On Tuesday the 22nd of October, trading on the euro closed down. Trading on the US dollar was mixed during the European session, which was brought about by uncertainty over Brexit on the eve of a crucial vote on the withdrawal agreement by the British parliament. The euro dropped to 1.1123 before recovering to 1.1154.

Towards the end of the day, the pound slumped after British lawmakers rejected the government’s Brexit timetable. This sent the euro down to 1.1118.

Day’s news (GMT+3):

15:30 Canada: wholesale sales (Aug).

16:00 US: housing price index (Aug).

17:00 Eurozone: consumer confidence (Oct).

17:30 US: EIA crude oil stocks change (18 Oct).

Current situation:

On Tuesday, we were expecting a breakout of the trend line during the US session. The bears broke through it at the beginning of the European session. At the time of writing, the euro is trading at 1.1118. A downwards channel has formed. Since the stochastic oscillator is looking up, we expect the pair to rise to the upper line of the downwards channel (22nd degree at 1.1140) at the beginning of today’s European session. In the US session, we expect the pair to drop to 1.1087.

Why should the rate gather downwards momentum after 1.1110?

On the 17th of October, the range of 1.1085 to 1.1110 acted as a sort of destabilisation zone. Bulls passed through this range very quickly, and in some places there were very low trading volumes. As such, if 1.1110 doesn’t manage to withstand the bears, the pair will quickly fall to 1.11087, which would cover the destabilisation zone judging by the volume profile from the 17th of October.

Trading is currently being dictated by developments on Brexit as well as on the US-China trade deal. Investors expect the UK to exit the EU with a deal, and for Trump to conclude a trade agreement with China. Le Yucheng, the Chinese Executive Vice-Minister of Foreign Affairs, has announced that China and the US have made significant progress in the trade talks.

When the pair reaches the balance line, the upper line of the channel, and the 22nd degree, we need to keep an eye on the crosses. If they are rising at the time, then of course it’s best to refrain from shorting the euro. Since the trend is still bullish, we should wait for a signal at around 1.1140 to go short. Unless this happens, selling is a risk, so one should either wait, or trade with limited volumes.

Asian stocks are mixed after US equities posted declines, as Brexit risks took hold of market sentiment in the absence of other major catalysts. With investors keeping risk appetites in check, most Asian currencies are weaker against the US Dollar, but are gaining versus the Pound. Gold is inching towards the $1490 psychological level, while 10-year US Treasury yields extended yesterday’s declines to drop below 1.75 percent at the time of writing.

GBPUSD returned to sub-1.29 levels after the UK Parliament blocked Prime Minister Boris Johnson’s pledge to deliver Brexit by October 31. However, the much-feared no-deal Brexit now appears a lessened prospect, hence the mitigated drop in Sterling.

Despite Parliament agreeing to the general principles of PM Johnson’s Brexit deal for now, the exact date for the UK’s departure from the EU is still up in the air. There appears to be ambitions among MPs to improve on the deal in hand, which could still sway the political support for the deal either way. The longer runway that’s been accorded this Brexit saga also means that investors may have to contend with more political risks by way of a UK election. Given the various potential political outcomes, future gains for Sterling are not assured, with politically-driven volatility set to be a recurring theme for GBPUSD.

Incoming US economic data to help stabilise Dollar

The Dollar index (DXY) gained 0.3 percent and climbed back above its 200-day moving average, aided by the Pound’s drop, with Sterling playing its role as the primary driver for DXY in recent days.

The Greenback could see more support over the coming days, provided the incoming US economic data such as factory orders, jobless claims and consumer sentiment do not stray too far from market expectations. Investors are now forecasting a 91.5 percent chance that the Federal Reserve will lower US interest rates by 25 basis points next week. A signed US-China trade deal in November may take some pressure off certain sectors of the US economy, which could allow the Fed to back away from further policy easing after this month.

Brent futures briefly breached $60/bbl before moderating, following a report that OPEC producers are mulling deeper supply cuts at their next meeting. Considering that US shale output remains at record levels while global demand is expected to wane next year, tighter OPEC production would be welcomed by Oil bulls as such a move may translate into higher prices for Brent.

Brent has not been able to take full advantage of the weaker Dollar this month, when comparing its meagre 0.3 percent month-to-date rise versus the Dollar index’s 1.9 percent decline during the same period. Oil continues to be weighed down by dogged concerns over diminishing global demand, and will need all the help it can get if prices are to climb meaningfully higher.

Disclaimer: The content in this article comprises personal opinions and should not be construed as containing personal and/or other investment advice and/or an offer of and/or solicitation for any transactions in financial instruments and/or a guarantee and/or prediction of future performance. ForexTime (FXTM), its affiliates, agents, directors, officers or employees do not guarantee the accuracy, validity, timeliness or completeness, of any information or data made available and assume no liability as to any loss arising from any investment based on the same.

Sterling was injected with another dose of volatility on Tuesday evening after British MP’s rejected a timetable for Boris Johnson’s Brexit deal by 322 to 308.

It followed the House of Commons passing a vote allowing the prime minister’s Withdrawal Agreement Bill to proceed to the next stage. The government losing this key vote on the Brexit timetable will make it incredibly difficult for Johnson to fulfil his “do or die” pledge to remove Britain out of the European Union on October 31st. With more delays, drama and uncertainty expected as the Brexit deadline looms, the path of least resistance for Sterling points south. This negative sentiment is already being reflected in the GBPUSD which is trading around 1.2870 as of writing. Until proper clarity and direction are provided on Brexit, the GBPUSD is poised to test 1.2800 and 1.2700, respectively.

Looking at the technical picture, Sterling bulls are losing some steam on the daily charts with 1.3000 acting as a strong resistance level. Sustained weakness below 1.3000 should encourage a decline back towards 1.2800. Although the GBPUSD is building momentum on the weekly charts, this could be reversed if bears can secure a weekly close below 1.2700.

Disclaimer: The content in this article comprises personal opinions and should not be construed as containing personal and/or other investment advice and/or an offer of and/or solicitation for any transactions in financial instruments and/or a guarantee and/or prediction of future performance. ForexTime (FXTM), its affiliates, agents, directors, officers or employees do not guarantee the accuracy, validity, timeliness or completeness, of any information or data made available and assume no liability as to any loss arising from any investment based on the same.

US stocks pulled back on Tuesday after weak earnings reports. The S&P 500 lost 0.4% to 2995.99. The Dow Jones industrial average slid 0.2% to 26788.10 as heavy losses from McDonald’s and Travelers on earnings misses outweighed United Technologies and Procter & Gamble gains. Nasdaq fell 0.7% to 8104.30. The dollar weakening reversed after Richmond Fed Manufacturing Index surprise improvement for October while Existing Home Sales fell more than expected in September. The live dollar index data show the ICE US Dollar index, a measure of the dollar’s strength against a basket of six rival currencies, rose 0.2% to 97.52 and is higher currently. Stock index futures point to lower openings today.

FTSE 100 biggest winner among European indexes

European stocks extended gains on Tuesday. The GBP/USD joined EUR/USD’s decline with both pairs higher currently. The Stoxx Europe 600 ended 0.1% higher led by energy stocks. The German DAX 30 edged up 0.1% to 12754.69. France’s CAC 40 advanced 0.2%. UK’s FTSE 100 rose 0.7% to 7212.49 as UK parliament voted to consider Prime Minister Boris Johnson’s Brexit plan but rejected his rapid timetable for approval.

Asian indexes retreat while Australia’s All Ordinaries Index edges higher

Asian stock indices are mixed today. Nikkei rose 0.3% to 22625.38 as yen continued its climb against the dollar. Chinese stocks are falling as reports late Tuesday indicated China plans to replace Hong Kong administrator by March: the Shanghai Composite Index is down 0.4% and Hong Kong’s Hang Seng index is 1% lower. Australia’s All Ordinaries Index edged up 0.01% as Australian dollar continued sliding against the greenback.

Brent futures prices are edging lower today. Prices rose yesterday on reports Organization of the Petroleum Exporting Countries consider making further reductions to crude output when they meet in December. Trade group the American Petroleum Institute late Tuesday report indicated US crude supplies rose by 4.45 million barrels last week. December Brent rose 1.3% to $59.70 a barrel on Tuesday. Today at 16:30 CET the Energy Information Administration will release US Crude Oil Inventories.

Note: This overview has an informative and tutorial character and is published for free. All the data, included in the overview, are received from public sources, recognized as more or less reliable. Moreover, there is no guarantee that the indicated information is full and precise. Overviews are not updated. The whole information in each overview, including opinion, indicators, charts and anything else, is provided only for familiarization purposes and is not financial advice or а recommendation. The whole text and its any part, as well as the charts cannot be considered as an offer to make a deal with any asset. IFC Markets and its employees under any circumstances are not liable for any action taken by someone else during or after reading the overview.

The factors at play in the company’s recent quarterly output are provided in a Pareto Securities report.

In an Oct. 18 research note, analyst Tom Erik Kristiansen reported that Pareto Securities expects Equinor ASA (EQNR:NYSE; EQNR:Oslo) to report a weak Q3/19, but that “could offer an attractive buying opportunity ahead of Sverdrup production impacting reported earnings and with European gas prices also being a recent positive (up 20% month over month).”

Kristiansen noted the indicators that Equinor will post a dampened Q3/19 even if it were to decrease its 2019 capex. For one, the company’s Norwegian natural gas production was down in September more than 30% from the average.

Two, prices continued to be low.

Three, output expectations for its international business in Q3/19 also are reduced. “We estimate adjusted EBIT of US$2.5 billion, 6% below consensus,” the analyst noted.

Kristiansen concluded with, “We have not changed our long-term positive view on Equinor.” Thus, Pareto has a Buy rating and an NOK210 per share price target on the energy company.

Disclosure: 1) Doresa Banning compiled this article for Streetwise Reports LLC and provides services to Streetwise Reports as an independent contractor. She or members of her household own securities of the following companies mentioned in the article: None. She or members of her household are paid by the following companies mentioned in this article: None. 2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. 3) Comments and opinions expressed are those of the specific experts and not of Streetwise Reports or its officers. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. 4) The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases.

Disclosures from Pareto Securities AS, Equinor, October 18, 2019

This publication or report has been prepared solely by Pareto Securities Research.

Opinions or suggestions from Pareto Securities Research may deviate from recommendations or opinions presented by other departments or companies in the Pareto Securities Group. The reason may typically be the result of differing time horizons, methodologies, contexts or other factors.

Analysts Certification The research analyst(s) whose name(s) appear on research reports prepared by Pareto Securities Research certify that: (i) all of the views expressed in the research report accurately reflect their personal views about the subject security or issuer, and (ii) no part of the research analysts compensation was, is, or will be directly or indirectly related to the specific recommendations or views expressed by the research analysts in research reports that are prepared by Pareto Securities Research.

The research analysts whose names appears on research reports prepared by Pareto Securities Research received compensation that is based upon various factors including Pareto Securities total revenues, a portion of which are generated by Pareto Securities investment banking activities.

Conflicts of interest

Companies in the Pareto Securities Group, affiliates or staff of companies in the Pareto Securities Group, may perform services for, solicit business from, make a market in, hold long or short positions in, or otherwise be interested in the investments (including derivatives) of any company mentioned in the publication or report.

In addition Pareto Securities Group, or affiliates, may from time to time have a broking, advisory or other relationship with a company which is the subject of or referred to in the relevant Research, including acting as that companys official or sponsoring broker and providing corporate finance or other financial services. It is the policy of Pareto to seek to act as corporate adviser or broker to some of the companies which are covered by Pareto Securities Research. Accordingly companies covered in any Research may be the subject of marketing initiatives by the Corporate Finance Department.

To limit possible conflicts of interest and counter the abuse of inside knowledge, the analysts of Pareto Securities Research are subject to internal rules on sound ethical conduct, the management of inside information, handling of unpublished research material, contact with other units of the Group Companies and personal account dealing. The internal rules have been prepared in accordance with applicable legislation and relevant industry standards. The object of the internal rules is for example to ensure that no analyst will abuse or cause others to abuse confidential information. It is the policy of Pareto Securities Research that no link exists between revenues from capital markets activities and individual analyst remuneration. The Group Companies are members of national stockbrokers associations in each of the countries in which the Group Companies have their head offices. Internal rules have been developed in accordance with recommendations issued by the stockbrokers associations.

This material has been prepared following the Pareto Securities Conflict of Interest Policy. The guidelines in the policy include rules and measures aimed at achieving a sufficient degree of independence between various departments, business areas and sub-business areas within the Pareto Securities Group in order to, as far as possible, avoid conflicts of interest from arising between such departments, business areas and sub-business areas as well as their customers. One purpose of such measures is to restrict the flow of information between certain business areas and sub-business areas within the Pareto Securities Group, where conflicts of interest may arise and to safeguard the impartialness of the employees. For example, the Corporate Finance departments and certain other departments included in the Pareto Securities Group are surrounded by arrangements, so-called Chinese Walls, to restrict the flows of sensitive information from such departments. The internal guidelines also include, without limitation, rules aimed at securing the impartialness of, e.g., analysts working in the Pareto Securities Research departments, restrictions with regard to the remuneration paid to such analysts, requirements with respect to the independence of analysts from other departments within the Pareto Securities Group rules concerning contacts with covered companies and rules concerning personal account trading carried out by analysts.

The details of this study and a second one are outlined in a ROTH Capital Partners report.

In an Oct. 16 research note, ROTH Capital Partners analyst Jerry Isaacson reported that Matinas BioPharma Holdings Inc. (MTNB:NYSE.American) launched its first clinical trial of MAT2203, for the treatment of cryptococcal meningitis.

MAT2203 is Matinas’ oral formulation of the approved antifungal amphotericin B using the biopharma’s lipid nanocrystal delivery (LNC). “LNC allows delivery of this drug, which has a difficult adverse effects profile, with fewer side effects, which may allow higher doses and extended use compared to current formulations,” Isaacson explained.

He noted that in the study, MAT2203 will be evaluated as both an induction and maintenance therapy for HIV patients with cryptococcal meningitis. In part 1 of the trial, MAT2203 will be tested in HIV-infected patients without cryptococcal pneumonitis to determine the maximum tolerated dose. In part 2, which will be randomized, MAT2203 will be evaluated against intravenous amphotericin B.

Preliminary results could be available by year-end 2019, Isaacson wrote. MAT2203 has orphan drug status as a cryptococcosis treatment and a qualified infectious disease product designation with the U.S. Food and Drug Administration.

Isaacson indicated that a second clinical trial for MAT2203 is planned, and Matinas started screening patients for it, aiming for 70 enrollees. In this study, MAT2203 will be compared to Vascepa. With the trial expected to start in Q1/20, data could be ready by Q4/20.

ROTH has a Buy rating and a $4 per share target price on Matinas. For that valuation, the investment banking firm assumes MAT9001 approval in 2023 and an estimated $400 million in sales in 2029. Matinas’ stock is currently trading at around $0.70 per share.

Disclosure: 1) Doresa Banning compiled this article for Streetwise Reports LLC and provides services to Streetwise Reports as an independent contractor. She or members of her household own securities of the following companies mentioned in the article: None. She or members of her household are paid by the following companies mentioned in this article: None. 2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. 3) Comments and opinions expressed are those of the specific experts and not of Streetwise Reports or its officers. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. 4) The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases.

Disclosures from ROTH Capital Partners, Matinas BioPharma Holdings Inc., Company Note, October 16, 2019

Regulation Analyst Certification (“Reg AC”): The research analyst primarily responsible for the content of this report certifies the following under Reg AC: I hereby certify that all views expressed in this report accurately reflect my personal views about the subject company or companies and its or their securities. I also certify that no part of my compensation was, is or will be, directly or indirectly, related to the specific recommendations or views expressed in this report.

ROTH makes a market in shares of Matinas BioPharma Holdings, Inc. and Amarin Corporation plc and as such, buys and sells from customers on a principal basis. A Research Analyst and/or a member of the Analyst’s household own(s) debt or equity securities of Matinas BioPharma Holdings, Inc. and Amarin Corporation plc stock. Shares of Matinas BioPharma Holdings, Inc. may be subject to the Securities and Exchange Commission’s Penny Stock Rules, which may set forth sales practice requirements for certain low-priced securities. Within the last twelve months, ROTH has received compensation for non-investment banking securities-related services from Matinas BioPharma Holdings, Inc. Within the last twelve months, ROTH has received compensation for investment banking services from Amarin Corporation plc. Within the last twelve months, ROTH has managed or co-managed a public offering for Amarin Corporation plc.

ROTH Capital Partners, LLC expects to receive or intends to seek compensation for investment banking or other business relationships with the covered companies mentioned in this report in the next three months.

Sector expert Michael Ballanger reflects on modern monetary policy and discusses his most recent investment decisions.

You have all heard me opine about the (un)dependability of rules-based investing in a managed market environment, where it is not kosher for a financial advisor to fire off a promotional tweet about their favorite stock but it is perfectly acceptable for a sitting president to fire off twelve tweets in a morning guaranteeing a “China trade deal” with the intent of triggering a torrent of algobot buy orders. The Twitterverse is rife with people like yours truly, who make a living out of attempting, sometimes successfully and other times abysmally, to provide followers with the slightest of “edge” with which to trade and competeand that’s fineexcept where the author of the newsletter or tweet or e-mail blast actually believes that the “research” or “system” or “data set” they are following or executing is in any way, shape or form responsible for the outcome.

I have a flash for all of those megalomaniacal gurus: In a managed market littered with the corpses of free market capitalists, winning trades are 99% the result of a majestic matriarch smiling down upon you while blessing your fortunes, and she goes by only one name: Lady Luck.

In my very early days as a trainee in the 1970s investment industry, I befriended a young man who had been successful in building a very respectable book of business in a very short period of time. I will refer to him as “Larry.” One day, after it was determined that I was too skilled as a “communicator” to stay and work on the bond desk in favor of “sales,” I aked Larry how he built his business. Now, Larry wore wonderfully tailored clothing that was at once both conservative and natty, but I had the distinct impression that the red silk bowtie he wore was a clue to his originality, because in 1977, nobody with a Bay Street job wore a silk bowtie. Probing into his formula for success, I asked him to give me his methodology for attracting clients, and this is what he told me.

“Get a list of really high-net-worth dumbass people that are terrified of gambling, typically doctors and dentists and farmers, who are too busy taking pulses or yanking molars or trudging through cow shit, and divide the list in half. Then take two of the most speculative penny resource stocks and assign the first stock to the first half of your dumbasses, then the second screamer to the second half. Get your pitch down to perfection on both stocks to the point where they both look like no-brainers. Then take the next week calling the two lists and making the pitches. Repeat this every week for a month and now you have eight groups to contact with a follow-up call.”

“Brilliant!” I shouted, rising from my chair in my private “Eureka” moment. As I readied myself for departure, Larry quickly grabbed my suspenders and sat me right back down and said, “But you haven’t heard the best yet. . .

“After both of your dumbass groups have heard the pitch, wait a month and then take a photocopy of the two share prices. One will be up sharply, with the other probably down the same amount. Take the list that wwas pitched the winner and separate it from the list that was pitched the loser. Take the loser list and sell it to the rookie broker in the next cubicle. Take the winner list and proceed to call them with the next ‘big winner.’ After they all open new accounts and give you all of their relatives’ contact info, proceed to repeat the process.”

All I could muster after hearing Larry’s motivational lesson was a blank stare. As I struggled to try to feign awe at his message, I found myself confronting one of the great conundrums of the financial services industry. It all boils down to being a “numbers game.” Whether you are a rookie stock salesman trying to woo new clients or billionaire money manager Ken Fisher describing his prowess with women and “the wealthy,” if you are an average money manager but a superb marketer, you will be seen as a genius by way of your assets undermanagement as opposed to your financial acumen.

Now, if you are the chairman of the Federal Reserve Board, Jerome Powell, and you have just decided that your 2018 attempt at normalizing (shrinking) your balance sheet was a ghastly mistake, you now decide that “liquidity issues” (like Deutsche Bank’ $46 trillion derivative book) demand that you inject $250 billion back into the system (after just removing it). You explain that we should not view the action as “quantitative easing (QE), but rather as a something other than that. Now, since the commutative property of arithmetic says that if a = b, and b = c, then a = c, if “adding liquidity” = “the phony creation of money out of thin air with the wave of a magic wand,” and “the phony creation of money out of thin air with the wave of a magic wand” = QE, then “adding liquidity” must equal QE. Ergo, what we have today is QE. It is not something other than QE; it is the “phony creation of money,” and if you or I were to do that in our basements, we would be incarcerated for counterfeiting.

When stock markets smell counterfeiting, they usually rise sharply because, as you have all read here countless times, one should never underestimate the replacement power of equities within an inflationary spiral. Now, for the CNBC guest commentator that counters my argument with “but there is no inflation!”, I volley back with this: The creation of $250 billion in POMO (permanent open market operations) is monetary inflation of the highest order. It is money printing and while it may be several trillion dollars less than the amount they used to bail out the criminal banks in 2009, it is still the same bubble-forming cocktail of bank-friendly “liquidity” that allowed their precious real estate collateral to recover while injecting steroids, amphetamines and hallucinogens into the global stock markets.

Most importantly, take all of the people who loves stocks and give them the “not QE” pitch, and then repeat for all of the seniors and savers and non-stock-investing citizens. Keep the former, and then sell the list of seniors and savers and non-stock-investing citizens to the rookie central banker in the next cubicle. Rinse and repeat and voila! No more financial crisis, ever. Isn’t investing just grand?

Gold prices appear to be doing exactly what I feared back on Sept. 4; they are correcting. Having formed a near-perfect head-and-shoulders top in the mid-August to mid-September period, we were gradually working off the massively overbought conditions of July-August. Then the central planners swooped into action, using interventions and interference to paint an ugly tape complete with blurry images of a “blow-off top” and the dreaded “head-and-shoulders top” formation.

It only took an expansion of about 150,000 contracts to the aggregate net short position of the Commercial traders to dull the advance and turn the Large Specs from buyers to sellers. Since those contracts are really only “hedges” put on by producers, that makes the manipulation both believable and legitimate. Additionally, since the gold prices went through the roof back in 20092011 after the initiation of the first QE, gold cannot make the same move because Jay Powell assures you and me that this $250 billion liquidity ejaculation is really not QE. And because the algobots and the dumbass money managers believe him, the gold correction continues.

Notwithstanding the obvious sarcasm, this current backfilling in the gold chart is both a frustration for the diehard bulls, whose gnarling and gnashing of teeth are largely underappreciated, but also blessing for the patient bulls who took advantage of the mania of late-August/early September, removing a few well-earned chips from the table. Falling firmly into the latter category, I have replaced the unleveraged gold ETFs (GDX/GDXJ), while I am lining up reentry into the leveraged ETFs (NUGT/JNUG) with bids under the market. Judging from the relative strength index (RSI)/moving average convergence-divergence (MACD)/histogram setups, December gold is approaching the 30 oversold status last seen back in August 2018. If I can wager a guess, it should be later this month that we get the final flush that sets up the trade. No guarantees but a definite possibility. . .

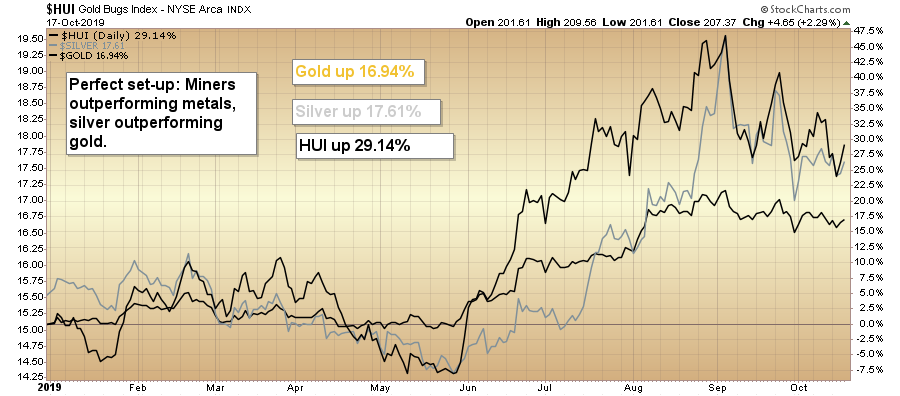

Silver is currently sitting 11.24% from the top, identified in this publication on Sept. 4 at $19.75, and is therefore solidly in correction mode. But as is normally the case with silver, it tends to have exaggerated moves once it gets “discovered” by the newbies. Despite the sharp pullback, it looks a tad healthier from a technical perspective than gold, and therefore the recommended short of the gold-to-silver ratio (GSR) from last July at 92.40 remains intact, with a 60 target some time in 2020.

I am currently long the December $18 calls from $0.23 (currently $0.22), and have enough buying power to quadruple the position at the optimum time. I expect silver to outperform gold over the balance of 2019 and well into 2020. If there is to be a surprise in Q4/2019, it will be a plunge in the GSR, accompanied by a piercing upside probe by silver. I base this on the high levels of negative sentiment still despite the shiny metal up 13.36% year-to-date, a respectable showing by any measure.

As you all know, I let the relative performance of the assets that exist in my world do the talking. It is like the “Dow Theory” of precious metals investing, where one component either outperforms or underperforms relative to another, setting up possible confirmations or non-confirmations of the bull or bear case. In our space, the mining stocks absolutely must outperform the metals for there to be a bona fide bull market in the mining shares, but there have been rare occurrences where mining shares reacted to gold-friendly events in odd ways, such as in the 1987 market crash and the 2008 market crash, where liquidity needs sent the entire investing worlds to the sidelines in search of safety.

The absolute worst scenario of all for us is when consumer prices finally react to monetary inflation and begin spiraling upward. All inflation in every form comes as a result of reckless disrespect for savers, and arrives on sanctimonious platter of bull delivered with great fanfare by the bankers who would have us believe in their roles as saviors.

The banks are not today, nor have they ever in the past been, saviors. They have always been opportunists and they have always been an integral part of the politico-military-industrialist cabal that runs the world. Banks are exquisitely trained “middlemen,” toiling in the insidious underbelly of world politics. As such, just as cockroaches fear the light, bankers fear gold, the ultimate harbinger of doom for the paperhangers.

The key to this counterfeiting exercise lies in secrecy and subterfuge. As long as the public is led to believe that inflation is “muted,” then the distraction of trade wars and deficits serve to deflect the public mood away from the root problem of unresolvable debt and ultimate sovereign insolvency.

My hero in the newsletter business was the late and infinitely great Richard Russell, who always beseeched his subscribers to “follow the money,” because at the end of every news event was an indefatigable trail leading to money. Just as we all learned in the pages of Atlas Shrugged, the outcome of exaggerated largesse in the form of patronage always manifests itself within the Halls of Political Crime, with the ultimate victims being the Middle Class, the ripest target in all of socio-economic history for plunder.

The irony here in 2019, soon to be 2020, is that since the 1990 release of the visionary work by John Naisbitt, Megatrends, in which he predicted the ascendancy of China’s populace from poverty to the middle class status, the Western middle class, once the envy of the world and led by the American production machine, has now been replaced by a rising and far-more-powerful Chinese middle class, whose existence was largely denied through 5,000 years of history. The arrival is now not only complete, but also a definable threat to the standards of living for the rest of the non-Chinese world.

When I get into discussions with people over China, the older generation, of which I am a member, tend to fall into agreement with me in my assessment of the risks associated with allowing “invasive species” into any ecosystem. The younger generation accuse me of being a racist, intolerant of non-Caucasian immigrants to Canada and an incendiary voice in the racial debate.

Quite on the contrary, I am a historian, well learned in the outcome of unintended consequences. If a European rabbit is introduced into a Australian habitat, where no natural predators exist, vegetation will cease to thrive as the overabundance of rabbits will alter the ecosystem in a negative manner. Similarly, if you allow a culture that is the cultivator of the largest pollution machine ever created in the history of mankind (China), to spread to continents like North America, with attitudinal conditioning that carries little, if any, regard for dealing with garbage bags, you are, by default, welcoming their wealth (in selling them the $35,000 house you bought in Scarborough in 1964 for $925,000). But without conditions. When money governs the debate, there are no “conditions.” And that is the problem facing us all. As Richard would say, in the China debate, were he still around, “Follow the money.”

I want to own the mining shares for the majesty of bull moves such as the one we experienced in the middle part of 2019, but I do not want to own them when “majesty” turns to “mimicry,” and hundreds of cannabis and crypto bloggers descend upon the Twitterverse claiming to be the first to have “called the bottom.” You want to wait until their Ritalin runs out and they flip on to their next deal, so that you can buy at the bottom what they bought at the top. Pretty easy stuff. . .

Before I launch myself into an invective concerning the U.S. equity markets, let me state for the record that I am the walking embodiment of the “anti-Kudlow”; I love gold and I hate stocks. However, Larry Kudlow is far more important than I could ever dream to be. Therefore, he has the innate ability to tell Donald Trump to “press the button,” and by that I do not refer to the nuclear button so popularized in the Cold War movies such as Dr. Strangelove and Fail Safe.

The United States National Security Agency has been empowered to ensure that stocks remain a key component of the U.S. citizens’ “security” and, as such, they must remain elevated at all times. Rather than drop cash from helicopters, the American banking cartel has trained the American investor class in the well-honed art of “Buying the Effing Dip.” By doing so, they have turned the socialist habit of wealth distributionan inverse financial Robin Hood of taking from the poor and giving to the richinto a capitalist video game where no matter what happens, you are going to be handed a windfall by the government.

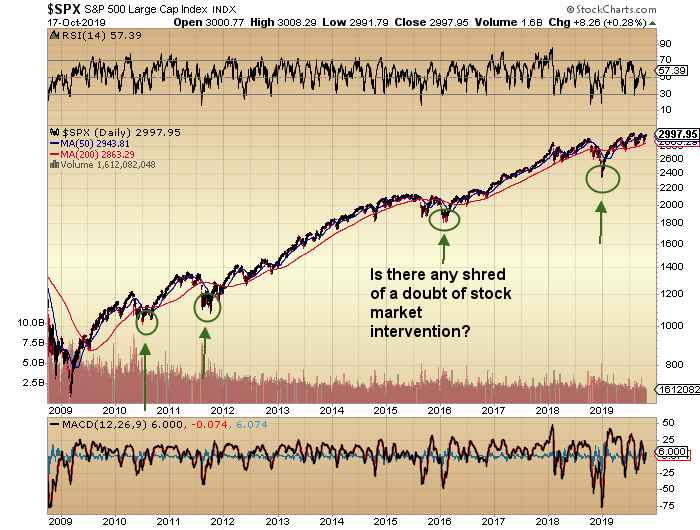

The “button” is the Working Group on Capital Markets, and the finger is the Secretary of the Treasury, Stevie Mnuchin, who openly admitted last Dec. 22 that he was calling a meeting of the Working Group (otherwise known as the “Plunge Protection Team” or PPT) in order to “calm” the markets, which had been in a kamikaze dive of terrifying proportion. Needless to say, that was with the S&P at 2,346 and here we are, a mere ten months later, at 2,977.95 despite the global economic slowdown, emergency REPO actions, POMO, impeachment proceedings and astronomical debt levels everywhere.

Now that strikes me as somewhat bizarre. Before you allow your intractable bearish leanings to play out in the form of “getting short,” think twice.

Maniacal rants set aside, history would show that purchases of common stocks during the last two weeks of October have proven to be the most timely of purchases for the investor class. Going into an election year, you can bet that DJT will be wearing out the Tweet button with stock-friendly color commentary on a par with Kudlow and Cramer (or any regional Fed governor).

So, for a gold bull and stock bear, the evidence is ample enough to trigger a put-buying extravaganza, along with a basket of shorts on your favorite growth (pumped) stocks, especially for the Millennials out there whose terminal case of recency bias has them planning for the same air pocket that they experienced this time last year.

The problem remains, for the bears, that sentiment is really not that ebullient, with AAII reporting only 20.3% bulls versus 44% bears. In terms of sentiment, this is not a setup where puts and shorts will be rewarded. What we bears need is a rip-roaring breakout to all-time highs that swings the AAII needle to 50-60% bulls, after which valuations will be in nosebleed territory and the probability of winning vastly improved.

As I wrote in September, I have the feeling that the PPT, with DJT at the helm, is going to go all-out in making damn sure that we have a booming stock market going into 2020, so that his re-election chances don’t suffer from the “It’s the economy, stupid” misfortune suffered by George Bush in his reelection run against Bill Clinton. This time, DJT will be in the “It’s the S&P, stupid” frame of mind, as he waves the magic wand of presidential authority over the American stock indices and also over the metals markets. Rampaging gold and silver will be a distraction for the voting public, and that is not good, with The Donald screaming and shouting and waving his arms as he points to the all-time high on the S&P.

Lastly, I have recently invested in two juniors that have defined resources of gold and/or silver, Aftermath Silver Ltd. (AAG:TSX.V) and Goldcliff Resource Corp. (GCN:TSX.V) I did so because, in addition to their exploration potential, their properties had defined resources of either gold or silver or both.

As I wrote about last summer, to have called the gold and silver rally as accurately as I did this year, with enormous gains in the miner ETFs, GLD and SLV call options, and the physical metals themselvesonly to see the junior explorcos in the portfolio (Getchell Gold Corp. [GTCH:CSE] and Stakeholder Gold Corp. [SRC:TSX.V]) stay absolutely dead in the water despite breathtaking advances in companies like Great Bear Resources Ltd. (GBR:TSX.V; GTBDF:OTCQX) ($2.33 to $9.04)was for me, a sore point. To be so right, and at the same time so wrong, because I was right in theory but wrong in execution, is maddening.

Markets rewarded every miner on the board except those looking for metal. Accordingly, it is with great delight that Getchell Gold yesterday announced the acquisition of the Fondaway property in Nevada, which brings over one million ounces of gold to GTCH for less than 20% dilution and a manageable cash cost. Getchell management must have been reading my words of frustration last summer, because after they drilled their #1 target (Hot Springs Peak) and discovered that the massive IP anomaly was devoid of gold and/or silver, they put the drills away and focused totally on securing an asset that will serve to underpin GTCH’s share price to the movement of the gold price.

Now, unlike last year, the company can see upside from three areas: 1) gold price advances; 2) exploration success; and 3) reclassification of the resource. At CA$0.11, assuming 20% dilution on top of the 52 million shares (f.d.) already issued, Getchell is priced at $7.21 per ounce of gold (Kitco uses $40/ounce as the benchmark). Therein lies the opportunity for value-driven gold bulls.

This transaction is reminiscent of the late ’70s, when I was shown a little silver company that had a small resource in the Yukon but with a production cost around $15 per ounce of silver. In 1978, with silver at $6 per ounce, nobody dared take a stab at the little junior, but at $0.25 per share, my grey-haired, cigar-chomping, whiskey-drinking mentors were inhaling the stock for a four-month period (as was I). After that, silver did a funny thing: it took off. In late ’79 with the Hunt brothers trying to corner the silver market, prices exploded into the $20s, then $30s and finally $50, during which time, we were serving up steaming helpings of our little silver deal at prices north of $20 per share.

You see, that sub-economic silver deposit in 1978 got “skated onside” by the underlying commodity, and that is doubly exciting for Getchell and the Fondaway property, because it is already advanced far enough that a preliminary economic assessment will be just around the corner, with only a smattering of drilling required.

The setup is ideal for the gold bull, because GTCH offers tremendous leverage to the gold price, along with a tremendous land package, all within the Getchell Trend of Nevada, which will be important when sentiment goes “crypto-weed” and explorcos finally become the darlings of the Millennials.

I’ll have another portfolio update after month-end with a few significant changes, so until then, you can follow my vitriolic rampages on Twitter (@Miningjunkie), which provide, from time to time, equal dollops of humor and trading ideas, as well as exotic recipes for self-medication and recreational delight.

Originally trained during the inflationary 1970s, Michael Ballanger is a graduate of Saint Louis University where he earned a Bachelor of Science in finance and a Bachelor of Art in marketing before completing post-graduate work at the Wharton School of Finance. With more than 30 years of experience as a junior mining and exploration specialist, as well as a solid background in corporate finance, Ballanger’s adherence to the concept of “Hard Assets” allows him to focus the practice on selecting opportunities in the global resource sector with emphasis on the precious metals exploration and development sector. Ballanger takes great pleasure in visiting mineral properties around the globe in the never-ending hunt for early-stage opportunities.

Disclosure: 1) Michael J. Ballanger: I, or members of my immediate household or family, own securities of the following companies mentioned in this article: Aftermath Silver, Getchell, Goldcliff, Stakeholder, Great Bear. My company has a financial relationship with the following companies referred to in this article: None. I determined which companies would be included in this article based on my research and understanding of the sector. Additional disclosures are below. 2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: Great Bear Resources. Click here for important disclosures about sponsor fees. As of the date of this article, an affiliate of Streetwise Reports has a consulting relationship with Aftermath. Please click here for more information. 3) Statements and opinions expressed are the opinions of the author and not of Streetwise Reports or its officers. The author is wholly responsible for the validity of the statements. The author was not paid by Streetwise Reports for this article. Streetwise Reports was not paid by the author to publish or syndicate this article. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy. 4) This article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases. As of the date of this article, officers and/or employees of Streetwise Reports LLC (including members of their household) own securities of Aftermath Silver, Getchell, Goldcliff and Stakeholder, companies mentioned in this article.

Charts provided by the author.

Michael Ballanger Disclaimer: This letter makes no guarantee or warranty on the accuracy or completeness of the data provided. Nothing contained herein is intended or shall be deemed to be investment advice, implied or otherwise. This letter represents my views and replicates trades that I am making but nothing more than that. Always consult your registered advisor to assist you with your investments. I accept no liability for any loss arising from the use of the data contained on this letter. Options and junior mining stocks contain a high level of risk that may result in the loss of part or all invested capital and therefore are suitable for experienced and professional investors and traders only. One should be familiar with the risks involved in junior mining and options trading and we recommend consulting a financial adviser if you feel you do not understand the risks involved.

Shares of Halliburton Co. at times traded greater than 8% higher after the firm reported improved Q3/19 earnings results versus Q2/19.

This morning before the opening bell Halliburton Co. (HAL:NYSE)announced its third quarter earnings for the period ending September 30, 2019. The company reported net income of $295 million, or $0.34 per diluted share, during Q3/19. This compares to reported net income for Q2/19 of $75 million, or $0.09 per diluted share, and adjusted net income for Q2/19 of 303 million, or $0.35 per diluted share, excluding impairments and other charges. Operating income was $536 million during Q3/19, compared to reported operating income of $303 million and adjusted operating income of $550 million for Q2/19.

Jeff Miller, Halliburton’s chairman, CEO and president commented, “Our organization executed effectively in the third quarter. We managed the market dynamics and delivered our financial results as per expectations…Total company revenue was $5.6 billion and operating income was $536 million, representing decreases of 6% and 3%, respectively, compared to revenue and adjusted operating income in Q2/19…International revenue, which was flat sequentially, was up 10% year to date and we remain confident that we will achieve high single-digit international growth for all of 2019. International growth continues across multiple regions, benefitting both our Drilling and Evaluation and Completion and Production divisions…Our North America revenue decreased 11% sequentially driven by customer activity declines and the execution of our new playbook. I am proud of how our team performed in this challenging market. We are successfully implementing our new strategy and are focused on taking the right actions to deliver returns and cash flow for our shareholders…As the international recovery continues and the North American market matures, our strategy is allowing us to thrive in this dynamic environment, generate strong free cash flow and produce industry-leading returns.”

The company further outlined revenues by business segment in the report noting “Completion and Production revenue in Q3/19 was $3.5 billion, a decrease of $299 million, or 8%, when compared to Q2/19, while operating income was $446 million, a decrease of $24 million, or 5%…Drilling and Evaluation revenue in Q3/19 was $2.0 billion, a decrease of $81 million, or 4%, when compared to Q2/19, while operating income was $150 million, an increase of $5 million, or 3%.”

The firmed stated that North America revenue in Q3/19 decreased 11% to $2.9 billion compared to Q2/19 primarily due to lower activity and pricing in pressure pumping and well construction services in North America land.

The company indicated that although International revenue overall in Q3/19 was essentially flat at $2.6 billion compared to Q2/19, revenue in Latin America in Q3/19 increased 6% sequentially to $608 million primarily from higher activity in multiple product service lines in Argentina, increased testing activity and artificial lift sales across the region and improved fluids activity in Mexico. The firm also advised that Europe/Africa/CIS revenue in Q3/19 was $831 million, and was relatively unchanged when compared to Q2/19, and that Middle East/Asia revenue in Q3/19 decreased by 4% to $1.2 billion due to reduced project management and stimulation activity across the region.

Halliburton was founded in 1919 and is headquartered in Houston, Tex. The firm states it is one of the world’s largest providers of products and services to the energy industry with approximately 60,000 employees operating in more than 80 countries. The firm serves national and independent oil and natural gas companies and states that it helps its customers maximize value throughout the lifecycle of the reservoir from locating hydrocarbons and managing geological data, to drilling and formation evaluation, well construction and completion, and optimizing production throughout the life of the asset. The company operates through two business segments. Its Completion and Production segment delivers cementing, stimulation, intervention, pressure control, specialty chemicals, artificial lift and completion services, and its Drilling and Evaluation segment provides field and reservoir modeling, drilling, evaluation and wellbore placement solutions that enable customers to model, measure, drill and optimize their well construction activities.

Halliburton has a market capitalization of about $16.1 billion with approximately 875.9 million shares outstanding and a short interest of around 4.2%. HAL shares opened lower today at $18.15 (-$0.28, -1.52%) compared to Friday’s closing price of $18.43. The stock has traded today between $18.10 and $20.00/share and currently is trading at $19.78 (+$1.34, +7.27%).

Disclosure: 1) Stephen Hytha compiled this article for Streetwise Reports LLC and provides services to Streetwise Reports as an independent contractor. He or members of his household own securities of the following companies mentioned in the article: None. He or members of his household are paid by the following companies mentioned in this article: None. 2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. 3) Comments and opinions expressed are those of the specific experts and not of Streetwise Reports or its officers. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. 4) The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases.

As we near the end of October 2019, a very interesting price setup is taking place across many of the US market sectors recently. We only have a total of about seven trading days left in October 2019 and the Financial Sector ETF is rolling over with what appears to be an Engulfing Bearish price pattern near price channel highs. Additionally, the tech-heavy NASDAQ (NQ) has been mostly weaker compared to the ES and YM.

On September 30, 2019, we published this research post that highlighted why our predictive modeling systems suggested the S&P 500 and NASDAQ market sectors would become much more volatile than the Dow Jones Industrials: MODELING SUGGESTS BROAD MARKET ROTATION IN THE NQ & ES.

We believe this research is still very valid given the current price rotation near these price channel highs and given the potential that the Dow Jones stocks may become relatively stronger alternatives than the S&P 500 and NASDAQ sector stocks.

We believe a downside price rotation is setting up in the US and global stock markets and we believe the potential for large price moves exists in at-risk sectors like the Financials, Technology, Biotech, Energy, Services and other sectors that do not directly relate to what we feel are “essential consumer staples”. The Dow Jones Industrials Index is full of companies that traditionally perform better in a consumer-based economic contraction for investors – which is why we believe the YM will present a very unique opportunity going forward for skilled traders.

FAS Daily Chart, the Direxion Financial Bull ETF

This first FAS Daily Chart, the Direxion Financial BULL ETF highlights the price channel in YELLOW and highlights the recent price rotation near the $80 price level which constitutes a potential “new lower high” price rotation. Our longer-term cycle analysis tools predict a downside price move initiating over the next 7 to 10 trading days. We believe this new downside price trend could push price levels below the lower price channel level if this move is associated with external news or economic data that panics the markets.

IWM, Russell 2000 ETF, Daily Chart

This IWM, Russell 2000 ETF, Daily chart highlights an “island Doji top” formation that is setting up as a very unique price formation. When Doji type candles form with a gap above the previous bars, this is often considered an “island top” type of formation. Doji candles represent indecision and uncertainty. They are often found near-critical top and bottom formation. In this current formation, we believe the island top formation is a very clear warning that a major price top is setting up in the Mid-Caps which would also be considered a “new failed price high” formation. Ultimately, the $144.50 level becomes critical support if price falls.

SSO, ProShares Ultra S&P 500 ETF, Daily Chart

This SSO, ProShares Ultra S&P 500 ETF, Daily chart highlights a similar price range setup. Notice how all of these sectors have rotated into these ranges over the past few months – very similar to what happened in 2015/16 prior to the 2016 elections. We believe the uncertainty related to global trade, global economics and the US political “circus” will continue to put pricing pressure on the US stock market and global markets. We believe the inability to achieve “new price highs” throughout many sectors is a very clear warning that a larger downside price move, a type of price reversion, maybe setting up and we have been trying to warn our followers to be very cautious in taking unnecessary risks at this time while trading.

If our cycle research and predictive modeling systems are correct, we could be setting up for a downside price move that may act as a “true price exploration/reversion event” and potentially target levels that may be below the June 2019 lows. If this move is associated with some external news event or global crisis event, we may see prices fall to levels below the December 2018 low price levels.

Overall, we urge all skilled technical traders to stay very cautious over the next few months. Target solid trades that present very clear opportunities and properly position your trades to attempt to mitigate unknown risks. This is not the time to go “all-in” on anything as the markets are far more capable of being irrational than you are likely to be able to handle the risks that are associated with a crazy market move.

As a technical analysis and trader since 1997, I have been through a few bull/bear market cycles. I believe I have a good pulse on the market and timing key turning points for both short-term swing trading and long-term investment capital. The opportunities are massive/life-changing if handled properly.

I urge you visit my ETF Wealth Building Newsletter and if you like what I offer, join me with the 1-year subscription to lock in the lowest rate possible and ride my coattails as I navigate these financial market and build wealth while others lose nearly everything they own during the next financial crisis. Join Now and Get a Free 1oz Silver Bar!

NOTICE: Our free research does not constitute a trade recommendation or solicitation for our readers to take any action regarding this research. It is provided for educational purposes only. Our research team produces these research articles to share information with our followers/readers in an effort to try to keep you well informed. Visit our web site to learn how to take advantage of our members-only research and trading signals.

The British economy faces another agonising delay and UK financial assets will be further squeezed following the UK government losing another crucial Brexit vote in parliament.

This is the stark warning from the CEO and founder of one of the world’s largest independent financial advisory organizations.

The comments from Nigel Green of deVere Group come as Prime Minister Boris Johnson confirms the Brexit Withdrawal Agreement Bill “will now be paused” after MPs voted against the accelerated timetable for the Brexit Bill. The withdrawal is now subject to weeks of scrutiny.

It was the second vote of the night. The first was a win for Boris Johnson as MP’s supported his withdrawal agreement in principle. It was the first time MPs have shown their backing for any Brexit deal, and was a significant political boost for the Prime Minister.

Nigel Green states: “Boris Johnson’s government lost the vote that mattered. This now means that Brexit is now highly unlikely to be delivered by October 31 – as the PM had repeatedly promised.

“The duration of Brexit extension that the EU offers is now in focus. It has been reported that Mr Johnson would accept a 10-day Brexit delay beyond “do or die” day on October 31 if it were a ‘final extension’.

“Interestingly, so far there’s been no mention of a general election from the Prime Minister. He had warned he would pull his Brexit legislation and push for a general election if MPs blocked his plan to pass the bill through the House Commons within just three days.”

He continues: “Tuesday night was an opportunity to move forward with the Brexit saga. The outcome means more delay and more uncertainty.

“Against this backdrop, the Brexit-pummelled pound fell yet again – even though it stabilised after its earlier spike and then sudden decline as much of the news has already been priced-in.

“However, the British economy faces more agonising delay and UK financial assets, with the exception of property, are likely to be squeezed still further.

“Wealth, jobs and opportunity-generating businesses – both in the UK and internationally- are crying out for certainty.

“The fog of Brexit is hampering investment and confidence in Britain. The serious and far-reaching impact of this saga has cost the UK three and a half years of lost opportunity and many tens of billions of pounds.”

He adds: “How this now plays out will depend on the length of extension offered by the EU.

“A short extension to scrutinise more fully the deal, which now has the support of the House of Commons, will be favourable.

“Hopefully, this will then be enough to get Boris Johnson’s Brexit deal over the line which will ultimately be good for the pound – possibly hitting $1.35 – good for the British, EU and global economies, and good for UK financial assets.”

The deVere CEO concludes: “Whatever happens next, this is just the beginning of the Brexit issue – and this was meant to be the ‘easy’ part. The uncertainty is here to stay, especially with the likelihood of a UK general election in the near future.

“As such, investors need to protect themselves from market uncertainty and also best-position themselves for the inevitable opportunities through exposure to a broad range of assets, currencies and geographical regions.”

About:

deVere Group is one of the world’s largest independent advisors of specialist global financial solutions to international, local mass affluent, and high-net-worth clients. It has a network of more than 70 offices across the world, over 80,000 clients and $12bn under advisement

Current situation:

Current situation: