A sense of optimism over global central banks and governments acting with a co-ordinated policy response has revived appetite for riskier assets.

Shares in Asia pushed higher on Tuesday following the overnight rally on Wall Street thanks to stimulus hopes, and this positivity is likely to roll-over into European markets ahead of a conference call today by G7 finance ministers at midday GMT. Investors remain hopeful that G7 countries will join hands to battle the COVID-19 outbreak by enforcing a wave of fiscal measures. However, questions are still being raised as to whether central banks have enough ammunition in their policy toolkits to counter the negative impacts of the outbreak. Let’s not forget the coronavirus is a health crisis that causes major supply-side shocks, so looser monetary policy may have minimal impact in solving the matter at hand.

Dollar humbled by Fed rate cut bets

The mighty Dollar has not been so mighty over the past few days, amid speculation around the Federal Reserve cutting interest rates as soon as its meeting on March 18.

While the Greenback is still considered as a safe-haven destination, investors may be coming to terms with the fact that the US economy is not bullet proof from the virus outbreak and this presents negative risks going forward. Signs of the outbreak impacting economic growth in the States may question the Dollar’s safe-haven status and fuel speculation around the Fed cutting interest rates further, beyond March.

Rocky path ahead for Sterling

After three years of dramatic and chaotic negotiations on the UK’s exit from the European Union, post-Brexit trade talks officially kicked off yesterday.

It looks like both sides have entered the talks adopting a hard-line stance, with Boris Johnson threatening to walk away if negotiations fail to progress by June. Pound sensitivity to Brexit headlines is set to intensify this week and for the rest of the first quarter, as investors evaluate whether a hard Brexit will become reality by the end of 2020.

Focusing on the technical picture, GBPUSD is under pressure on the daily charts. A breakdown below 1.2750 may inspire a decline towards 1.2650. Alternatively, an intraday breakout above 1.2830 could trigger a move towards 1.3000.

Commodity spotlight – Gold

Gold regained some of its lustre on Tuesday, rising roughly 0.5% after experiencing its worst single-day decline since 2013, last Friday.

Although the technical picture suggests that Gold could extend losses, the fundamentals remain in favour of the bulls. Concerns over slowing global growth remain rife amid the coronavirus outbreak, especially after the Organisation for Economic Co-operation and Development (OECD) downgraded its 2020 global growth forecast from 2.9% to 2.4%. The general unease and speculation around loose monetary policy should support appetite for Gold, especially amid the potential for a weaker dollar.

Focusing on the technical picture, Gold is under pressure on the daily charts with prices trading around $1598 as of writing. Sustained weakness below $1600 may encourage a decline back towards $1579 in the near term. Alternatively, a breakout above $1600 could open the doors towards $1620.

Disclaimer: The content in this article comprises personal opinions and should not be construed as containing personal and/or other investment advice and/or an offer of and/or solicitation for any transactions in financial instruments and/or a guarantee and/or prediction of future performance. ForexTime (FXTM), its affiliates, agents, directors, officers or employees do not guarantee the accuracy, validity, timeliness or completeness, of any information or data made available and assume no liability as to any loss arising from any investment based on the same.

US stock market rallied on Monday on investors’ hopes central banks will act to support economies impacted by spread of coronavirus infection from China. The S&P 500 rebounded 4.6% to 3090.23. Dow Jones industrial jumped 5.1% to 26703.32. The Nasdaq rose 4.5% to 8952.16. The dollar weakening continued at faster pace yesterday on disappointing data as the Institute for Supply Management’s manufacturing index fell more than expected: the live dollar index data show the ICE US Dollar index, a measure of the dollar’s strength against a basket of six rival currencies, fell 0.5% to 97.52 and is lower currently. Futures on stock indexes point to lower openings today.

FTSE 100 led European indexes recovery

European stocks ended marginally higher on Monday. The EUR/USD accelerated its climbing while GBP/USD continued sliding yesterday with both pairs higher currently. The Stoxx Europe 600 index added 0.1%. The DAX 30 however dipped 0.3% to 11857.87. France’s CAC 40 added 0.4% and UK’s FTSE 100 rose 1.1% to 6654.89.

Asian indexes recover while Nikkei falls

Asian stock indices are mostly higher today following the rally on Wall Street overnight. Nikkei however lost 1.2% to 21719.78 as yen slide against the dollar reversed. Markets in China are rising before a conference call today by finance ministers and central bank leaders of the Group of Seven major industrial countries to discuss an economic response to the coronovirus outbreak: the Shanghai Composite Index is up 0.7 % and Hong Kong’s Hang Seng Index is 0.3% higher. Australia’s All Ordinaries Index recovered 0.7% despite continuing Australian dollar climb against the greenback even though the Reserve Bank of Australia cut rates to a record low 0.5%.

Brent futures prices are retracing lower today. Prices ended sharply higher yesterday as traders bet OPEC and major producers of crude oil will soon announce additional production cuts. May Brent crude closed 4.5% higher at $51.90 a barrel on Monday.

Gold rises as Dollar weakening continues

Gold prices are extending gains today. April gold rose 1.8% on Monday.

Note: This overview has an informative and tutorial character and is published for free. All the data, included in the overview, are received from public sources, recognized as more or less reliable. Moreover, there is no guarantee that the indicated information is full and precise. Overviews are not updated. The whole information in each overview, including opinion, indicators, charts and anything else, is provided only for familiarization purposes and is not financial advice or а recommendation. The whole text and its any part, as well as the charts cannot be considered as an offer to make a deal with any asset. IFC Markets and its employees under any circumstances are not liable for any action taken by someone else during or after reading the overview.

Proven and Probable’s Maurice Jackson and Sprott USA financial advisor Tekoa Da Silva discuss the common mistakes investors make in securing private placements.

Maurice Jackson: This is one interview in a special four-part series entitled All About Private Placements. Joining us for conversation is Tekoa Da Silva. He is an accomplished licensed financial advisor for Sprott USA, the preeminent name in the natural resource base. Full disclosure, the following is not a Sprott USA-endorsed product, and it is for educational purposes only.

Tekoa, what are the most common mistakes you see when people buy private placements?

Tekoa Da Silva: Boy, what a wonderful question. The first one that comes to mind is buying a private placement when an individual’s legally, technically, not qualified to be able to do so. What comes to mind is a young man that I spoke with once who was looking for someone to assist him with depositing his private placement securities. There is contract that you have to complete in order to buy the private placement. We discussed his net worth and I found that he was not an accredited investor. And I asked him how he was able to buy those securities not being an accredited investor, because the issuers, at least from a North American contextthese natural resource mining share companiesin most instances [have] to verify in the subscription agreement there. The issuing company asks you to check off all the boxes indicating that you’re an accredited investor. And if you don’t check off those boxes, they don’t sell you these securities. They don’t sell you the private placement.

But somehow this young gentlemanhe had these securities. So I thought that somewhere in the process, maybe the issuer made a mistake or maybe he made a mistake, but he somehow bought these things not being accredited. And my understanding was that he couldn’t find any brokerany specialist, a resource broker who could do your private placement depositswho could help him. So he was trapped. His money was stuck inside the security because he was unaccredited.

So that’s the first mistake, I would say. Confirm with the issuer. Do we have to be accredited? And if they say yes and someone’s thinking, “Well, what proof needs to be provided indicating that I’m an accredited investor?”

Do you need bank statements? Do you need any proof? The issuer says, “No,” and the person may think, “Oh well,” maybe fudging the documents or something like that just to be able to buy it. Don’t do it. Don’t do it. Tell the truth, because you don’t want your capital to get stuck inside of security that can’t be liquidated. So always confirm and don’t make that mistake.

The next mistake that I would say is pretty common that a person could make is buying into a private placement, obtaining a. . .physical security, without first having a destination, a home with which to deposit the security. I came across a gentleman who is based in a country, a wonderful country that I’ve traveled in and visited; it’s a great place. But from a banking standpoint, there are some North American clearing firms or broker dealers that don’t want to do business with certain regions or residents in those regions.

And so this gentleman said, “Hey, I’ve got this private placement security, can you deposit it for me?” I said, “Well, I can’t; maybe another broker can.” Not because I don’t want to, but because the clearing firm doesn’t want to because that country is not within their grouping of accepted jurisdictions.

So you want to double check with the broker that you use. After you open the account, say, “Hey, I’m a resident of this country. Is there going to be any problem?” Double check this before you put your money up to buy the security. So that’s the second most common mistake that I’ve seen.

The next common mistake that I’ve seen [happens when] they really like a company, and they want to support it multiple times by private placement over the course of a couple of years. So let’s just say that they keep their shares. They don’t deposit them in a broker dealer account every time they do the private placement, but they just keep them at home in a safe deposit box or something like this. They do multiple product placements, and in each of the product placements, they buy the exact same share count.

So, let’s say you do three private placements in the company. Let’s say an individual bought their private placement there three times, and every time they bought 50,000 shares. That’s wonderful. They’ve got a great position of 150,000 shares and hopefully 150,000 warrants. But what happens is, if a person rushes then to go deposit all three of those private placements at the exact same time with their broker dealer, the administrative staffthey get these three deposits all matching of 50,000 shares. And what they need to do is they need to build a legal case for every single one of them. They have to find the proof of purchase, they have to have copies of the original subscription agreements. And if every single one of these has matching share accounts, the administrative staff cannot easily identify between all three of the private placements without reading out long numbers of saying something like yes, private placement number one, which is the security number XQZTY5000, and that’s having to communicate with each other all day long.

So I would suggest instead of doing three private placements for 50,000 shares each, do three private placements and number them this way: 50,100 shares, 50,200 shares, 50,300 shares, so the administrative staff can quickly identify amongst each. Because they’ll have three to four employees at each of the layerseach of the financial organization layers are going to be touching this thing and communicating with each other. If you number them that way, they can say, “Oh yeah, placement that’s marked number 150,100.” Boom. They can pull up all the old paperwork and help you faster, because the last thing you want is administrative staff in some part of the processing, saying “You know what, this is just. . .I’ve got to push this aside and do some other work right now.”

Maurice Jackson: Well, it also raises eyebrows, does it not? Because it could be there’s a question of, is this an illegal certificate I’m receiving, is this something counterfeit? And you referenced something else I don’t think we’ve covered so far. And that is you do have to have proof of purchase?

Tekoa Da Silva: Your broker dealer can walk you through the legal package that you need to assemble every time you deposit private placement, obtaining security. And just for reference, that’s going to be your subscription agreement. It’s going to be your proof of purchase and it’s going to be the access security itself along with anything else that they have, that they ask for.

Maurice Jackson: We’ve covered companies predominantly on the Toronto Stock Exchange that are public companies. Are we able to participate in private placements through companies that are pre-IPO?

Tekoa Da Silva: I would say that this is an extension of that question of what are some of the worst mistakes the person can make when participating in a private placement. . .still assuming natural resource exploration, development-stage companies, [and that is] participating in a private or pre-IPO entity and being a nonprofessional, or participating in a company in which you don’t have a high level of assurance from the issuer or from the broker that this company is actually going to go public someday. If a person is a busy professional, and they’re not working with real pros in terms of the issuer that they’re working with, like skilled entrepreneurs, where they’re good for their word. And then also, a broker dealer [is] the same way, where they know how to handle private and pre-IPO private placements.

If they don’t have those two things involved and someone solicits them with an opportunity like that, I would say be very careful. Because if they don’t go public, you may never get your capital out back from that security; it’s stranded on an island. And then also, it could take longer than expected.

One example comes to mind of a company that I observed in 2014 that said, “We’re going to be going IPO public sometime soon, when we get a little bit of recovery in the market.” That same companynow it’s five years later and they’re still private. And the person that participated in that private placement, along with others that I’ve seen, is still waiting. And then, in the meantime, anything could be going on with that company. Personnel could be coming and going, their financial situation could be deteriorating. And then the person who owns the stock certificate bought by the private placement could have changes going on in their own personal life.

The next common mistake that I see people makethis one is so hugeand that is, losing your supporting documents that you obtained when you did your private placement at the beginning. Your supporting documents [are] your [copies] of the executed subscription agreementthat 30- to 40-page document that you filled out. It’s going to have your signatures and information on here, and [it’s] going to have the company’s, the issuing company’s signature on there, too. You can’t lose that document. Because these days, if you lose that document, you may have a broker say, “Well, according to anti-money laundering laws, we can’t deposit this from you, because we don’t know that this came from a legitimate source.

And in the same thing, if a proof of purchaseif you can’t prove that you got a bank statement or a wire receipt, some other transference of money documented by a real bankthe broker dealer could say, “Well, we can’t document or we can’t prove to our compliance department that you didn’t pay for this private placement with a suitcase full of cash obtained from some strange circumstances.”

So. . .never lose your supporting documents. . .Keep a scanned copy in your records, keep a physical copy if you need to. And then if there’s a third party, such as your broker, you could e-mail them copies of all the information, and they’ll have archived email records. At least they should, which will keep a permanent copy in your records to see you don’t lose them.

Another common mistake here too is losing your security certificate or your stock certificate, your debenture, your warrant certificate. You want to try not to lose those things. It’s not the end of the world if you do, but guess what? Getting a new copy, it’s a hassle. It could take anywhere [up] to 10 weeks dealing with the issuer and with the transfer agent, getting that security reproduced. And it could cost you money. . .though the $600 is a good budget for third-party administrative fees.

But in the meantime, through that 4 to 10 week process, anything could be going on with the stock. It could be exploding, it could be collapsing, there could be all types of things going on, and you just don’t want to do that to yourself. So make sure to keep the certificate in a safe place. If you’re going to keep it in your possession, I would suggest having a pretty good system in place for possession of those, or immediately get them to your broker dealer. Because they’ll have a bolting system, or at least they should, with their clearing firm keep them really safe and secure.

