.

Bill Powers: What does the treasury and the burn rate of the company look like right now?

Greg Crowe: The treasury is about CA$4.2 to $4.5 million, in that range there. We do have these ongoing exploration programs, which will probably amount to about CA$2 million in total, but outside those, the average burn rate of the company is about CA$1.2 million per year.

Bill Powers: As we conclude, what final thoughts would you like to leave with the investors listening to us?

Greg Crowe: Well, [for] those of you who really do believe, shall we say, that we live in a somewhat unstable world, and in uncertainty economically, and you’re a believer in solid assets like gold and silverthen look at not only gold and silver, but gold and silver companies; especially those that have some something behind them and good financial backers behind them.

Bill Powers is the host of the Mining Stock Education podcast that interviews many of the top names in the natural resource sector and profiles quality mining investment opportunities. Powers is an avid resource investor with an entrepreneurial background in sales, management and small business development. His latest interviews can be found at MiningStockEducation.com.

Disclosure: 1) Bill Powers: I, or members of my immediate household or family, own shares of the following companies mentioned in this article: None. I personally am, or members of my immediate household or family are, paid by the following companies mentioned in this article: None. My company has a financial relationship with the following companies mentioned in this article: Silver One Resources is a Mining Stock Education advertiser. 2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. 3) Statements and opinions expressed are the opinions of the author and not of Streetwise Reports or its officers. The author is wholly responsible for the validity of the statements. The author was not paid by Streetwise Reports for this article. Streetwise Reports was not paid by the author to publish or syndicate this article. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy. 4) This article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases.

The content produced by Bill Powers and Mining Stock Education LLC is for informational purposes only and is not to be considered personal, legal or investment advice or a recommendation to buy or sell securities or any other product. It is based on opinions, public filings, current events, press releases and interviews but is not infallible. It may contain errors and we offer no inferred or explicit warranty as to the accuracy of the information presented. If personal advice is needed, consult a qualified legal, tax or investment professional. Do not base any investment decision on the information contained on MiningStockEducation.com, our podcast or our videos. We usually hold equity positions in and are compensated by the companies we feature and are therefore biased and hold an obvious conflict of interest. MiningStockEducation.com may provide website addresses or links to websites and we disclaim any responsibility for the content of any such other websites. The information you find on MiningStockEducation.com is to be used at your own risk. By reading MiningStockEducation.com, you agree to hold MiningStockEducation.com, its owner, associates, sponsors, affiliates, and partners harmless and to completely release them from any and all liabilities due to any and all losses, damages, or injuries (financial or otherwise) that may be incurred.

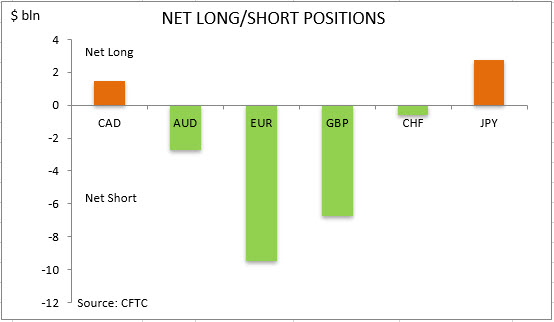

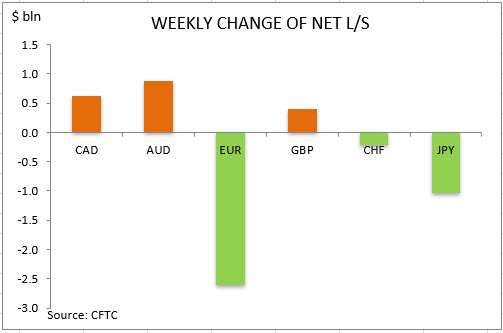

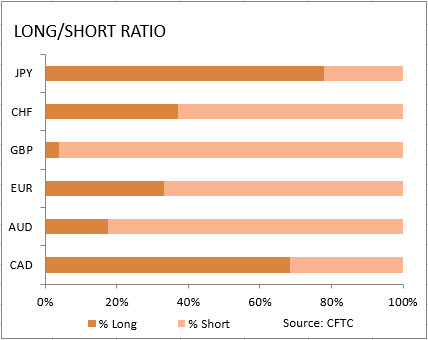

US dollar net long bets rose to $ 15.28 billion from $13.34 billion against the major currencies during the one week period, according to the report of the Commodity Futures Trading Commission (CFTC) covering data up to September 17 and released on Friday September 20. The dollar bullish bets rose as the Commerce Department reported US retail sales grew above expected 4.1% on-year in August, providing more support to the view no urgent stimulus is needed as US economy is strong.

Note: This overview has an informative and tutorial character and is published for free. All the data, included in the overview, are received from public sources, recognized as more or less reliable. Moreover, there is no guarantee that the indicated information is full and precise. Overviews are not updated. The whole information in each overview, including opinion, indicators, charts and anything else, is provided only for familiarization purposes and is not financial advice or а recommendation. The whole text and its any part, as well as the charts cannot be considered as an offer to make a deal with any asset. IFC Markets and its employees under any circumstances are not liable for any action taken by someone else during or after reading the overview.

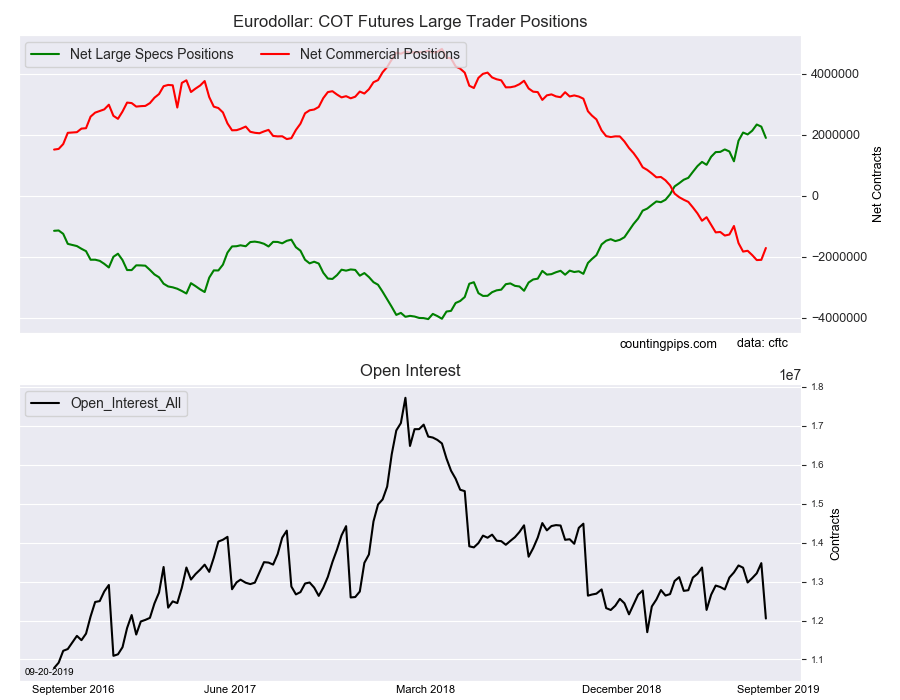

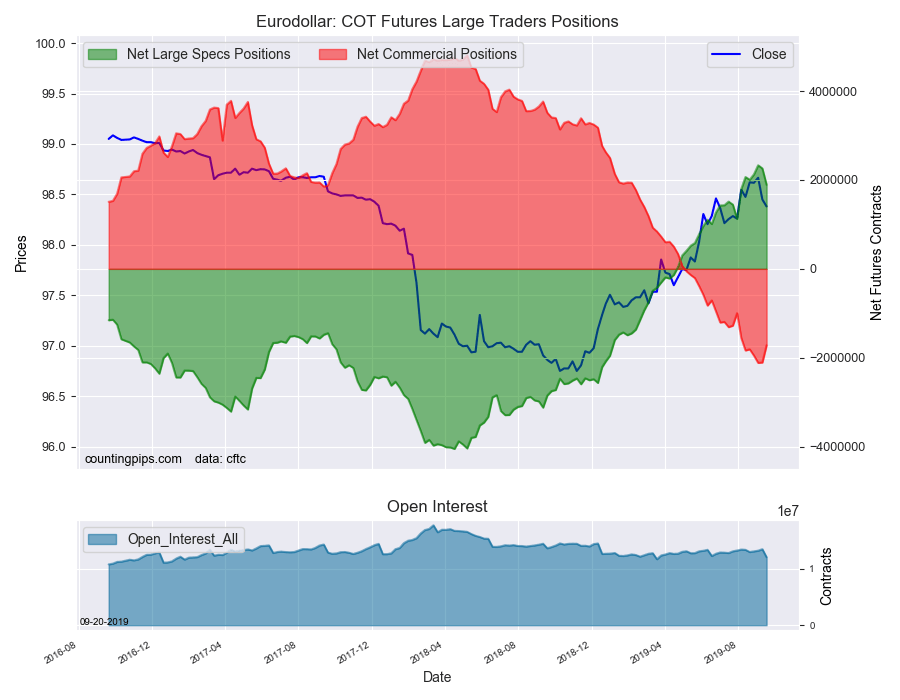

Large bond speculators decreased their bullish net positions in the Eurodollar futures markets last week after ascending to a multi-year high level, according to the latest Commitment of Traders (COT) data released by the Commodity Futures Trading Commission (CFTC) on Friday.

The non-commercial futures contracts of Eurodollar futures, traded by large speculators and hedge funds, totaled a net position of 1,890,849 contracts in the data reported through Tuesday September 17th. This was a weekly reduction of -370,345 net contracts from the previous week which had a total of 2,261,194 net contracts.

The week’s net position was the result of the gross bullish position (longs) dropping by -761,648 contracts (to a weekly total of 2,645,460 contracts) while the gross bearish position (shorts) fell by a lesser amount of -391,303 contracts for the week (to a total of 754,611 contracts).

Eurodollar speculators cut back on their bullish bets for the second straight week and by a total of -440,580 contracts over these past couple weeks. The speculative Eurodollar position has been consistently trending higher after turning from overall bearish to bullish on April 16th. The net position reached a 201-week high (dating back to October 2015) on September 3rd before turning lower on September 10th and 17th.

Eurodollar Commercial Positions:

The commercial traders position, hedgers or traders engaged in buying and selling for business purposes, totaled a net position of -1,719,047 contracts on the week. This was a weekly gain of 388,451 contracts from the total net of -2,107,498 contracts reported the previous week.

ED Futures:

Over the same weekly reporting time-frame, from Tuesday to Tuesday, the Eurodollar Futures closed at approximately $98.38 which was a decline of $-0.07 from the previous close of $98.45, according to unofficial market data.

*COT Report: The COT data, released weekly to the public each Friday, is updated through the most recent Tuesday (data is 3 days old) and shows a quick view of how large speculators or non-commercials (for-profit traders) as well as the commercial traders (hedgers & traders for business purposes) were positioned in the futures markets.

The CFTC categorizes trader positions according to commercial hedgers (traders who use futures contracts for hedging as part of the business), non-commercials (large traders who speculate to realize trading profits) and nonreportable traders (usually small traders/speculators).