Shares of Dova Pharmaceuticals opened 38% higher today on news that the firm will be acquired by Swedish Orphan Biovitrum. The deal is reportedly valued at $915 million or $29/share.

This morning Durham, N.C.-based Dova Pharmaceuticals Inc. (DOVA:NASDAQ)announced that it has entered into an agreement and plan of merger with Swedish Orphan Biovitrum AB (SOBI:OMX). The firm states that under the terms of the agreement, an indirect subsidiary of Sobi will commence a tender offer for all outstanding shares of Dova, whereby Dova stockholders will be offered an upfront payment for $27.50 per share in cash, along with one non-tradeable Contingent Value Right (CVR) that entitles them to an additional $1.50 per share in cash upon regulatory approval of Doptelet for the treatment of chemotherapy-induced thrombocytopenia (CIT), representing a total potential consideration of $29.00 per share, or up to $915 million on a fully diluted basis.

The company states that the upfront price of $27.50 per share represents a premium of 36% to Dova’s September 27, 2019, closing price and a premium of 59% to the 30-day volume weighted average price. The company advised that that the transaction was unanimously approved by the Boards of Directors of both companies and is expected to close in Q4/19. The firm added that the transaction is subject to customary closing conditions, including the tender of more than 50% of all outstanding Dova shares at the expiration of the offer and termination of the waiting period under the Hart-Scott-Rodino Antitrust Improvements Act. The non-tradeable CVR will be paid upon the regulatory approval of Doptelet for the treatment of CIT. There can be no assurance such approval will occur or that any contingent payment will be made.

Dova says that it will file a recommendation to shareholders recommending they tender their shares to Sobi, subject to the terms of the definitive merger agreement. Some of the company’s major stockholders, including Paul B. Manning, that represent a majority of the outstanding shares have entered into a Tender and Support Agreement committing them to tender their shares into the tender offer. The report notes that Sobi will acquire any shares of Dova not tendered into the tender offer through a merger for the same per share consideration as will be payable in the tender offer.

The proposed transaction is anticipated to enhance Sobi’s position as a leader in hematology and orphan diseases and expand its presence in the U.S. Sobi further intends to leverage its strong international presence to maximize the availability and commercial potential of Doptelet globally.

David Zaccardelli, PharmD, president and CEO of Dova, commented, “We are extremely pleased to announce this merger with Sobi, which we believe will continue the expansion of DOPTELET in the U.S., and provide the necessary resources to maximize DOPTELET’s availability to patients in both the US and internationally…On behalf of the Board of Directors, I’d like to thank our employees and shareholders for their continued support and dedication to our mission of providing novel and effective therapeutic options for patients with thrombocytopenia; we believe Sobi is ideally positioned to continue that mission.”

Sobi’s CEO and President Guido Oelkers, PhD, added, “The cadence of upcoming launches and approvals across indications and regions that Doptelet provides, enables us to further accelerate growth in our hematology franchise. There is a large unmet medical need within thrombocytopenia and for us this is a great opportunity to be able to give patients access to new and improved treatments. Furthermore, we are excited to welcome the 125 professionals from Dova who will greatly strengthen Sobi’s hematology infrastructure and broaden our value chain in the U.S.”

Sobi also announced the merger agreement today, stating that the acquisition of Dova provides it with Doptelet (avatrombopag), a differentiated on-market product in Chronic Immune Thrombocytopenia (ITP), a well established and growing market, for Chronic Liver Disease (CLD) and an ongoing phase 3 trial in Chemotherapy Induced Thrombocytopenia (CIT). The release noted that the acquisition of Dova will broaden the scope of Sobi’s product portfolio into hematology and enhance Sobi’s commercial presence in the U.S. Sobi claims that Doptelet will further diversify Sobi’s revenue base adding a new growth driver and that company will leverage its expertise and existing infrastructure in hematology to grow Doptelet across its indications by expanding patient access outside the U.S.

Dova Pharmaceuticals is based in Durham, N.C., and was founded in 2016 in order to commercialize Doptelet (avatrombopag), a second generation small-molecule thrombopoietin receptor (TPO) agonist used in the treatment of thrombocytopenia by increasing platelet count. Doptelet is approved by both U.S. Food and Drug Administration and European Medicines Agency for treatment of thrombocytopenia (low platelet counts) in adults with chronic liver disease (CLD). Doptelet was also approved in the U.S. for Chronic Immune Thrombocytopenia (ITP) in adult patients who have had an insufficient response to a previous treatment, and filing is expected in early 2020 in Europe. ITP is a rare autoimmune bleeding disorder characterized by a low number of platelets. Chronic ITP is a rare autoimmune bleeding disorder characterized by low number of platelets, affecting approximately 60,000 adults in the U.S.

Sobi is headquartered in Stockholm, Sweden, and states that it is a specialized international biopharmaceutical company that is transforming the lives of people affected by rare diseases. The firm lists that it provides sustainable access to innovative therapies in the areas of a specialized international biopharmaceutical company, immunology and specialty care. Sobi employs approximately 1,300 worldwide and had annual revenues of SEK 9.1 billion in 2018.

Dova Pharmaceuticals started the day with a market capitalization of about $581.5 million. The company has 28.8 million shares outstanding, and as of Friday’s close, had a short interest of around 6.1%. The stock has a 52-week price range of $5.6228.10/share. This morning, DOVA shares opened much higher at $28.00 (+$7.81, +38.68%) over Friday’s $20.19 closing price. The stock has traded on more than 12-times average volume today between $27.92 and $28.10/share and at present is trading at $27.97 (+$7.78, 38.53%).

Disclosure: 1) Stephen Hytha compiled this article for Streetwise Reports LLC and provides services to Streetwise Reports as an independent contractor. He or members of his household own securities of the following companies mentioned in the article: None. He or members of his household are paid by the following companies mentioned in this article: None. 2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. 3) Comments and opinions expressed are those of the specific experts and not of Streetwise Reports or its officers. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. 4) The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases. 6) This article does not constitute medical advice. Officers, employees and contributors to Streetwise Reports are not licensed medical professionals. Readers should always contact their healthcare professionals for medical advice.

The Critical Investor reviews Golden Arrow’s deal with SSR Mining to sell its remaining interest, and also discusses the company’s other projects.

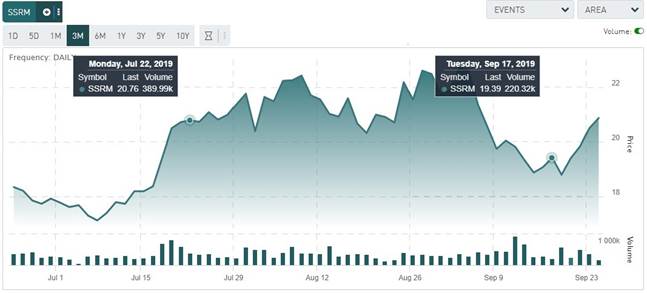

Golden Arrow Resources Corp. (GRG:TSX.V; GARWF:OTCQB; G6A:FSE) recently ended the seven-year-long Chinchillas adventure, by closing the deal involving selling its 25% interest in Puna Operations to SSR Mining Inc. (SSRM:NASDAQ) on September 19, 2019. Despite a rising silver price since the announcement of the sale on July 22, 2019, and consequently growing unease among shareholders of Golden Arrow about the appropriate value of the Puna asset, no less than 94.62% of represented voting interest voted in favor of the transaction.

All presented tables are my own material, unless stated otherwise.

All pictures are company material, unless stated otherwise.

All currencies are in US Dollars, unless stated otherwise.

The final specification of the C$44.4 million transaction payment came in as follows:

C$3.0 million in cash considerationunchanged

1,245,580 common shares of SSRM representing a value of approximately C$25.9 million and calculated using a price per share based on the 20-day volume weighted average trading price of SSRM’s common shares on the Toronto Stock Exchange ending on September 17, 2019this resulted in an average price per share of C$20.79, compared to an estimated 20d VWAP price per share of about C$19.40 at the time of the announcement at July 22, 2019. If Golden Arrow Resources had been able to fix the price at that day, it would have received 90,000 shares more, currently worth C$27.87 million, a difference of almost C$2 million or 7.7%. Share price 3 month time frame

Approximately C$15.1 million in cash, which amount was used to repay in full the outstanding principal and accrued interest owed by Golden Arrow under the credit agreement entered into in July 2018 with SSRMthis was C$14.5 million, and the result of additional accrued interest since the announcement

The return for cancellation, for no consideration, of 4,285,714 Golden Arrow common shares owned by SSRMunchanged

As we know from my last article about Golden Arrow, SSR Mining did an excellent deal at the bottom of the market, with Golden Arrow having so many financial obligations coming up (not only cash payments to SSR Mining to fund operational deficits, but also upcoming debt payments to SSR Mining and option payments for its other assets in 2020) that it basically had no other choice. For sure the company tried, but as it wasn’t able to raise more money at the time and Puna AISC was projected to remain unexpectedly high for the next quarters, the situation was dire. What seemed like a rock solid leveraged play on silver not too long ago quickly became one big financial liability.

How bad the negotiation position really was showed in the fact Golden Arrow couldn’t even arrange royalty or performance bonuses in case of higher silver prices. Management is no stranger to negotiations, as they for example beautifully worked out a 1% royalty on the Gualcamayo Gold Mine, owned by Yamana, bringing in between $2 million and $3 million annually. On November 12, 2012, they sold the NSR for no less than $17.75 million to Premier Gold Mines, bringing in a pile of cash so they could drill Chinchillas, their new exploration project at the time. One can also wonder why they didn’t negotiate an NSR when the JV was formed and the first 75% optioned out to SSR Mining, when sentiment was still good.

Investors weren’t too happy as the stock is trading even lower than the 2009 post-financial crisis lows, when all Venture stocks hit rock bottom at the time. This was of course well before the discovery of the Chinchillas deposit in 2012.

The latest small bull market, which started in 2016, helped sentiment in precious metals, and of course Macri came into power in December 2015 in Argentina, which at the time was seen as a huge economic catalyst for the country, after years of misery caused by Kirchner. Golden Arrow thrived on all this, further fueled by an extensive marketing program. Lots of investors with short horizons bailed out after the Puna JV was announced in March 2017, as they were targeting an outright buyout at a nice premium, and a JV would take many years to crystallize into solid cash flows.

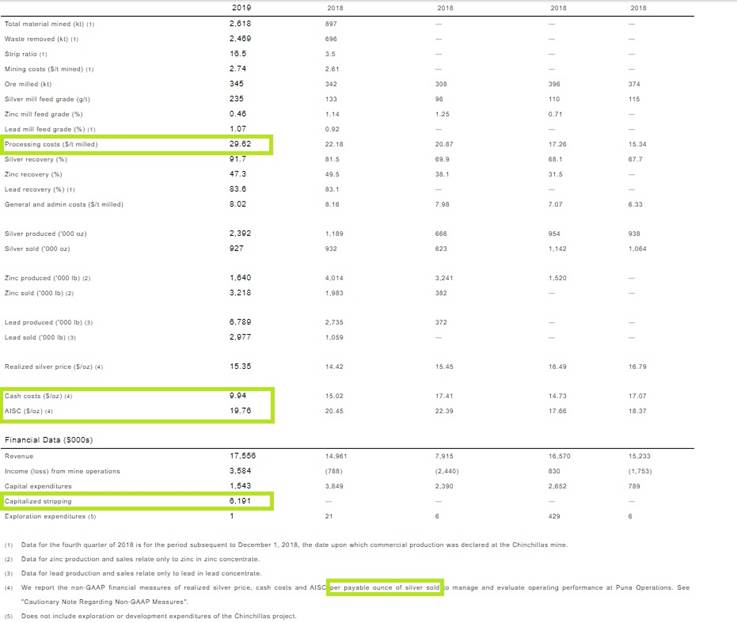

After that sentiment in general gradually slowed down, sending silver to multiyear lows again, as did the perception of Macri and his politics, which wasn’t as effective as hoped by many. As a result, Golden Arrow suffered along with investors, and had to wait for Puna cash flows. Unfortunately and unexpectedly, these never came so far, due to high opex. Instead of the planned PFS opex of US$9.75/oz Ag, cash costs were hovering around the price of silver itself for a long time (US$14-17/oz Ag), and last quarter (first quarter of commercial production) the AISC went considerably beyond that (US$19,76/oz Ag) despite cash cost coming down to US$9.94/oz Ag.

One can imagine for such developments to cause trouble for Golden Arrow, right at the time the company expected to see cash coming in from Puna. But it didn’t stop there, as SSR Mining projected this situation of high costs to last well into 2020, meaning Golden Arrow had to raise C$12 million each quarter to satisfy the cash calls from Puna by SSR Mining. This was the primary reason for Golden Arrow to sell its 25% interest, as the needed cap raises were almost undoable, also with the repayment of the US$10 million credit facility coming up in a year. Of course, with a willing JV partner one could roll over/refinance this debt or delay payments, but the cash calls weren’t handled as flexible, unfortunately.

I still have issues with the way SSR Mining handled all this as a majority JV partner. According to management, SSR Mining reportedly had to strip more than planned, and there were also heavy rains and severe lightning, causing problems for hauling ore to Pirquitas.

But the main difference in costs appeared to be in Processing, as reported in the SSR Mining Q1 news release, and this is something that is completely controlled by SSR Mining as the operator. Processing costs almost doubled compared to the PFS figures for Q1, as Golden Arrow provided the following numbers: Q1: Mining 2.74 USD/t-mined, Processing 29.62 USD/t-mined and G&A at 8.02 USD/t-mined versus PFS: of 2.52 USD/t-mined, Processing 15.08 USD/t-milled and G&A of 6.16 USD/-milled. This would have resulted in AISC being higher to the tune of an estimated $4/oz, which is substantial.

A lot of the high AISC could have to do with the lower sold ounce number, but then again cash costs are very low anyway, so something else is going on.

When looking closely, the realized stripping wasn’t out of the ordinary as it was planned to be (very) high the first commercial quarters in the PFS. When looking at PFS table 16.3, the stripping for Y2Q1 (Y2 is 2019) and Y2Q2 is indeed very high (16.51 and 14.42) as planned, but coming down fast in Y2Q3 and further (5.90, 4.32, 3.75, 5.7). The realized stripping was 16.5, so almost exactly as planned.

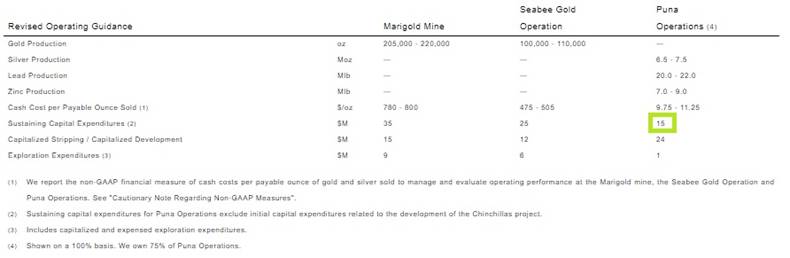

It seems as if sustaining capital was high for Q1, to the tune of an estimated $78 million, compared to a total forecasted sustaining capital outlook for 2019 of just $15 million:

Maybe my biggest issue with SSR Mining is why it didn’t sell more ounces of silver, as it produced 2.39Moz Ag and sold just 0.927Moz Ag. Zinc and lead evened out a bit more but also contributed to higher AISC. When you sell just 39% of the silver you produce it is only logical to expect huge pressure on cash flows in a ramping up operation. Golden Arrow did all it could, as it paid for all pre-production capital expenditures pro rata before the end of Q1. In my view, and of course I am biased, SSR Mining is at least partly responsible for the developments that forced Golden Arrow into selling their share in Puna.

One could say that the silver price didn’t cooperate, contracts are contracts and ramping up operations always has teething problems, but what is happening here is not making too much sense to me if SSR Mining really had a good, long-term relationship with Golden Arrow in mind. I do believe this could affect future JVs for SSR Mining, as potential JV candidates will undoubtedly have the Golden Arrow case vividly on their radar for many years to come.

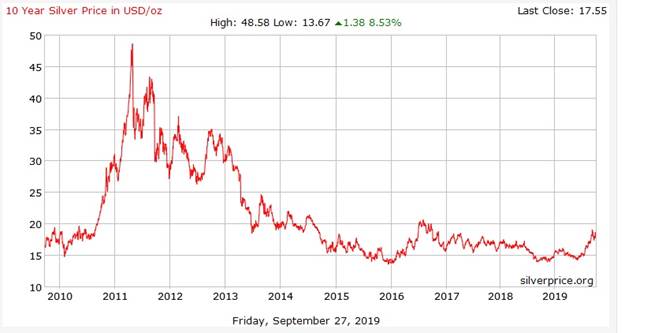

Of course the timing couldn’t have been better for SSR Mining, as the silver price just started something of a recovery, slowly following gold in its footsteps:

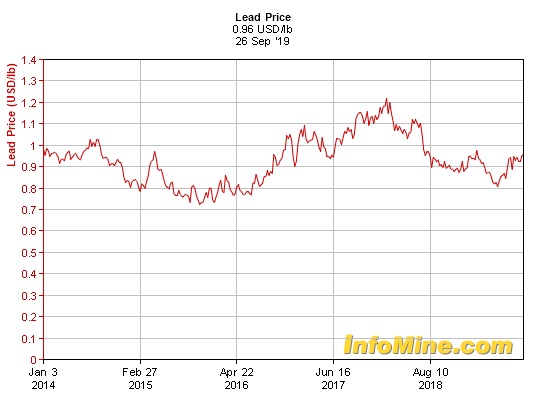

The lead price isn’t doing too much lately although it isn’t very volatile in general, at least much less compared to its sister zinc:

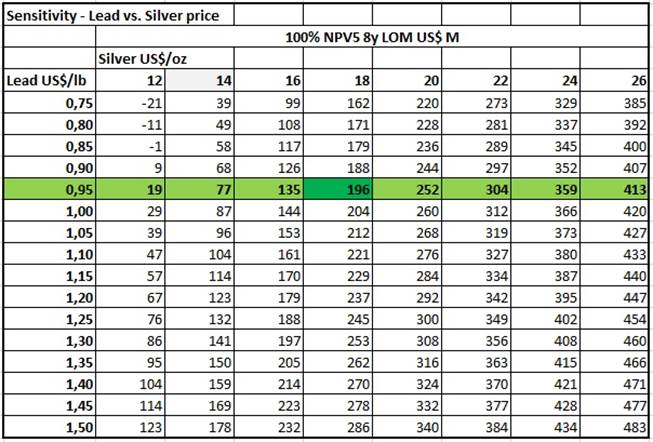

With silver at US$17.55/oz Ag, and lead at US$0.96/lb Pb, the NPV5 comes closer to PFS base case figures, based on US$19,50/oz Ag and US$0.95/lb Pb. A discount of 5% is warranted despite the jurisdiction, as commercial production has been reached and the original Pirquitas operation has been operating without major issues throughout its life of mine. Here is the sensitivity table:

The NPV5 at spot prices comes in at US$180 million, as I didn’t add full capex and pre-stripping to the NPV figures. It’s all subjective, but personally I never value a constructed plant at full capex value, as the minute one dollar is spent it is depreciated, as you can never get that dollar back in full. So I don’t automatically add full capex to NPV when construction is finished and commercial production starts. Another small item is the already extracted metals, of which potential cash flows have to be subtracted from the LOM production in the DCF model. When NPV5 is divided by 4, the 25% ownership of Golden Arrow attributes to US$45 million, which is C$60 million, so SSR Mining could already be sitting on C$15 million paper profits here. This is of course without calculating further upside, as the current resource easily enables a 50% longer life of mine, and potentially doubles it if almost all resources can be converted to a higher category. And of course, as Golden Arrow was one of theif not thebest leveraged plays on silver in my view, a rising silver price could turn things even more interesting for SSR Mining.

As Golden Arrow has lots of SSR Mining equity at its disposal now, a stronger silver price will undoubtedly have some positive influence, of course heavily watered down by the predominantly gold leveraged flagship assets. However, if silver does well, gold usually does even better these days, so as long as SSR’s gold mines keep on track I don’t see many issues here. What will Golden Arrow do with its current assets?

Nowadays, Golden Arrow has a significant portfolio of exploration assets, managed by fully owned subsidiary New Golden Explorations. It recently completed a sampling program at its Atlantida gold/copper project in Chile, which sports a 427Mt @0.43% CuEq historical resource, with the following highlights:

216 meters averaging 0.25 g/t Au in trench 2, including 48 meters averaging 0.53 g/t Au

74 meters averaging 0.66 g/t in trench 7

52 meters averaging 0.34 g/t Au and 10 meters averaging 0.96 g/t Au in trench 5

20 meters averaging 0.72 g/t Au in trench 4

The company is looking for large copper porphyries, which can be found all over the region, and has started a six-hole RC drilling program, aiming at completing 1,000 meters of drilling by the end of September. Management anticipates to be able after this to make a decision on the upcoming cash payment of US $0.4 million by October 3 for Atlantida. The project is made up of a collection of concessions, Atlantida being the largest. It has a 100% earn-in for US$6 million over four years. Even if the company decides to drop Atlantida it will retain other concessions in the area.

Another very interesting project the company optioned last year is the Indiana project, located about 35km from the Atlantida project, also in Chile. Indiana contains an historical, near surface Inferred resource of 600koz @4.7g/t AuEq (2.8g/t Au and @1.6% Cu), with high recoveries for both gold (90%) and copper (92%), with significant potential to increase resources. A two-stage drill program is planned, a 12-hole, 3,000m program is planned for ore shoot delineation and starts in October 2019, and a second program will follow this, testing potential expansion and new targets. A cash payment of US$1 million is due before year-end here.

Here the company has a 100% earn-in for a massive US$15 million over four years, with a last payment of US$7 million at the end of year 4. This sounds like a lot, but if it can prove up the historical resource as such, which could be all open pittable, and appears to have a low strip ratio, then this project will be very economic, as a small-medium sized 1.3-1.5g/t Au open-pit project can have a strip ratio of 4:1 and still be economic at US$1300/oz Au. If the section below is any indication, it seems that a strip ratio of 4:1 is definitely achievable.

Combined with the significant upside exploration potential this seems like a more interesting project than I previously thought. If the company manages not only to prove up the 600koz, but can expand it to, say, 1Moz at roughly the same grade, a hypothetical NPV8 of US$150200 million isn’t out of the question. If I were management, I would make this the flagship project.

Besides the Chilean projects, Golden Arrow optioned the Tierra Dorada project in Paraguay. This project doesn’t have a historical resource estimate on it, but has seen lots of sampling and some RC drilling, with results up to 148.4g/t Au, over a 2.5km sub-outcropping trend, and its geology is predominantly based on quartz veins.

To have an idea, historical drilling highlights include:

6.1m @ 1.12 g/t Au, including 1.5m @ 3.32 g/t Au in SM-H3 starting at 12.2 meters depth

3.05m @ 2.87 g/t Au, including 1.5m @ 3.74 g/t Au in SM-H4 starting at 19.8 meters depth

4.57m @ 1.72 g/t Au, including 1.5m @ 2.85 g/t Au in SM-H5 starting at 9.2 meters depth

3.05m @ 1.35g/t Au, including 1.5m @3.6g/t Au in SMH6 starting at 27.5 meters depthA reconnaissance exploration program including sampling, mapping, trenching and surveys has started a week ago, in order to define drill targets. This project has no cash payments due for year-end. There is a 100% earn-in for US$2 million over six years.

Finally, the company isn’t abandoning its long-time home base Argentina, as it still has five early-stage exploration projects in this country. The Flecha de Oro Gold project located in the Rio Negro province is more or less its flagship project over there. Gold mineralization has been found through sampling at numerous trends of quartz veins and stockworks. A surface sampling and mapping program, combined with a ground magnetic survey, will take place in Q4, starting next month. This project has a 100% earn-in for US$2.1 million over seven years.

Regarding cash payments, Golden Arrow had another project that has seen significant exploration spending and cash payments on it the last few years, and this is the Antofalla project in Argentina. However, management determined that results weren’t promising enough and didn’t justify further spending, and elected to opt out of this project.

Although Golden Arrow missed out on a golden opportunity (with no silver lining, unfortunately) to enjoy the Puna cash cow for a long time, not having to go back to the markets again for the foreseeable future not all is lost here. I view the Atlantida and especially the Indiana project as worthy successors of Chinchillas, with in my opinion Indiana definitely as the more economic prospect of the two, potentially even much more economic than Chinchillas itself. The company wasted no time and has started several exploration programs, which will generate news flow in a month or so.

Conclusion

Golden Arrow Resources seemed to have picked a very solid and trustworthy JV partner with SSR Mining, but unfortunately when things got difficult for the tiny junior, the mid-tier producer didn’t hesitate to add more pressure, in order to rip the 25% interest out of the hands of Golden Arrow at a bargain. I still have several question marks about proceedings, and I am certainly not blaming Golden Arrow management for all of this, although I feel they should at least have negotiated a royalty, either at the 75% sale or the 25% sale. Also agreeing to the non-solicitation clause was something that proved to be decisive, as discarding it could have saved Golden Arrow when silver prices went up and alternative financings could have presented themselves, but this is all in hindsight, of course. For now, the company is still very much alive, has a decent war chest that will last it at least well into 2021, is diversifying out of Argentina, which is going nowhere, and has a few very interesting exploration projects that will generate drill results pretty soon.

I hope you will find this article interesting and useful, and will have further interest in my upcoming articles on mining. To never miss a thing, please subscribe to my free newsletter on my website http://www.criticalinvestor.eu, in order to get an email notice of my new articles soon after they are published.

The Critical Investor is a newsletter and comprehensive junior mining platform, providing analysis, blog and newsfeed and all sorts of information about junior mining. The editor is an avid and critical junior mining stock investor from The Netherlands, with an MSc background in construction/project management. Number cruncher at project economics, looking for high quality companies, mostly growth/turnaround/catalyst-driven to avoid too much dependence/influence of long-term commodity pricing/market sentiments, and often looking for long-term deep value. Getting burned in the past himself at junior mining investments by following overly positive sources that more often than not avoided to mention (hidden) risks or critical flaws, The Critical Investor learned his lesson well, and goes a few steps further ever since, providing a fresh, more in-depth, and critical vision on things, hence the name.

The author is not a registered investment advisor, currently has a long position in this stock, and Golden Arrow Resources is a sponsoring company. All facts are to be checked by the reader. For more information go to www.goldenarrowresources.com and read the company’s profile and official documents on www.sedar.com, also for important risk disclosures. This article is provided for information purposes only, and is not intended to be investment advice of any kind, and all readers are encouraged to do their own due diligence, and talk to their own licensed investment advisors prior to making any investment decisions.

Streetwise Reports Disclosure: 1) The Critical Investor’s disclosures are listed above. 2) The following companies mentioned in the article are sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. 3) Statements and opinions expressed are the opinions of the author and not of Streetwise Reports or its officers. The author is wholly responsible for the validity of the statements. The author was not paid by Streetwise Reports for this article. Streetwise Reports was not paid by the author to publish or syndicate this article. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy.

4) The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases. As of the date of this article, officers and/or employees of Streetwise Reports LLC (including members of their household) own securities of Golden Arrow Resources, a company mentioned in this article.

The system, target markets and the marketing campaign for it are discussed in a Dawson James Securities report.

In a Sept. 26 research note, Dawson James Securities analyst Jason Kolbert reported that IsoRay Inc. (ISR:NYSE.MKT) launched a new marketing campaign called the The Power of Blu at the annual American Brachytherapy Science conference in June.

The purpose was to reintroduce IsoRay’s Cesium-131 as Cesium Blu and introduce its new Blu Build real-time Cesium-131 brachytherapy delivery system. That system was subsequently used for the first time by a physician as a treatment for prostate cancer.

Kolbert pointed out that Blu Build allows the physician user to target a tumor directly. That capability and the shorter half-life of Cesium-131 versus other radioisotopes on the market allow for minimization of damage to tissue at and around the cancer site. The end result is improved quality of life for the patient.

Kolbert concluded, “With a competitive price and a customized procedure model, the stage is set for Blu Build to be an effective (efficacy and cost) treatment for not only prostate cancer, but also other hard to treat cancers in the brain, pelvis, gynecologic, head, neck, lung, colon and rectal areas.”

The analyst also reported that IsoRay reported Q4 FY19 revenue of $1.9 million, with the preponderance of sales in the prostate cancer market during that period. This revenue resulted in $5 million on the balance sheet and a net loss of just over $1 million for the quarter.

Dawson James views the prostate cancer market as the real driver for IsoRay although opportunities exist in the non-prostate cancer market as well. The brokerage firm has a Buy rating and a $1 per share target price on IsoRay, whose stock is currently trading at around $0.33 per share.

Disclosure: 1) Doresa Banning compiled this article for Streetwise Reports LLC and provides services to Streetwise Reports as an independent contractor. She or members of her household own securities of the following companies mentioned in the article: None. She or members of her household are paid by the following companies mentioned in this article: None. 2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. 3) Comments and opinions expressed are those of the specific experts and not of Streetwise Reports or its officers. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. 4) The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases.

Disclosures for Dawson James Securities, IsoRay Inc., September 26, 2019,

The Firm does not make a market in the securities of the subject company(s). The Firm has NOT engaged in investment banking relationships with ISR in the prior twelve months, as a manager or co-manager of a public offering and has NOT received compensation resulting from those relationships. The Firm may seek compensation for investment banking services in the future from the subject company(s). The Firm has not received any other compensation from the subject company(s) in the last 12 months for services unrelated to managing or co-managing of a public offering.

Neither the research analyst(s) whose name appears on this report nor any member of his (their) household is an officer, director or advisory board member of these companies. The Firm and/or its directors and employees may own securities of the company(s) in this report and may increase or decrease holdings in the future. As of August 31, 2019, the Firm as a whole did not beneficially own 1% or more of any class of common equity securities of the subject company(s) of this report. The Firm, its officers, directors, analysts or employees may affect transactions in and have long or short positions in the securities (or options or warrants related to those securities) of the company(s) subject to this report. The Firm may affect transactions as principal or agent in those securities.

Analysts receive no direct compensation in connection with the Firm’s investment banking business. All Firm employees, including the analyst(s) responsible for preparing this report, may be eligible to receive non-product or service specific monetary bonus compensation that is based upon various factors, including total revenues of the Firm and its affiliates as well as a portion of the proceeds from a broad pool of investment vehicles consisting of components of the compensation generated by investment banking activities, including but not limited to shares of stock and/or warrants, which may or may not include the securities referenced in this report.

Analyst Certification: The analyst(s) whose name appears on this research report certifies that 1) all of the views expressed in this report accurately reflect his (their) personal views about any and all of the subject securities or issuers discussed; and 2) no part of the research analysts compensation was, is, or will be directly or indirectly related to the specific recommendations or views expressed by the research analyst in this research report; and 3) all Dawson James employees, including the analyst(s) responsible for preparing this research report, may be eligible to receive non-product or service specific monetary bonus compensation that is based upon various factors, including total revenues of Dawson James and its affiliates as well as a portion of the proceeds from a broad pool of investment vehicles consisting of components of the compensation generated by investment banking activities, including but not limited to shares of stock and/or warrants, which may or may not include the securities referenced in this report.

Money manager Adrian Day reviews two undervalued resource companies that have seen important recent developments.

Osisko Gold Royalties Ltd. (OR:TSX; OR:NYSE, US$9.69) has moved further away from the pure royalty model with the acquisition of Bakerville Gold Mines for equity valued (at the time of the bid) at CA$338 million. Based on the August PEA (preliminary economic assessment) on Bakerville’s Cariboo project in British Columbia, this is an acquisition price of 0.6 times net present value. Osisko, which already held 33% of Bakerville, says it intends to develop the project and then monetize it, “ultimately,” when the junior market improves.

At the same time, Osisko announced it had formed the North Spirit Discovery Group, intended to develop and finance projects in Canada, in conjunction with joint venture partners or private equity. Few details were revealed.

Royalties or Development: Which Is Primary Though the Bakerville acquisition is accretive to net assetsit does reduce cash flow per sharemore importantly to us, it moves Osisko away from the pure royalty model. It has long been a hybrid, with its increasingly important “accelerator model.” But rather than financing a junior in exchange for royalties, it increasingly seems to be using royalty revenue to acquire and develop projects. It is fair to say that CEO Sean Roosen is a mine builder at heart; he and his team built Canadian Malartic, one of the largest mines in the country. They lost the mine after a hostile takeover fight initiated by Goldcorp Inc., eventually selling to Agnico Eagle Mines Ltd. (AEM:TSX; AEM:NYSE) and Yamana Gold Inc. (YRI:TSX; AUY:NYSE; YAU:LSE) in exchange for an attractive royalty, the foundation of Osisko Gold Royalties. We agree with Roosen when he says that there are tremendous opportunities in Canada and that the industry has underspent on exploration, drilling and development.

Good Deal, but Increased Risk So this opportunistic acquisition may be a good deal, but it adds to the risk at a royalty company that was already a higher-risk company than its peers. Because of this, it has traded at lower multiples than other royalty companies. Now the risk is increased, and so too is the justifiable discount at which it should trade. From $12.25 per share at the beginning of the week, the stock plunged after the deal was announced to close at $9.70.

This is overdone, and Osisko can be bought here, but no longer with the expectation that the valuation gap should completely close over time.

New Mine and Saving Another In other recent developments, Osisko saw the first gold pour at Victoria Gold Corp.’s (VIT:TSX.V) Eagle Gold Mine in the Yukon, on which it holds a 5% royalty. This is a successful example of the company’s accelerator model.

It also announced the successful completion of a restructuring of Stornoway Diamond Corp. (SWY:TSX); with other creditors, Osisko acquires Stornoway, on whose Renard mine it holds a 9.6% stream. Renard, which continues to operation, represents about 3% of Osisko’s royalty revenue, so again, this is a significant investment, which may prove successful but deviates from the royalty model.

Not unexpectedly, Pretium Resources Inc. (PVG:TSX; PVG:NYSE) bought back an offtake agreement from Osisko, following its repurchase of a royalty on its Brucejack Mine. This is a bad result for Osisko since the offtake was a low margin asset after losing the royalty, and adds over US$40 million to the cash balance. Together with an increase in its credit facility (to $400 million), this puts the company in a strong position, with about CA$525 million liquidity by year end.

More Risk and Lower Valuation Than Peers Osisko is a dynamic company, with two foundational cash-flowing royalties (Malartic and Eleonore), other cash-flowing assets, and an increasing pipeline; it has a strong balance sheet, and aggressive and technically strong management. But it carries significantly higher risk than a traditional royalty company, risk that appears to be increasingly not diminishing. So it should trade at a discount to pure royalty companies.

But its current value of price-to-book of 1.2x, and price-to-free cash flow of 24x, with a yield of 1.6%, compares very favorably with, say, industry-leader Franco-Nevada Corp.’s (FNV:TSX; FNV:NYSE) multiples of 3.6x book; 35x cash flow (the free cash flow number is distorted for this year); and a yield of less than 1.1%. Franco remains our core holding, but Osisko is a buy at this level.

Fortuna’s Next Mine Nearly There

Fortuna Silver Mines Inc. (FSM:NYSE; FVI:TSX; FVI:BVL; F4S:FSE, US$3.27) has announced the start of pre-production mining at its Lindero gold project, another milestone toward first gold pour in the first quarter of 2020. In building the mine, Fortuna experienced a modest delay and cost overrun, largely due to unusually heavy rains which flooded the road to the site. But the mine is well on its way to completion, 70% complete as of the end of August. The company’s website includes a brief video showing the progress on site. Guidance for the mine to produce 145,000 to 160,000 ounces of gold in its first 12 months remains, and representing nearly half of the company’s free cash flow by 2021, after the ramp-up is complete.

Earlier in the month, Fortuna issued a convertible debenture with interest of 4.65%, raising $40 million. The funding was not necessary to complete construction at Lindero, but Fortuna, a very conservative company, wanted a minimum of $50 million cash on hand until Lindero is successfully producing.

Argentina Risk Fortuna has three strong mines (long-life and a high-grade silver mines in Peru and Mexico, respectively, in addition to Lindero), a strong balance sheet, and technically strong and conservative management. The problem is that Lindero is in Argentina. The opposition, with former president Christina Kirchner as running mate on the presidential ticket, is expected to win next month’s election handsomely, bringing concerns of a return to the disastrous economic policies of her administration. After a win in a primary election, the peso has collapsed, leading supposedly pro-market president Marci to introduce capital controls and renegotiate the terms of much outstanding debt. Although presidential front-runner Fernandez has made some placating sounds, there are concerns that the country will see higher inflation, export controls, and another debt crisis.

All this has real impact; Fortuna’s VAT refund after mine completion may turn out to be considerably less, in dollar terms, than what it paid, for example, while inflation will lead to higher wages at the mine, and most important, export controls may limit what it can take out of the country in dollars. Since it has, more or less, completed its construction costs, it is now in no need of pesos in the country. In addition to the reality is the perception, which will affect investors’ willingness to hold companies heavily exposed to the country.

Buy. . .and Trade Unfortunately, this could get a lot worse before it gets better, so we expect Fortuna to trade below comparable valuations for other growing producers. From $4.33 per share at the beginning of the month to $3.27 today, the stock, already undervalued as discussed in our previous write-up, is discounting most of the risks. At this price, it is trading at only 85% of book, with a cash-flow multiple of 7.5 times. At todays level, Fortuna is a buy and a strong one. We do expect further volatility as the Argentina situation develops, so you should be ready to trim positions on rallies, and add on any shocks that may come along.

Support for Almaden

Mexico’s environmental authority recently held a public consultation meeting regarding Almaden Minerals Ltd.’s (AMM:TSX; AAU:NYSE) Ixtaca project in the town of Santa Maria on June 25. The meeting was recorded. You don’t have to be fluent in Spanish to get a feeling that there is support among local people for this project.

Adrian Day, London-born and a graduate of the London School of Economics, heads the money management firm Adrian Day Asset Management, where he manages discretionary accounts in both global and resource areas. Day is also sub-adviser to the EuroPacific Gold Fund (EPGFX). His latest book is “Investing in Resources: How to Profit from the Outsized Potential and Avoid the Risks.”

Disclosure: 1) Adrian Day: I, or members of my immediate household or family, own shares of the following companies mentioned in this article: Franco-Nevada. I personally am, or members of my immediate household or family are, paid by the following companies mentioned in this article: None. My company has a financial relationship with the following companies mentioned in this article: None. Funds controlled by Adrian Day Asset Management hold shares of the following companies mentioned in this article: Almaden Minerals, Fortuna Silver Mines, Osisko Gold Royalties. I determined which companies would be included in this article based on my research and understanding of the sector. 2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: Pretium Resources. Click here for important disclosures about sponsor fees. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. 3) Statements and opinions expressed are the opinions of the author and not of Streetwise Reports or its officers. The author is wholly responsible for the validity of the statements. The author was not paid by Streetwise Reports for this article. Streetwise Reports was not paid by the author to publish or syndicate this article. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy. 4) This article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 5) From time to time, Streetwise Reports and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases. As of the date of this article, officers and/or employees of Streetwise Reports LLC (including members of their household) own securities of Osisko Gold Royalties,Franco-Nevada, Newmont Goldcorp and Pretium Resources, companies mentioned in this article.

The latest clinical trial results are dissected in a ROTH Capital Partners report.

In a Sept. 26 research note, ROTH Capital Partners analyst Jerry Isaacson reported that AzurRx BioPharma Inc.’s (AZRX:NASDAQ) Phase 2 OPTION trial for lead candidate MS1819 in cystic fibrosis patients “answered all of the questions surrounding the treatment, all with positive results.”

Isaacson explained that overall, the study, which compared MS1819 to the standard of care, or a pancreatic enzyme replacement therapy (PERT) regimen, demonstrated that MS1819 improved patients’ coefficient of fat absorption. Also, it showed nitrogen absorption with MS1819 was comparable to that with PERT. Further, concerning the primary question and goal, the trial showed MS1819 to be safe.

“We find the market’s reaction to the data unfortunate,” given the results and given the company is now “poised for late stage development,” he added.

In contrast to the market, ROTH considers AzurRx a stock with multibagger potential, as indicated by its target price on the biopharma of $10.20 per share. The company’s current share price is around $0.61.

Isaacson discussed the efficacy and safety of MS1819 as demonstrated in the OPTION trial.

Regarding efficiency, he highlighted that the study importantly showed the coefficient of nitrogen absorption with MS1819, 93%, was comparable to that with PERT, 97%. “This result shows that a protease is not a necessary addition to MS1819, clearly validating the company’s hypothesis,” he commented.

Also, half of the OPTION patients achieved a coefficient of fat absorption that was not inferior to that obtained with PERT. This indicates the dose of MS1819 administered is efficacious but greater doses could yield a greater fat absorption benefits in a larger proportion of patients.

Regarding safety, in OPTION, AzurRx could only test an MS1819 dosing 2 grams per day despite the optimum dosing likely being higher. This was due to the U.S. Food and Drug Administration’s (FDA’s) concerns about the drug’s safety, Isaacson pointed out. However, with the study results allaying that worry, the biopharma now can conduct a trial that “truly demonstrates the efficacy of MS1819.”

As such, the next step is a Phase 2b/3 trial in which AzurRx will likely test higher doses of the enzyme. It also will administer MS1819 via an FDA-approved, enteric-coated capsule for optimal drug delivery.

The U.S.-based company has another Phase 2 trial of MS1819 underway, that one in patients with more chronic cystic fibrosis, with severe exocrine pancreatic insufficiency. The study is testing the administration of MS1819 in addition to the standard of care.

Disclosure: 1) Doresa Banning compiled this article for Streetwise Reports LLC and provides services to Streetwise Reports as an independent contractor. She or members of her household own securities of the following companies mentioned in the article: None. She or members of her household are paid by the following companies mentioned in this article: None. 2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. 3) Comments and opinions expressed are those of the specific experts and not of Streetwise Reports or its officers. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. 4) The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases.

Disclosures from ROTH Capital Partners, AzurRx BioPharma Inc., Company Note, September 26, 2019

Regulation Analyst Certification (“Reg AC”): The research analyst primarily responsible for the content of this report certifies the following under Reg AC: I hereby certify that all views expressed in this report accurately reflect my personal views about the subject company or companies and its or their securities. I also certify that no part of my compensation was, is or will be, directly or indirectly, related to the specific recommendations or views expressed in this report.

ROTH makes a market in shares of AzurRx BioPharma, Inc., Inc. and as such, buys and sells from customers on a principal basis.

Shares of AzurRx BioPharma, Inc. may be subject to the Securities and Exchange Commission’s Penny Stock Rules, which may set forth sales practice requirements for certain low-priced securities.

ROTH Capital Partners, LLC expects to receive or intends to seek compensation for investment banking or other business relationships with the covered companies mentioned in this report in the next three months.

Sector expert Michael Ballanger interprets the implications of the last COT report for the precious metals markets.

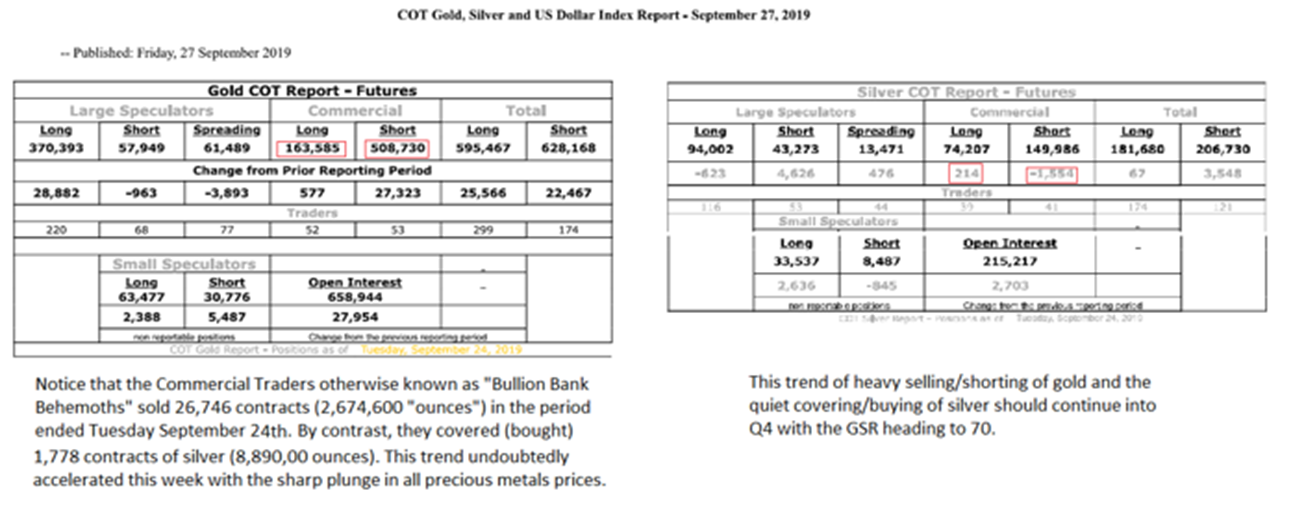

It was only a few hours ago that I was cruising through a lovely early-autumn Friday afternoon preparing for one of the last weekends at the marina for the 2019 season when I came across the much-heralded (and often misinterpreted) COT report. I was on the way up the eastern shoreline of Lake Simcoe when I saw that, for the COT week ended Sept. 24, the Commercial Cretins, seeing the usually wrong Big Money managers drunkenly piling into carloads of December gold contracts (29,845 contracts to be sure) hand over fist, decided to “fill ’em”and they happily supplied all of the paper gold needed to crush the advance at the exact, precise peak of the advance, which ended Tuesday at $1,543.50.

The rest (of the week), as they say, was history, and in more ways than simply the passage of time. December gold lost over $50 as option expiries, futures expiries and general Bullion Bank shenanigans all conspired to vaporize any semblance of investor optimism. It puts to bed the notion, as I have been warning for weeks now (amid blogosphere ridicule and investor anxiety), that the “Forces of Goodness” had finally and forever vanquished the banking cartel and its symbolic putrefaction.

My worst recurring nightmare of the past forty-five years has me sitting in a final exam room during my graduation year of university completely unprepared and totally in need of a passing grade to receive my diploma. It actually did happen to me but, as it turned out, the professor was a hockey fan and cut me a much-needed break, a C+ in Statistics and Data Analysis, arguably the most boring class I have ever taken.

The second recurring nightmare is one that has only cropped up in recent months, and it is that the precious metals markets revert back to pre-June behaviors, with COT reports calling the shots and commercial traders once again slapping the managed money CTAs like rented mules.

From the August 2016 top to the May lows, I successfully avoided five massive drawdowns by trading with the bullion bank criminals, choosing to fade all rallies in gold that accompanied their aggressive shorting activities. It worked until the June 20 breakout, after which all bets had to be cancelled and strategies reexamined. However, in the past three weeks, it appears that investor complacency in the precious metals community allowed the Bullion Bank behemoths to quietly creep back in the control room where, in a matter of a few short weeks, they have inflicted immeasurable pain on the newborn bulls that were taking victory laps on Sept. 4, “long leveraged” to their back teeth, with champagne flute in hand.

The silver COT was far more friendly than the gold COT, but month-end shenanigans may wreak havoc upon both metals with the bottom later in the week. After the Twitterverse became inundated with bullish pronouncements from bloggers around Sept. 4, the space is now eerily silent, with bullish tweets being recalled and the fuzzy-cheeked trading wizards all hiding under their desks.

Conditions like this, while normally bullish, are not going to disappear overnight, because just as “Hell hath no fury like a woman scorned,” “Hell hath no fury like a Bullion Banker burned.” so the vengeance being inflicted on those who failed to heed Santanyana’s finger-wagging rebuke (something about people ignoring history’s famous mistakes being doomed to repeat them in the future) are now being fully educated on the meaning of the term “wrath.” To be sure, $50 drops in gold and $2 drops in silver can soften stardom and end marriages, not to mention foster an alcohol addiction and high dives from skyscrapers.

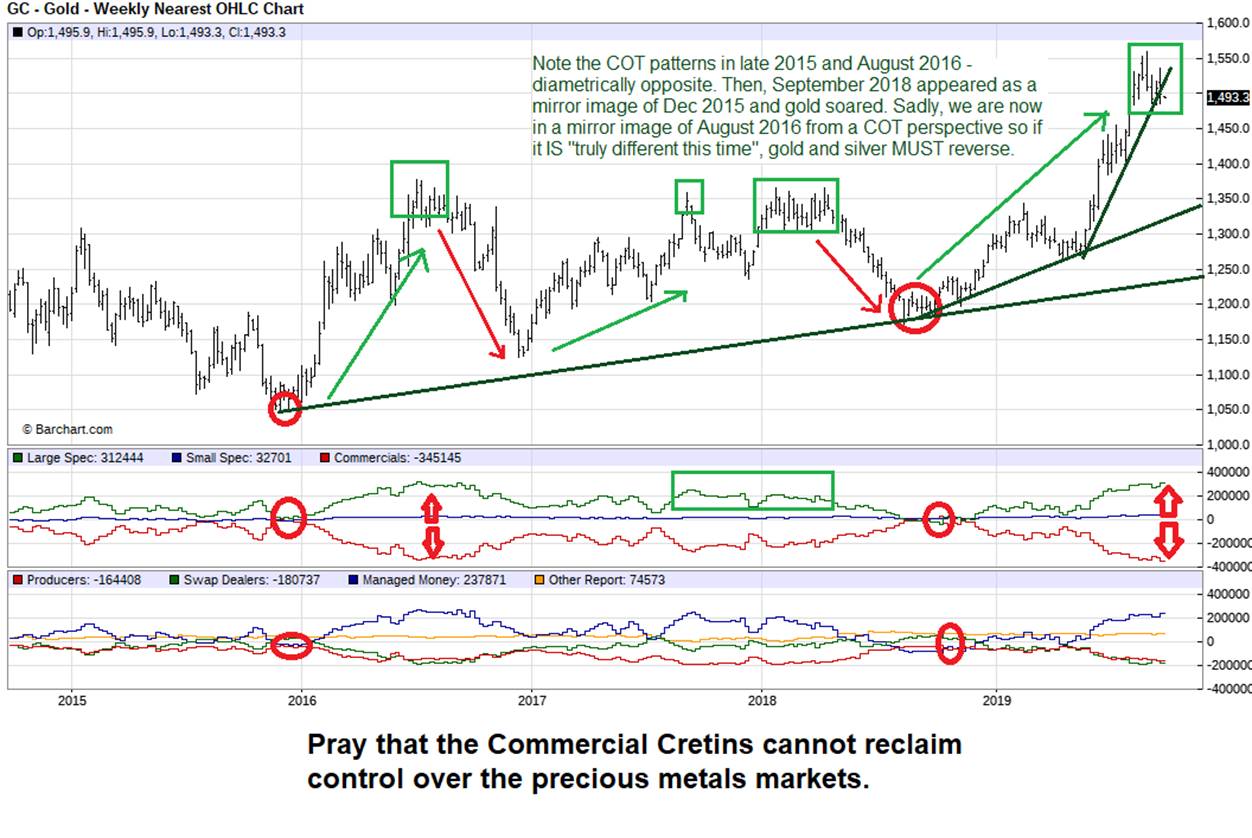

Another way of looking at the COT is through the eyes of a professional money manager (“Large Speculator”). This chart clearly illustrates the manner in which the Commercials lie in wait as the Large and Small Speculators, comprised of money managers, CTAs and the public, get completely fleeced by the Commercials, comprised of Bullion Banks supposedly acting on behalf of “clients” hedging future production. (If you believe the cartel bankers are acting only on behalf of clients, I have 100 acres of quality farmland just outside of Chernobyl to sell you.)

From June until mid-September, most of the skirmishes went to the Large and Small Speculators. This has recently reversed with a “déjà vu all over again” creeping back into the Crimex pits. We know that the “creature” shown in the graphic is really the central banking cartel, and when the jaws of extreme positioning widen, a downturn is inevitableand that is what we are now witnessing as we move into Q4.

This correction in gold (and silver) is the natural outcome of excessive greed, where newly anointed participants suddenly discover a long-awaited uptrend and come piling into the market, ignorant beyond all comprehension of the dangers lurking below the surface and well-off the radar.

Old-timers (like me) saw the rush to judgement coming late last month and began scaling back and taking profits, and only just began replacing positions late last week. The 50-dma (daily moving average), at $1,502, has now fallen to the Evil Axis of Market Manipulation, with $1,434 and $1,377 holding the fort at 100-dma and 200-dma levels of solid support.

Mind you, those with any cranial cells left are now looking with agony-filled eye sockets at the $1,525 level, where, back in 2013, its defeat ushered in thirty more months of dental surgery sans novocaine. Healthy bull markets tend to shrug off attacks such as this, so while the stalwart bulls will feign indifference to a $1,485 gold price because of the much-daunted “$1,375 breakout,” I do not want to see a print anywhere close to $1,434, or even $1,450. We need a solid turn in the precious metals this week or else my second-worst nightmare may become a reality.

I completed the buybacks of the senior and junior miner ETFs late last week, and although both are a tad weaker today, the GDX/GDXJ dynamic duo will probably (hopefully?) resume their uptrends by the end of the week, after the institutional money flows return to normal. The GSR, at 86.6, is still well below my short entry level of 92.40, but it is also a far cry from the 78.9 level it touched on Sept. 4. Silver itself is now a full $2.55/ounce below the 52-week high of $19.75, and well below the 2016 high north of $21/ounce. I thought that $17.50 would be the “line in the Sand,” but obviously, the Commercial Cretins thought otherwise, and but for month-end malarkey, this week “should” mark the turn (back up) with the operative word being should.

A great many e-mails, phone calls, tweets and text messages have bombarded me in the past few days, all with the same inquiry: “Is the bull move finished?” My reply is emphatic: “Not on your life.” Long before the price explosion in June, I was writing about the growing mistrust permeating the global debt arena, and that, my friends, has not ceased and desisted, nor will it any time soon. I think that the $1,566.20 and $19.75 price points for gold and silver might have been the highs for the year, but with global debt levels exceeding $246 trillion (as of July 15), that number is 320% of global GDP and an unarguable floor of support for gold and silver ownership.

Debt is going to be the undoing of not only this global stock market obsession; it is also going to be the Great Unraveller of standards of living around the planet. So, with Fido once again hiding in the crawl space under the tool shed and my domestic partner currently residing somewhere in the next county, and with dart boards of Jerome Powell and Mario Draghi pockmarked with ordnance holes, conditions are now ideal for a return of the precious metals’ uptrends. The only thing missing is a quote machine sailing through the air in search of a Bullion Banker forehead, but that may not (or may) be necessary during this go-around.

Originally trained during the inflationary 1970s, Michael Ballanger is a graduate of Saint Louis University where he earned a Bachelor of Science in finance and a Bachelor of Art in marketing before completing post-graduate work at the Wharton School of Finance. With more than 30 years of experience as a junior mining and exploration specialist, as well as a solid background in corporate finance, Ballanger’s adherence to the concept of “Hard Assets” allows him to focus the practice on selecting opportunities in the global resource sector with emphasis on the precious metals exploration and development sector. Ballanger takes great pleasure in visiting mineral properties around the globe in the never-ending hunt for early-stage opportunities.

Disclosure: 1) Statements and opinions expressed are the opinions of Michael Ballanger and not of Streetwise Reports or its officers. Michael Ballanger is wholly responsible for the validity of the statements. Streetwise Reports was not involved in any aspect of the article preparation. Michael Ballanger was not paid by Streetwise Reports LLC for this article. Streetwise Reports was not paid by the author to publish or syndicate this article. 2) This article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 3) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases.

Charts provided by the author.

Michael Ballanger Disclaimer: This letter makes no guarantee or warranty on the accuracy or completeness of the data provided. Nothing contained herein is intended or shall be deemed to be investment advice, implied or otherwise. This letter represents my views and replicates trades that I am making but nothing more than that. Always consult your registered advisor to assist you with your investments. I accept no liability for any loss arising from the use of the data contained on this letter. Options and junior mining stocks contain a high level of risk that may result in the loss of part or all invested capital and therefore are suitable for experienced and professional investors and traders only. One should be familiar with the risks involved in junior mining and options trading and we recommend consulting a financial adviser if you feel you do not understand the risks involved.

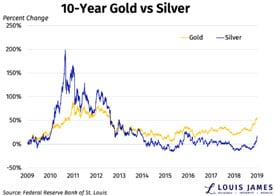

The people who are prepared are going to reap rewards such as they have never dreamed. We’re going to have the biggest transfer of wealth in history – from the fools – to those who are prepared. – Bob Moriarty

The run up of the last few months to $1,565 gold and $19 silver has stalled out into a relatively high-level correction, giving back less than might be expected after such a spirited rise.

Many people are focusing on the downside, without asking themselves, “What’s the relative reward?”

Even if you only believe the upside case to be around $2,000, that’s still a potential 5x:1 reward compared to perceived risk.

Whatever gold’s potential gain, silver’s will almost certainly be considerably greater, as has historically been the case.

In the 1970’s bull run, my biggest holding was silver bullion. The stagflation theme made it the go-to asset. Is history about to repeat? I think so.

Note the excellent overall performance of silver against gold during the 1970s. Singapore dealers are suddenly reporting that investors are buying more silver than gold. My simple advice to investors in the West is: Join them and buy silver bullion now! – Stewart Thomson, Graceland Updates

On the above chart above we can see that silver tends to be quite volatile on the upside – and as recent trading sessions have demonstrated – on the downside too!

This is why you should be leery of adding leverage or margin. Just stick with tubes of physical trade rounds, and/or bars from reputable dealers.

Could I be wrong? Of course. Risk and reward go hand in hand. Remember, without risk, there would be no profit potential either. (Though negative interest bonds are attempting to disprove this thesis!)

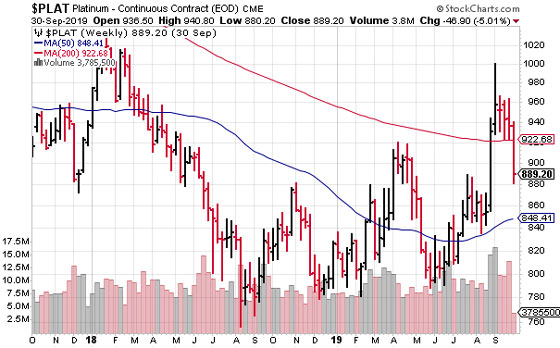

“Platinum declining into support.”

Check your premise. How big is your picture? How much and for how long are you willing to wait? Does any other current investment theme offer such asymmetric potential?

Though platinum is a smaller market, it holds a certain allure. Largely an industrial metal, the questionable supply profile, coming mostly from South Africa, Zimbabwe and Russia, makes it an interesting speculation.

Until a few years ago, this metal (known as “little silver” by early Spanish Conquistadors who tossed it back into a stream to “grow up”), has usually sold for several hundred dollars/ounce more than gold.

Now at almost six hundred dollars less, the profit potential in platinum could be substantial, if it can regain its normal relationship.

Throwing the Bones. In ancient cultures, animal bones were heated and tossed onto a mat, looking for “patterns” to predict the future. Today, Elliott microWavers, Japanese Candlestickers and other precious metals’ “bone throwers” seek to divine data from charts and graphs.

In fact, we use some of those tools ourselves. But occasionally, a massively profitable opportunity arises when a sector has reached a certain “tenor” that a bone toss can’t tease out.

Where the best efforts at interpreting the questions Mr. Market poses cannot be answered until later. Where maybe this time it is different. Where those who don’t hold anything at all – regardless of the current price – run the risk of being left completely behind.

It’s not easy to “buy the correction.” You can either take a position and accept information risk or wait until later and deal with price risk. Stu Thomson nails it when he says,

We are all cowards on price weakness. Those who admit it, who bet against it make money. Those who hide it and lie about it, lose money. End of story.

Don’t forget that during a correction, most news is negative. You’ll be dealing with the crowd’s uncertainty.

You’ll start doubting yourself, waiting for even lower prices, and more than likely fail to carry out the most critical step – acting on what you’ve already decided.

Maybe you didn’t buy gold at $1,100, or $1,250 or $1,350. Perhaps you kept waiting for the arrival of a well-known analyst’s call of $700. (Whose tune has now changed to predicting $1,800!). What to do now?

At certain times in history owning money is the best available “investment” idea, because all other investment classes have become so corrupted and distorted that having money is the only sensible choice. We are at such a point today, which means people who are the best informed, choose to place a portion of their wealth into the precious metals. David Morgan

Confusing linear with exponential. Markets spend most of the time trading in a linear, predictable manner – usually in congestion; occasionally in an up or down trend run.

Over 90 percent of the time, Bollinger Bands contain price movement within two standard deviations above or below the mid line. But once in awhile an outlier – stronger and more durable than the markets expect – is capable of driving the price exponentially in one direction.

This is where really big money can be made… or missed. If you wait for it to become obvious, these exceptional gains can reduce a speculator to the status of… a spectator.

The Gold story, while showing more of the same, is also shifting emphasis. It is making all-time highs in most of the world’s major currencies. Central banks bought a record 651 tonnes in 2018 – a 75% increase from the previous year, and the highest level of net purchases since 1971 when President Nixon closed the gold window.

Additions by China, Russia, India and Turkey remain robust. But in recent months, a larger percentage of the world’s gold refining, which routes through Switzerland on its way to Asia, is being siphoned off to the U.K. Germany, and France.

This shift is a strong indicator that the crucial “missing link” – a metaphorical spark which can ignite the supply-demand powder keg, destroying the market’s delicate balance – may soon be lit.

Add the fear of missing out by North Americans as it becomes obvious that the last train is leaving the station, and in short order a demand contagion could spread across the entire precious metals’ space.

It would be wise rather soon to decide if you want to participate…or just watch and wish you had.

The Money Metals News Service provides market news and crisp commentary for investors following the precious metals markets.

From the tiny archipelago of Seychelles in the Indian Ocean to Europe and the United States, monetary policy was loosened further in the third quarter of 2019 as 46 central banks slashed interest rates 67 times in response to muted inflation and a synchronized global economic slowdown.

Monetary policy worldwide pivoted at the start of the year from tightening to easing, and the pace of rate cuts has accelerated during the year as the U.S. administration’s efforts to reshape the global trading system threatens economic growth by disrupting cross-border supply chains and undermining business confidence and investment.

In contrast to 2018, when central banks raised interest rates and continued to wean financial markets of some $12 trillion of extra money that was pumped into the global system through asset purchases, 2019 has been characterized by a rapid pace of pre-emptive rate cuts in response to the prospect that global growth will slow to the weakest level since the global financial crises.

In the third quarter, benchmark interest rates were cut 67 times and by a total of 28 percentage points, up from 26 cuts in the second quarter by 15.75 percentage points, and 19 cuts in the first quarter by 925 basis points.

In September alone, policy rates were cut by a total of 1,050 basis points, up from cuts of 800 points in August and 950 points in July.

Year-to-date 60 central banks have cut policy rates 113 times and by a cumulative 47.21 percentage points, easily rolling back rate hikes that totaled 43.40 percentage points in 2018.

In addition to rate cuts, central banks have also turned to other tools to stimulate credit and economic activity as the threat of inflation, the main focus of central banks, evaporates across the world as waning demand undermines energy and commodity prices.

Including cuts in reserve requirements, new low-cost loans and restarting asset purchases, central banks worldwide have taken 130 steps toward easier policy, including 117 rate cuts, out of 414 policy decisions followed by Central Bank News as of Sept. 30.

In contrast only 15 central banks have tightened their policy this year, including raising rates 19 times, which means 84.4 percent of all decisions about monetary policy have favored easing, up from 74 percent at the end of the second quarter.

As an illustration of the speed with which central banks loosened their policy in the third quarter, 18 central banks, including the U.S., Brazil and Russia, cut rates twice while two central banks, Indonesia and Paraguay, cut rates three times.

For a detailed list of countries that changed their monetary policy stance in 2019, please click on “Easier or Tighter,” for a country-by-country overview of changes to monetary policy by the 96 central banks followed by Central Bank News. EARLIER YEARS 2018: 43 central banks tightened monetary policy and 32 eased, global net tightening of 11 2017: 28 central banks tightened monetary policy and 34 eased, global net easing of 6 2016: 29 central banks tightened monetary policy and 46 eased, global net easing of 17 2015: 48 central banks tightened monetary policy and 34 eased, global net tightening of 14

Tomorrow we have the last major bit of data for the week, which could set the trend for the next couple of days.

Inflation is one of the key data points tracked by the SNB, so it gets a lot of attention. That being said, the central bank in Switzerland is not due to meet until December. And this leaves the currency to move on its own.

CPI in Switzerland hasn’t been near the SNB’s target in years. In fact, it has been trickling lower since peaking in mid-2018.

The move is in conjunction with a slowing economy and increasing demand for safe havens that have pushed up the value of the currency and made life difficult for exporters.

The market appears to have internalized the reality of low inflation staying low for a long time.

What We Are Looking For

The market tends to focus on the monthly CPI figure, which is expected to increase slightly to 0.1% from 0.0% prior.

Low as it is, it’s still an improvement over repeated negative rates that have been the most common since the economic slump began late last year. At these low rates, just a decimal or two difference can have a big impact. The market reacts to relatively small changes.

Expectations are for annualized CPI to be just 0.2%, a decrease from 0.3% in the prior month. This would be the slowest growth since late 2017.

Negative inflation (deflation) is a common occurrence in Switzerland, usually in times of global economic stress. While such a low inflation rate in most other countries would have the central bank scrambling, the SNB is more sanguine.

Unlike any other currency, the Swiss franc is still backed by gold. Around 20% of their money supply is tied to the yellow metal. This means that inflation and deflation comes not just from economic situations, but also from changes in the price of gold.

As the trade war continues and the global economic outlook remains uncertain, gold has been climbing since last October. This is putting pressure on Swiss inflation.

In the meantime, large foreign cash flows seeking a safe haven have put pressure on the value of the Swiss Franc, diminishing the cost of imported goods.

Money is Scarce

On the demand side, a recent survey of managers showed that Swiss businesses are planning to raise wages by an average of just 1% this year.

Given the SNB’s expectation of inflation, that would imply a real increase of 0.8%, and slightly below the long-term average. This lower than average increase in income will lead to less inflationary pressure both this year and next.

It might be one more bit of evidence that the SNB needs to redouble its efforts to support price increases.

The thing is, though, there is a growing consensus that negative rates are not effective in the current circumstances and no substitute for fiscal reforms.

And to make matters worse, most of their economic problems are imported from their neighbors and largest trade partners. Recent reports are showing slowing manufacturing output, and it’s likely to remain low. So, there isn’t much to drive inflation higher in the near future.