The next common mistake that I see people make in private placements is buying in a registration name that is different from a brokerage account name that they may use after broker. Okay: What does the registration name? Registration name or registrant, that’s simply the name that gets printed on your security. So if you’ve got a security, Maurice, in let’s say Novo Resources Corp. (NVO:TSX.V; NSRPF:OTCQX), a private placement says Maurice Jackson, the registration name is Maurice Jackson. But if a different name is printed on that security. . .

Maurice Jackson: Let’s use Proven and Probable. . .

Tekoa Da Silva: Proven and Probable. . .that’s a different registrant. It’s legally a different party. So if we were to talk to a broker about it, with a brokerage account that matched your personal name or my personal name or the name of a business, they may say, “Whoa, we understand that you own both, but they’re not compatible with each other.”

So, in order for a person to deposit the private placement security that’s in your name or the business into the vice versa brokerage account they have, they may say, “Well, we could do it for you, but first you’re going to have to send that placement security back to the transfer agent and you get it reissued, get everything printed, and get the opposing name printed on the certificate.” And then someone says, “Okay, sure, it sounds nice and easy. How long is that going to take?” Four to six weeks. So two weeks sending it both directions. It’s four to six weeks, reprinting it and then another, potentiallywho knows how longtwo to four, six weeks of a deposit process that the brokerage account, the broker firm, may have redepositing that security again.

So be careful. Check with your broker first. What’s the exact legal name of my brokerage account? Does my private placement, my registration name for the private placement, need to match exactly and precisely? I just want to have this confirmed before I do it. That way you can avoid costly time errors that come in down the road.

Maurice Jackson: And another option would bewhich is not one that people really want, because you don’t want open up a second accountbut the other option may be then just open up a personal name account with that broker and a business name. And then you can toggle between the two, whichever is appropriate for the name on the actual share certificate.

Tekoa Da Silva: Yes, sir. That’s another route that a person could take. But I’ll tell you, in some crazy market conditions, and resource markets, they can oftentimes can be exploded, or they can be completely dead. But when you’re moving in a period of explosive market conditions, if you’re working with a small, specialist, resource firm, all their staff [is] inundated with paperwork, with phone calls, with just things going haywire. And you don’t want to be caught in a situation like that unprepared, with having a wrong account. So way in advance, doing what you just said, having an extra account already created if neededI think it’s a very good idea.

Maurice Jackson: So timing and being prepared are the two components here that are intangible, [and] really you’re sharing words of wisdom, the experience you’ve been there. You’ve seen it; you’ve heard the profanity on the other end of the line, I’m sure. Do you have another example for us?

Tekoa Da Silva: Oftentimes the junior resource space companies are going through mergers and acquisitions, or need changes, or the share structure changes, where there may be a 10-for-1 rollback or a 100-for-1 rollback. And if you’ve got that share certificate in your possessionthe name of the company and the number of shares or security, a quantity on a certificateit can’t immediately be produced for you unless the company takes it on their own to send you a new certificate immediately in the mail.

So what happens is, the change happens but your certificate stays the same and your broker may say, “Oh well, you could send it in when it’s convenient for you, and we’ll just make that adjustment when it gets here.” But what happens if six months down the line, the company makes another change, another share structure adjustment, or another M&A, and then another and then another.

Maurice Jackson: These do happen. This is a realistic scenario that you’re providing here.

Tekoa Da Silva: Yeah. You know, we saw this happen with a very successful company and successful management team. I think it was Equinox Gold in its early years; I believe it was Trek Mining, and then JDL Gold. So they had multiple changes down the road. And I, just off the top of my head, can’t recall if they had share structure changes along the way, too.

What I’m saying is when you see that name change or the share structure change, get that security deposited and update it as fast as you possibly can. Because if it’s two, three and four changes down the road, the administrative staff, the legal review department, what they’re going to do is they’re going to say, “You know what, in order for us to verify all this, it may take a month or longer.” So they may just say, “Hey, we’ll get it done when we get it done.” And it could just be a much more time-consuming process than it otherwise could be the case if you immediately moved when you saw that change happen.

Maurice Jackson: And if I can interject here, but then you miss out on what could potentially be an arbitrage opportunity. And they’re not long, but you have to be prepared, and that’s something we’re emphasizing here. It’s timing and being prepared and having a plan.

Tekoa Da Silva: Another common mistake that I see made during private placements is if a person is of the opinion that at some time in the future they may be passing on their securities to their heirs, that that time has come, and they own physical certificates of companies. I think that could be a smart idea, in consultation with their managers, to consider getting those securities deposited and put in a digital format in the individual’s name or in the name of a trust or whatever entity is in question. Because if a person passes away and the securities are still in that person’s name that passed away, you have a period of time where that can be so fairly quickly handled and I think one wants to move quickly in that circumstance.

Because what happens if one doesnt move quickly? Well, you may have an M&A, you may have a restructuring change, you may have another change with any structure of errors, or another manager coming in to manage the estate, or simply time passes. I saw circumstance where a person had securities decades old and the various people that I talked to in that circumstance, simply had no idea how to assist that individual. And various industry people that I spoke to with circumstances like that say, “Well, you may have had people out there who own securities from the ’30s, the ’40s, the ’50s. And what happens is, you have to research the ownership chain, all the entities that came and went throughout that process, in order to recover that money.

And if you don’t have a person or a group that’s willing to go through the legal history review, the capital could be permanently lost. . .I see is if you have a change in the living parties, or the heirs share certificates. If you see that’s coming, immediately get them deposited, put into a digital format, maybe convert them into cash or something like that so you can conveniently pass along those assets to the heirs so that you can avoid them being permanently lost.

Maurice Jackson: These are wonderful gems that you’re sharing with us. I should say, golden nuggets of wisdom, because it really makes a difference for someone if they’re not aware in thinking the entire process out.

And you have to respect the process because it is a process. The market doesn’t move when we want it to move. And when I say the market, it’s not just the prices of shares, but it’s also behind the scenes. What we’re discussing here in this format is the process to take it from that certificate format to direct registration to street name. It is a process and if you don’t respect the process, you will get stressed out. You will be upset, and if you understand what’s coming before you, you can be better prepared. And that’s exactly what we’re trying to do here.

And again, this is not legal advice. This is not financial advice. This is simply an education format that we want to provide to you regarding the value proposition of private placements. Did you have another one for us, sir?

Tekoa Da Silva: No worries. Those I would say pretty much cover the most common mistakes that I’ve seen in regards to private placements.

Maurice Jackson: Well, Tekoa, we’ve covered a lot of material here. What are your closing thoughts or words of wisdom that you’d like to share with anyone regarding private placements?

Tekoa Da Silva: Well, I’d think about it very carefully before doing it. I think understanding that the process of participation is probably a one- to three-year commitment. Going about thinking of trying it out for one to three months to see if it fits may not be too helpful. Within the one- to three-year period, one really needs to find the right people to work with. Find the best sources of information for the pipeline of opportunities, the best people to work with in terms of depositing the securities and handling the cashpeople who are competent at that and who can also help you vet those deals that you may find on their own.

Those individuals, from an administrative standpoint, can really help you, step-by-step guide you through the process, to help protect you from losing your money. I think that’s what I would say. Definitely [don’t] not be shy about mapping out the entire process and talking to all those parties, talking to multiple sources within those different groups, so that you can have the whole thing [thought] out, even if you decide not to do it. I think that’s probably the best advice that I would suggest.

Maurice Jackson: Ladies and gentlemen, this concludes our series All About Private Placements. If you wish to have a conversation with Mr. Da Silva, e-mail [email protected]. If you want to find out which private placements have our attention at Proven and Probable, simply visit www.provenandprobable.com. Place your correspondence in the subscribe box and let us know that you are accredited. Subscription is free and we do not share your correspondence with third parties.

Maurice Jackson is the founder of Proven and Probable, a site that aims to enrich its subscribers through education in precious metals and junior mining companies that will enrich the world.

Disclosure: 1) Maurice Jackson: I, or members of my immediate household or family, own shares of the following companies mentioned in this article: Novo Resources. I personally am, or members of my immediate household or family are, paid by the following companies mentioned in this article: None. My company has a financial relationship with the following companies mentioned in this article: Novo Resources. Proven and Probable disclosures are listed below. 2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. 3) Statements and opinions expressed are the opinions of the author and not of Streetwise Reports or its officers. The author is wholly responsible for the validity of the statements. The author was not paid by Streetwise Reports for this article. Streetwise Reports was not paid by the author to publish or syndicate this article. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy. 4) This article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases.

Proven and Probable LLC receives financial compensation from its sponsors. The compensation is used is to fund both sponsor-specific activities and general report activities, website, and general and administrative costs. Sponsor-specific activities may include aggregating content and publishing that content on the Proven and Probable website, creating and maintaining company landing pages, interviewing key management, posting a banner/billboard, and/or issuing press releases. The fees also cover the costs for Proven and Probable to publish sector-specific information on our site, and also to create content by interviewing experts in the sector. Monthly sponsorship fees range from $1,000 to $4,000 per month. Proven and Probable LLC does accept stock for payment of sponsorship fees. Sponsor pages may be considered advertising for the purposes of 18 U.S.C. 1734.

The Information presented in Proven and Probable is provided for educational and informational purposes only, without any express or implied warranty of any kind, including warranties of accuracy, completeness, or fitness for any particular purpose. The Information contained in or provided from or through this forum is not intended to be and does not constitute financial advice, investment advice, trading advice or any other advice. The Information on this forum and provided from or through this forum is general in nature and is not specific to you the User or anyone else. You should not make any decision, financial, investments, trading or otherwise, based on any of the information presented on this forum without undertaking independent due diligence and consultation with a professional broker or competent financial adviser. You understand that you are using any and all Information available on or through this forum at your own risk.

Sangamo Therapeutics shares traded higher after the company reported Q4/19 and FY/19 earnings and advised that it signed a global collaboration agreement with Biogen to develop gene regulation therapies for Alzheimer’s, Parkinson’s, neuromuscular and neurological diseases.

This morning prior to the U.S. markets open, genomic medicine company Sangamo Therapeutics Inc. (SGMO:NASDAQ),reported fourth quarter and full-year 2019 financial results and recent business highlights.

The report comes one day after the firm announced that it entered into a global collaboration agreement with Biogen Inc. (BIIB:NASDAQ) to develop and commercialize gene regulation therapies for Alzheimer’s, Parkinson’s, neuromuscular and other neurological diseases. Under the terms of the agreement, “Biogen has exclusive global rights to ST-501 for tauopathies including Alzheimer’s disease, ST-502 for synucleinopathies including Parkinson’s disease, and a third undisclosed neuromuscular disease target.”

The company’s CEO Sandy Macrae commented, “This quarter marked an important milestone for Sangamo, as we transitioned to a Phase 3 company following the transfer of the IND for SB-525 hemophilia A gene therapy to our partner Pfizer Inc. (PFE:NYSE), who plan to commence the registrational study this year. This is a significant step in our mission to bring our genomic medicines to patients…This year we also look forward to progressing our wholly owned assets, ST-920 gene therapy for Fabry disease and TX200 CAR-Treg cell therapy, in the clinic, and will work closely with our collaborator, Kite, a Gilead Sciences Inc. (GILD:NASDAQ) company, as they advance KITE-037, an anti-CD19 allogeneic CAR-T therapy into a Phase 1/2 clinical trial.”

The company reported Revenues for Q4/19 of $54.9 million, compared to $26.8 million for Q4/18, and consolidated net income of $4.6 million, or $0.04 per share, compared to -$18.7 million, or -$0.18 per share in the same corresponding period.

For FY/19 the firm stated that Revenues were $102.4 million, compared to $84.5 million in FY/18, and a consolidated net loss of -$95.2 million, or -$0.85 per share, compared to a consolidated net loss -$68.3 million, or -$0.70 per share in FY/18.

The company advised that it expects FY/20 GAAP total operating expenses will be in the range of $270-$285 million and FY/20 Non-GAAP total operating expenses are estimated to be in the range of $245-$260 million.

Sangamo Therapeutics is based in Brisbane, Calif. and states that “it is committed to translating ground-breaking science into genomic medicines with the potential to transform patients’ lives using gene therapy, ex vivo gene-edited cell therapy, and in vivo genome editing and genome regulation.”

Sangamo Therapeutics began the day with a market capitalization of around $772.7 million billion with approximately 115.9 million shares outstanding and a short interest of about 15.3%. SGMO shares opened more than 30% higher today at $8.93 (+$2.265, +33.40%) over yesterday’s $6.665 closing price. The stock has traded today between $8.02 to $9.19 per share and is currently trading at $8.675 (+$2.01, +30.16%).

Disclosure: 1) Stephen Hytha compiled this article for Streetwise Reports LLC and provides services to Streetwise Reports as an independent contractor. He or members of his household own securities of the following companies mentioned in the article: None. He or members of his household are paid by the following companies mentioned in this article: None. 2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. 3) Comments and opinions expressed are those of the specific experts and not of Streetwise Reports or its officers. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. 4) The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases. 6) This article does not constitute medical advice. Officers, employees and contributors to Streetwise Reports are not licensed medical professionals. Readers should always contact their healthcare professionals for medical advice.

Matador Resources’ Q4/19 performance and its 2020 guidance are reviewed in a Raymond James report.

In a Feb. 25 research note, Raymond James analyst John Freeman reported that Matador Resources Co. (MTDR:NYSE) ended 2019 with a beat on both volumes and EBITDA in Q4.

Freeman relayed that the Dallas-based company’s quarterly volumes exceeded the Street’s expectation by 7%, driven by shorter-than-expected shut-in times, improved well performance and accelerated turned in lines (TILs). Whereas the early TILs increased capex, 2% above consensus’ forecast, the outperformance in volumes more than made up for it. EBITDA in Q4/19 surpassed the Street’s forecast as well, by 12%.

Freeman reviewed expectations for Matador in 2020. The energy company intends to maintain, through the year, the six rigs it has working now in the Delaware Basin. It intends to complete 69 gross, or 58 net, operated wells and participate in a significant number of non-operated wells.

Matador’s guidance for 2020 production is 75,500 barrels of oil equivalent per day, higher than that of 2019 and 3% higher than the Street’s projection. Exit rate guidance is “massive,” 87,000 barrels of oil equivalent per day, 9% above consensus’ forecast, the analyst noted. These achievements should more than offset expected capex during the year of $815 million, which is 2% higher than consensus’ projection. “The extremely strong Q4/20 run rate (oil volumes up 22% over Q4/19) should set Matador up with strong momentum into 2021,” commented Freeman.

As for the spending gap, Freeman indicated that Matador intends to work toward narrowing it by achieving further efficiencies, divesting of additional non-core assets and monetizing mineral interests.

Raymond James has an Outperform rating but no target price on Matador Resources. Its stock is trading at around $9.64 per share.

Disclosure: 1) Doresa Banning compiled this article for Streetwise Reports LLC and provides services to Streetwise Reports as an independent contractor. She or members of her household own securities of the following companies mentioned in the article: None. She or members of her household are paid by the following companies mentioned in this article: None. 2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. 3) Comments and opinions expressed are those of the specific experts and not of Streetwise Reports or its officers. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. 4) The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases.

Disclosures from Raymond James, Matador Resources Company, February 25, 2020

ANALYST INFORMATION

Analysts Holdings and Compensation: Equity analysts and their staffs at Raymond James are compensated based on a salary and bonus system. Several factors enter into the bonus determination, including quality and performance of research product, the analyst’s success in rating stocks versus an industry index, and support effectiveness to trading and the retail and institutional sales forces. Other factors may include but are not limited to: overall ratings from internal (other than investment banking) or external parties and the general productivity and revenue generated in covered stocks.

The analyst John Freeman, primarily responsible for the preparation of this research report, attests to the following: (1) that the views and opinions rendered in this research report reflect his or her personal views about the subject companies or issuers and (2) that no part of the research analyst’s compensation was, is, or will be directly or indirectly related to the specific recommendations or views in this research report. In addition, said analyst(s) has not received compensation from any subject company in the last 12 months.

RAYMOND JAMES RELATIONSHIP DISCLOSURES Certain affiliates of the RJ Group expect to receive or intend to seek compensation for investment banking services from all companies under research coverage within the next three months.

Raymond James & Associates, Inc. makes a market in the shares of Matador Resources Company.

Additional Risk and Disclosure information, as well as more information on the Raymond James rating system and suitability categories, is available here.

Reliq Health Technologies advised that it has been selected as remote patient monitoring and chronic care management solutions partner by U.S. health data company MaxMD.

In a news release, mobile health and telemedicine solutions technology company Reliq Health Technologies Inc. (RHT:TSX.V; RQHTF:OTCQB) announced that “it has partnered with MaxMD of Fort Lee, N.J, a leading U.S. provider of secure healthcare information technology and interoperability solutions.”

“We are thrilled to partner with MaxMD to leverage the rich data their technology platforms can provide for clinicians, healthcare systems and payors…MaxMD has customers in all 50 States and Puerto Rico, and we are excited to introduce their client base to our Remote Patient Monitoring (RPM) and Chronic Care Management (CCM) solutions,” commented Reliq Health Technologies’ CEO Dr. Lisa Crossley.

Scott Finlay, CEO of MaxMD added, “MaxMD provides standards-based solutions that feed legacy systems the data they need, and supply the most advanced information-sharing capabilities in the industry…Working with Reliq Health will allow us to offer our clients new options to expand access to care, improve health outcomes and reduce healthcare costs by using the iUGO Care RPM and CCM platforms.”

The report stated that “MaxMD is the leader in secure healthcare information technology and interoperability solutions, and that its deep technical expertise and industry leadership in the application of Healthcare Information Technology (HIT) standards such as Fast Healthcare Interoperability Resources (FHIR), HL7 Version 2 (V2), Clinical Document Architecture (CDA), public key infrastructure (PKI), USCDI, and the Direct Protocol. MaxMD products enable clients to leverage current and emerging standards through a completely unique approach to data exchange designed to create ‘scalable data liquidity.'”

The report further indicated that “Reliq Health Technologies is a healthcare technology company that specializes in developing innovative software solutions for the Community Care market,” and that “the firm’s iUGO Care platform allows complex patients to receive high quality care at home, improving health outcomes, enhancing quality of life for patients and families and reducing the cost of care delivery.”

Disclosure: 1) Stephen Hytha compiled this article for Streetwise Reports LLC and provides services to Streetwise Reports as an independent contractor. He or members of his household own securities of the following companies mentioned in the article: None. He or members of his household are paid by the following companies mentioned in this article: None. 2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. 3) Comments and opinions expressed are those of the specific experts and not of Streetwise Reports or its officers. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. 4) The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases. As of the date of this article, officers and/or employees of Streetwise Reports LLC (including members of their household) own securities of Reliq Health Technologies, a company mentioned in this article. 6) This article does not constitute medical advice. Officers, employees and contributors to Streetwise Reports are not licensed medical professionals. Readers should always contact their healthcare professionals for medical advice.

Shares of Nemaura Medical traded 20% higher after the firm reported that it is investigating using its non-invasive continuous glucose monitor sugarBEAT® jointly with its planned health subscription service BEAT®diabetes, to provide personalized lifestyle coaching for people with Type 2 diabetes and prediabetes.

Medical technology company Nemaura Medical Inc. (NMRD:NASDAQ), a developer and manufacturer of wearable micro-systems-based diagnostic devices including its flexible continuous glucose monitor (“CGM”) sugarBEAT®, together with BEAT®diabetes, a planned health subscription service designed to help people with Type 2 diabetes and prediabetes through personalized lifestyle coaching, yesterday, announced that “it is planning to initiate a user study comparing sugarBEAT® directly against a highly successful major incumbent CGM sensor.” The company noted that its goal is to position sugarBEAT as a non-invasive, cost-effective alternative and complementary device to other expensive and invasive CGMs.

The company’s CEO Dr. Faz Chowdhury commented, “Our decision to go head-to-head vs. a hugely successful CGM sensor was based on positive feedback we received from recent meetings with public health insurers in key territories in Europe…We believe that most people with diabetes do not currently use any continuous glucose monitoring system due to the high costs and the invasiveness of current products. We believe that sugarBEAT® changes this paradigm and is the first non-invasive CGM to provide the masses an option for daily monitoring whenever they choose at an affordable price point…We believe that sugarBEAT®’s flexibility empowers users with very powerful trend data at a lower cost compared to current CGM’s, which we believe will encourage broad adoption of the system”.

The company advised that “several studies are planned over the course of this year designed to demonstrate the effectiveness of sugarBEAT® to increase Time-In-Range, thus reducing HbA1C with intermittent (non-consecutive days) use over a few days per week or even month.”

The sugarBEAT device is worn during waking hours and consists of a daily disposable adhesive skin-patch that is connected to a rechargeable transmitter and works with an app that displays glucose readings at five-minute intervals.

The firm stated that it initiated phase one of the commercial launch of sugarBEAT in the U.K. after it received CE Mark approval in 2019. This approval designation is the manufacturer’s declaration that the product meets EU standards for health, safety and environmental protection. During the initial phase, devices were supplied to only a small group of users while the company focused its efforts on ramping up production. The company advised that DB Ethitronix, the U.K. licensee of sugarBEAT, is currently finalizing the launch of online sales of sugarBEAT.

Nemaura is a medical technology firm developing non-invasive and minimally invasive wearable diagnostic devices, coupled with artificial intelligence capabilities for digital healthcare. The firm is also presently engaged in “commercializing BEAT®diabetes, a health subscription service designed to help people with diabetes and prediabetes better manage diabetes and reverse Type 2 diabetes or prevent diabetes through 1-on-1 lifestyle coaching and behavior driven by real time continuous glucose monitoring (CGM) and daily glucose trend data provided by sugarBEAT®, a non-invasive and flexible CGM.”

Nemaura started the day with a market capitalization of around $120.7 million with approximately 20.81 million shares outstanding. NMRD shares opened nearly 38% higher today at $8.00 (+$2.20, +37.93%) over yesterday’s $5.80 closing price. The stock has traded today between $6.66 and $10.40 per share and at present is trading at $7.40 (+$1.60, +27.59%).

Disclosure: 1) Stephen Hytha compiled this article for Streetwise Reports LLC and provides services to Streetwise Reports as an independent contractor. He or members of his household own securities of the following companies mentioned in the article: None. He or members of his household are paid by the following companies mentioned in this article: None. 2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. 3) Comments and opinions expressed are those of the specific experts and not of Streetwise Reports or its officers. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. 4) The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases. 6) This article does not constitute medical advice. Officers, employees and contributors to Streetwise Reports are not licensed medical professionals. Readers should always contact their healthcare professionals for medical advice.

Bob Moriarty of 321gold discusses a company he sees as a safe haven amid economic chaos.

Last week provided a glimpse into the future of the stock market. Only a glimpse. It is going to get a whole lot worse.

On January 1, I said in an article I titled Beware the Stock Market, “As the Everything Bubble pops, the financial system will destroy most investors because they are unprepared.” Lest my readers misconstrue what I meant, I followed that up with another article on January 27 where I repeated, “Now would be a great time to be prepared for a disaster bigger than any in history.”

The two biggest measures of metals stocks would be the XAU and HUI. Both peaked on the 24th of February and began to tumble. I wrote another piece a couple of days later and said, “The Greatest Depression is going to have negative effects on everyone. No one will escape entirely no matter how well prepared you are.”

When the metals shares fell out of bed I got fifty emails essentially asking why I hadn’t warned my readers.

Sigh!!

One of the smartest people I follow thinks the stock market is going to drop by 50%. I like David Collum a lot but this time he’s dead wrong. Another very bright financial investor named John Hussman believes not only that the Fed is powerless, he says the stock market is going to collapse by 67%. Both predictions are interesting but basically absurd.

Those guys are way too optimistic.

The Dow topped on September 3rd, 1929, at 381.17 before starting to tumble. The decline continued until July 8, 1932, when the Dow measured at 41.22. That’s in excess of an 89% decline. On January 21st, 1980 silver touched $50.25 an ounce on the Comex. By early February of 1993 the price of the metal touched $3.53, a fall of 93% in thirteen years.

Do I believe the stock market will drop by 50% or 67%?

Yes.

On the way down to the bottom that will be far lower.

Readers should remember back to 2008 when gold was up $100 one day after being down $150 the day before. These are the most dangerous markets I have ever seen and most investors are going to screw it up by listening to the people who tell them what they want to hear.

I’ve written two books and hundreds of articles about what I see in progress. And I’ll say I get it right a lot more often than I get it wrong. If you haven’t spent the $12 or so each costs, you are being penny-wise and pound-foolish. Would you spend a few cents to make dollars?

They are great books filled with important advice. We are in totally uncharted waters. The Fed is clueless. Their chance of fixing the problem is zero; they caused the greatest bubble in world history. The Chinese just nuked the Everything Bubble and if you believe it’s because of the coronavirus, you are missing what is right in front of you.

In the best case, a bad flu season might last 4-6 months into the summer when they usually die off naturally. If we are exceptionally lucky, this virus will do the same. That’s a giant IF. While it continues, the Just in Time manufacturing just stopped for the 4-6 months minimum to get over the virus. Everything in China just stopped. We in the West are but a month behind China. Auto manufacturing is stopping. The cruise industry just died. Airline crews are refusing to fly. Shortages of medicines using 90% of their ingredients from China are happening already. The world’s economy is dying.

China is going to lose more people to starvation than to the virus and the world’s economy just came to a screeching halt. I don’t know how many other people than me see that so far. They will in another month or so.

There are some safe havens. Or relatively safe havens.

While so far the baby has been tossed out with the bathwater as margin clerks sharpened their quills, mining and resource stocks will lead the way out at the end of the carnage. The safest now and most resilient will be the producers.

But Calibre just announced another giant step forward. It’s no secret that the majors have been consuming their young and each year have less in reserve. And it’s not secret that they have stopped exploration almost entirely.

Well, Rio Tinto sees the potential in Nicaragua as well as in Calibre. On the 24th of February the two announced a partnership in the country to the benefit of both. Rio entered into a deal with Calibre where Rio will invest as much as $45 million to partner with Calibre in their Borosi gold project in the Northeast of Nicaragua. The venture will also include a strategic exploration alliance where the two companies will work together to identify and acquire concessions in the country.

I see this as the near term future for mining. Newmont is doing something similar with Irving in Japan. Barrick is partnering with Japan Gold as well.

The investing horizon is the most dangerous I have seen in my lifetime. Banks are at risk; the entire financial structure may well come tumbling down. Resources are a form of safe haven but investors must learn to buy cheap and sell dear. The prices of rhodium and palladium went supernova in the past month as gold open interest blew past all the records yet most investors refused to take profits while they could. I can write all the good advice in the world, if investors have no sense, they will have no cents.

Gold production stories offer safe haven and Calibre has both excellent management and projects. I bought shares in the private placement (the one with zero warrants) and they are an advertiser. Please take responsibility for your own investment decisions, it’s your money, after all.

Bob Moriarty founded 321gold.com, with his late wife, Barbara Moriarty, more than 16 years ago. They later added 321energy.com to cover oil, natural gas, gasoline, coal, solar, wind and nuclear energy. Both sites feature articles, editorial opinions, pricing figures and updates on current events affecting both sectors. Previously, Moriarty was a Marine F-4B and O-1 pilot with more than 832 missions in Vietnam. He holds 14 international aviation records.

Disclosure: 1) Bob Moriarty: I, or members of my immediate household or family, own shares of the following companies mentioned in this article: Calibre Mining and Irving Resources. My company has a financial relationship with the following companies mentioned in this article: Calibre Mining and Irving Resources are advertisers on 321 Gold. I determined which companies would be included in this article based on my research and understanding of the sector. 2) The following companies mentioned are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. 3) Statements and opinions expressed are the opinions of the author and not of Streetwise Reports or its officers. The author is wholly responsible for the validity of the statements. The author was not paid by Streetwise Reports for this article. Streetwise Reports was not paid by the author to publish or syndicate this article. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy. 4) The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases. As of the date of this article, officers and/or employees of Streetwise Reports LLC (including members of their household) own securities of Irving Resources and Newmont Goldcorp, companies mentioned in this article.

Building demonstration plant at Lanxess Project site

After Standard Lithium Ltd. (SLL:TSX.V; STLHF:OTCQX) managed to arrange a CA$5 million (CA$5M; US$3.75M) convertible loan and guarantee agreement with Lanxess AG (LXS:DE) on Oct. 30, 2019, management hasn’t been sitting on its hands. On Feb. 26, 2020, the company announced that an ongoing capital raise, intended to raise CA$6M, was closed at no less then CA$12.1M.

I found this to be very impressive, as sentiment for lithium developers has recovered slightly on the back of Tesla’s unexpected positive results and the following run-up of the share price of the car and battery manufacturer, but is still neutral to negative. The proceedings will be used for the ongoing development of the mentioned demonstration plant, which is capital intensive.

All presented tables are my own material, unless stated otherwise.All pictures are company material, unless stated otherwise.All currencies are in U.S. dollars, unless stated otherwise.

The original announcement on Jan. 30, 2020, mentioned a non-brokered private placement of up to 8 million special warrants, at a price of CA$0.75 per special warrant, for gross proceeds of up to CA$6M. On a side note: The financing being non-brokered is already impressive in itself, as Standard Lithium didn’t have to tap the brokers who usually dominate these financings. Each special warrant or unit consisted of one common share and a half warrant. Each warrant entitled the holder to acquire an additional common share at a price of CA$1.00 per share for a period of twenty-four months, subject to an accelerated expiry if the closing price of the company’s shares is greater than CA$1.50 per share for a period of 15 consecutive trading days. Commodity Capital AG, a strategic investor in the company for a long time, together with management and board of directors signed up for a large portion of this round.

Site visit at project site

As the share price at the time was CA$0.86, and there was an average discount, but nowhere near the maximum allowed discount of 20%. Investors sold off, probably in order to raise cash so they could participate and get that half warrant, but the stock recovered quickly:

However, on Feb. 4, 2020, management announced an increase of the financing to CA$9M, consisting of 12 million special warrants, due to strong demand. This wasn’t it, as despite the coronavirus outbreak the company released news on Feb. 21, 2020, stating that the financing was closed at a very impressive CA$12.1M, for 16.14 million special warrants.

From the reported highlights, I especially liked the personal investments of the CEO Robert Mintak and the COO Andy Robinson, who, together with director Anthony Alvaro, invested another meaningful CA$800,000 besides their already sizable positions:

Two strategic investors subscribed for 4,100,000 special warrants or $3,075,000;

Meaningful participation from the company’s board of directors and senior management and technical team members;

Chief Executive Officer Robert Mintak, President and Chief Operating Officer Dr. Andy Robinson, and director Anthony Alvaro subscribed for a total of 1,066,667 special warrants or $800,000.

In connection with completion of the private placement, the company has paid limited finders’ fees of CA$119,268, and issued 452,025 warrants, to certain arms-length parties who assisted in introducing subscribers to the company. As usual, finders’ fees are based on 67% of the amount raised; this was obviously meant only for a small part of the total raise of CA$12.1M. Most of it was brought in by the strategic investors, which together with management and the board of directors represented a big vote of confidence.

The cash will be used to complete the commissioning of the LiSTR direct lithium extraction demonstration plant in southern Arkansas, as well as to maintain existing property interests and for general working capital purposes.

Following the news releases about this impressive financing news, I had some questions, and contacted CEO Robert Mintak to have a small interview.

The Critical Investor (TCI): Can you say a bit more about the investors that took part in this round?

Robert Mintak (RM): These included new and existing European funds, and a number of local Arkansas investors who have been active and following our development over the past 18 months.

TCI: Was Lanxess taking part in this financing, if you can disclose?

RM: No, they didn’t.

TCI: Is this all the cash you need for commissioning, prefeasibility study (PFS) and optimization?

RM: This will be subject to operational success of the demo plant. We are confident that this will fund us through the proof-of-concept requirements for joint venture (JV) to be formally executed.

TCI: How long will this cash last, and do you foresee more rounds, and if so for what?

RM: This funding round should allow us to push through several significant milestones, including a final investment decision in late Q2, that we believe will be inflection points for a revaluation of our share price over the coming two quarters.

TCI: What about the SiFT plant? This was scheduled to be constructed in Q4 2019.

RM: Construction is underway on the SiFT pilot plant. We anticipate delivery to the Arkansas site in early to mid-Q2.

TCI: When is the PFS expected? Try to be as specific as possible.

RM: A significant amount of data for the PFS is in hand. We are targeting mid to late Q2 for the PFS to be finalized.

TCI: Anything else you want to add?

RM: There has been a lot of recent news surrounding Silicon Valley investment in a startup direct lithium extraction technology, which is exciting news for the entire space. The attention it is bringing to the industry reflects the transformation that direct extraction offers to an industry that is strangely not known for embracing innovation.

I would like to highlight that Standard Lithium is several years ahead of anyone in the direct extraction space at this time. The successful operation of our “LiSTR” industrial-scale direct extraction demonstration plant is one the final steps to cross before a final investment decision on the commercial build is made at our Arkansas projecta project that is already flowing billions of gallons of brine annually. This is a project that, if successful, will be a global showcase for direct extraction and disciplined project execution.

Together with the CA$5M convertible loan raised four months ago, Standard has raised over CA$17M for this period, and this is, apart from amazing, also likely enough to take the project through PFS and a Lanxess final investment decisionof course, depending on the success of the LiSTR demonstration plant.

As a reminder: this demonstration plant is roughly designed at 1/60 scale of the target production capacity of the first phase of commercial production, and should provide sufficient testing data this quarter for a planned, upcoming prefeasibility study in Q2 2020, as mentioned. If the testing is successful, it should be straightforward to scale to commercial production after the investment decision would have been made by Lanxess.

It is important to note that with direct extraction, the commercial construction can be phased, unlike the “all in,” massive earth-moving exercise of evaporation ponds. The demonstration plant is based on Standard Lithium’s proprietary LiSTR technology, which uses a solid sorbent material to selectively extract lithium from Lanxess’ tail brine. The environmentally friendly process eliminates the use of evaporation ponds, reduces processing time from months to hours and greatly increases the effective recovery of lithium.

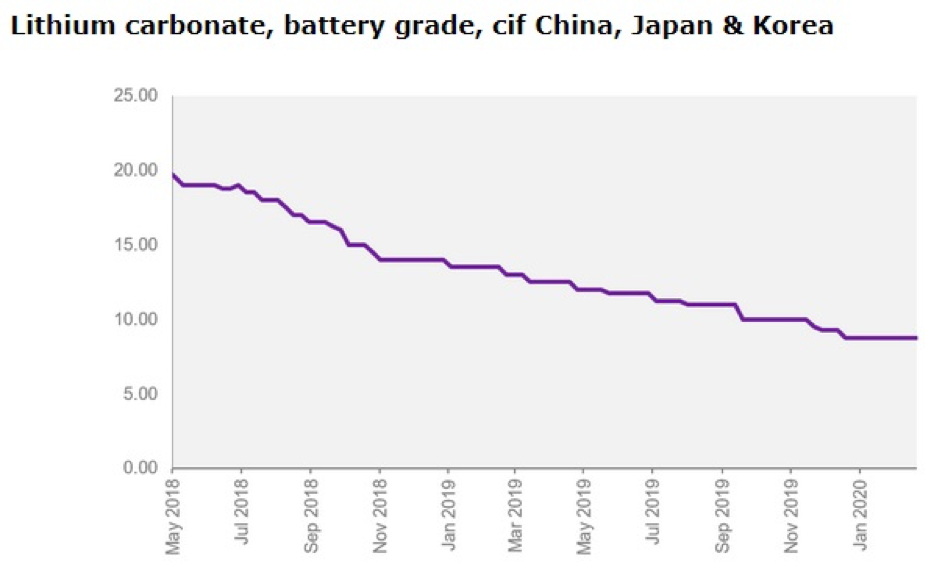

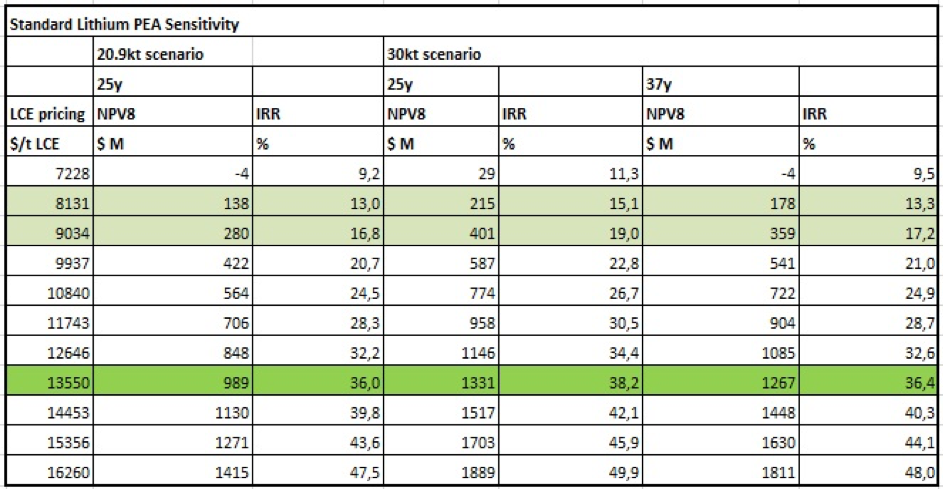

The economics indicate a pretty robust lithium project, at a capex of US$437M. An operation can be constructed with an after-tax net present value (NPV)8 of US$989M and an after-tax internal rate of return (IRR) of 36%, based on an average long-term lithium carbonate equivalent (LCE) price of US$13,550/t.

I already viewed this base-case price as high in the recent past, and the situation for LCE pricing has deteriorated further since then. Fastmarkets quotes an LCE price of US$8,750/t in this useful article of Matt Bohlsen on Seeking Alpha. Benchmark Mineral Intelligence mentions US$7,922/t LCE, so the estimated average would hover at US$8,400/t at this time. The trend is still following a downward path, as can be seen here in this chart from Fastmarkets:

Despite Tesla breaking record after record on the markets (and giving a decent percentage back due to the coronavirus anxiety these days), lithium pricing appears to be negative, on the back of Chinese gross domestic product (GDP) growth issues, which drags down almost all commodities. Therefore, I reworked the lithium sensitivity, where three scenarios are presented, the 20,900t LCE per annum (pa) base case, and the hypothetical 30,000t LCE pa expansion scenarios, as I calculated them in my first article on the company:

An US$8,400/t LCE price would still generate a hypothetical NPV8 of US$183275M, and a hypothetical post-tax IRR of 1416%, which would render the project not economic, as lithium projects usually need an IRR of at least 25%. These figures are based on 100% project ownership economics, and 100% equity financed, which is standard for economic studies or hypothetical estimates like this. In the news release dated Nov, 12, 2018, Lanxess is committed to provide project finance to the JV when testing and the PFS are successful for them, and Standard will probably be an estimated 30% JV partner (according to company documents filed on SEDAR).

At a current market cap of CA$70,99M, the JV share of the NPV8 for Standard is at the moment hovering at the same level, depending on which firm you ask about the current LCE price. So there doesn’t seem to be much upside. However, I do believe Lanxess hasn’t been committing CA$5M for no reason. As it is set to fund full capex, I do believe it is cheaper for Lanxess to buy Standard out at a low point in NPV valuation, and consolidate the entire project. The recent CA$12.1M raise points toward the same direction, as it was a unusually large amount for a lithium junior/developer. I believe something could be going on behind the scenes, and I usually don’t base an investment thesis on a buy-out scenario, but this time it could be different.

Conclusion

With this fresh non-brokered raise of CA$12.1M closed now, another strong vote of confidence in the Lanxess project of Standard was issued recently. I see a takeover as inevitable now, when this kind of money is invested in a lithium junior, an unloved subsector of mining at the moment.

Standard management doesn’t seem to be fazed one second, and is on the road raising cash like it is 2011 or 2016 again. It is almost unbelievable, as about any non-gold company has trouble raising over a few million. Sitting at a full treasury, Standard is cashed up to complete most, if not all, necessary testing at the LiSTR demonstration plant, complete the PFS and await a construction decision from Lanxess. I am curious, too.

I hope you will find this article interesting and useful, and will have further interest in my upcoming articles on mining. To never miss a thing, please subscribe to my free newsletter on my website www.criticalinvestor.eu, and follow me on seekingalpha.com, in order to get an e-mail notice of my new articles soon after they are published.

Disclaimer:The author is not a registered investment advisor, and currently has a long position in this stock. Standard Lithium is a sponsoring company. All facts are to be checked by the reader. For more information go to www.standardlithium.com and read the company’s profile and official documents on www.sedar.com, also for important risk disclosures. This article is provided for information purposes only, and is not intended to be investment advice of any kind, and all readers are encouraged to do their own due diligence, and talk to their own licensed investment advisors prior to making any investment decisions.

Streetwise Reports Disclosure: 1) The Critical Investor’s disclosures are listed above. 2) The following companies mentioned in the article are sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. 3) Statements and opinions expressed are the opinions of the author and not of Streetwise Reports or its officers. The author is wholly responsible for the validity of the statements. The author was not paid by Streetwise Reports for this article. Streetwise Reports was not paid by the author to publish or syndicate this article. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy.