– Economic and social upheaval plus the collapse of oil prices have pushed responsible and impactful investing further into mainstream finance, affirms the CEO of one of the world’s largest independent financial advisory organizations.

The comments from Nigel Green, the chief executive and founder of deVere Group, come as the global coronavirus emergency continues and as oil prices went negative this week for the first time in history.

Mr Green says: “At the start of 2020 I said that Environmental, Social and Governance (ESG) investing would reshape the investment landscape in this new decade – but this phenomenon has been dramatically and irreversibly accelerated by the current situation.

“Even before the start of the Covid-19 pandemic, ESG investments often outperformed the market and had lower volatility over the long-run.

“What is perhaps more impressive is that those investments with robust ESG credentials are still typically continuing to outperform throughout the coronavirus-triggered stock market crashes where major indices were extremely volatile, with some plummeting 20 per cent.

“Clearly, this is going to increasingly attract both retail and institutional investors seeking decent returns in turbulent times.”

He continues: “The collapse of oil prices, which are likely not to rebound to pre-crisis levels in the short-term, has also helped drive ESG investments to the top of the performance charts and keep them there.

“This is because ESG funds circumnavigate oil stocks, so their performance will not be adversely impacted by the fall in share prices.

“There is a wider and growing force behind the rise of Environmental, Social and Governance investing,” says Nigel Green.

“The current situation has acted as a wake-up call in many respects.

“It underscores that human health is reliant upon healthy ecosystems; that we need to ensure the sustainability of supply chains; and that those companies with robust corporate governance and good business practice fare better in difficult times and are ultimately best-positioned for the future.

“This growing collective awareness of mutual responsibility fits perfectly into the narrative of ESG investing.”

The deVere CEO concludes: “The collective wake-up call delivered by Covid-19 plus the search for profits in these highly unusual times are catapulting responsible, sustainable and impactful investing into the mainstream.”

About:

deVere Group is one of the world’s largest independent advisors of specialist global financial solutions to international, local mass affluent, and high-net-worth clients. It has a network of more than 70 offices across the world, over 80,000 clients and $12bn under advisement.

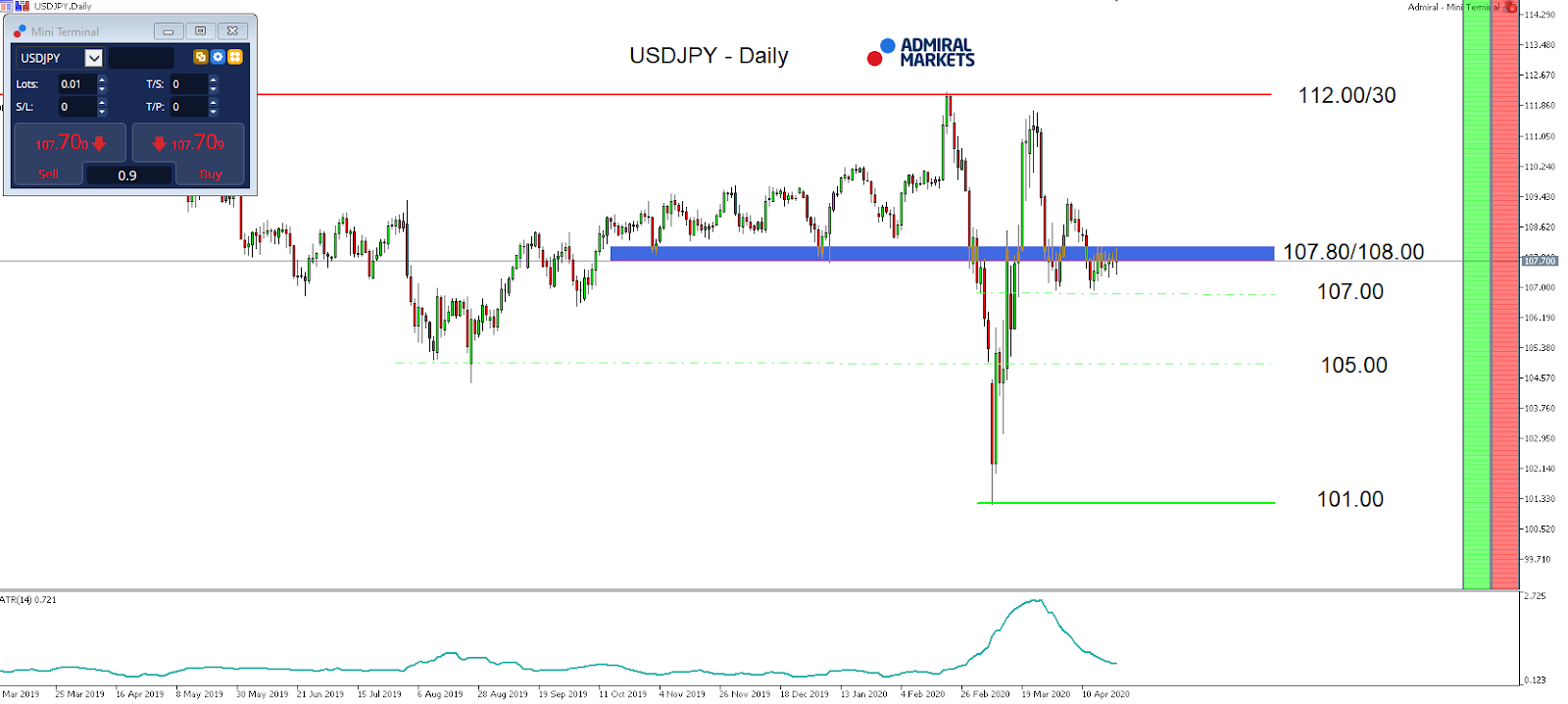

Despite recent volatility in global oil markets, volatility in forex markets remained relatively low, particularly in the USD/JPY. In fact, it seems unlikely that this will change given the pretty thin economic calendar leading up to the weekly close.

Given the drop in the University of Michigan’s consumer sentiment for the US which dropped to 71 in April of 2020 from 89.1, there may be room for surprise. But with expectations for the final print to come in even lower at 68, much of worst-case scenario is likely already priced into the markets, including the USD/JPY.

Still, while the currency pair stays technically choppy, an overall bearish tendency remains.

The main reason for this bearishness is the continuing pressure on 10-year-US Treasury yields, which leaves room in the USD/JPY to test the short-term relevant region of support around 107.00.

A sustainable break wasn’t seen yet, but if we get to see one in the days to come, probably with voices of a bailout of the badly hit US oil industry by the recent turbulence in the oil market growing louder.

A break below 107.00 would technically activate the region around 105.00 as a first target:

Source: Admiral Markets MT5 with MT5-SE Add-on USD/JPY Daily chart (between March 1, 2019, to April 23, 2020). Accessed: April 23, 2020, at 10:00pm GMT – Please note: Past performance is not a reliable indicator of future results, or future performance.

In 2015, the value of USDJPY increased by 0.5%, in 2016, it fell by 2.8%, in 2017, it fell by 3.6%, in 2018, it fell by 2.7%, in 2019, it fell by 0.85%, meaning that after five years, it was down by 9.2%.

Discover the world’s #1 multi-asset platform

Admiral Markets offers professional traders the ability to trade with a custom, upgraded version of MetaTrader 5, allowing you to experience trading at a significantly higher, more rewarding level. Experience benefits such as the addition of the Market Heat Map, so you can compare various currency pairs to see which ones might be lucrative investments, access real-time trading data, and so much more. Click the banner below to start your FREE download of MT5 Supreme Edition!

Disclaimer: The given data provides additional information regarding all analysis, estimates, prognosis, forecasts or other similar assessments or information (hereinafter “Analysis”) published on the website of Admiral Markets. Before making any investment decisions please pay close attention to the following:

This is a marketing communication. The analysis is published for informative purposes only and are in no way to be construed as investment advice or recommendation. It has not been prepared in accordance with legal requirements designed to promote the independence of investment research, and that it is not subject to any prohibition on dealing ahead of the dissemination of investment research.

Any investment decision is made by each client alone whereas Admiral Markets shall not be responsible for any loss or damage arising from any such decision, whether or not based on the Analysis.

Each of the Analysis is prepared by an independent analyst (Jens Klatt, Professional Trader and Analyst, hereinafter “Author”) based on the Author’s personal estimations.

To ensure that the interests of the clients would be protected and objectivity of the Analysis would not be damaged Admiral Markets has established relevant internal procedures for prevention and management of conflicts of interest.

Whilst every reasonable effort is taken to ensure that all sources of the Analysis are reliable and that all information is presented, as much as possible, in an understandable, timely, precise and complete manner, Admiral Markets does not guarantee the accuracy or completeness of any information contained within the Analysis. The presented figures refer that refer to any past performance is not a reliable indicator of future results.

The contents of the Analysis should not be construed as an express or implied promise, guarantee or implication by Admiral Markets that the client shall profit from the strategies therein or that losses in connection therewith may or shall be limited.

Any kind of previous or modeled performance of financial instruments indicated within the Publication should not be construed as an express or implied promise, guarantee or implication by Admiral Markets for any future performance. The value of the financial instrument may both increase and decrease and the preservation of the asset value is not guaranteed.

The projections included in the Analysis may be subject to additional fees, taxes or other charges, depending on the subject of the Publication. The price list applicable to the services provided by Admiral Markets is publicly available from the website of Admiral Markets.

Leveraged products (including contracts for difference) are speculative in nature and may result in losses or profit. Before you start trading, you should make sure that you understand all the risks.

On Thursday the 23rd of April, trading on the euro closed down. Market volatility was high. After breaking the support at 1.0817,the pair dropped further to 1.0756. After this, buyers recovered to reach fresh highs. The euro sharply surged against the dollar after German chancellor Angela Merkel said that this is just the beginning of the coronavirus. By close, the euro had erased all its gains after reports that EU leaders had failed to reach an agreement on an economic recovery fund. The pair returned to 1.0762.

Stock indices also lost ground. They were downed by news that initial trials of a medicine called Rendisivir, developed by Gilead Sciences, had been unsuccessful.

Day’s news (GMT+3):

11:00 Germany: IFO – business climate (Apr), IFO – expectations (Apr), IFO – current assessment (Apr).

15:30 US: durable goods orders (Mar).

17:00 US: Michigan consumer sentiment index (Apr).

20:00 US: Baker Hughes US oil rig count.

Current situation:

The fundamentals are driving the euro. When there’s positive news, it goes up against the dollar, and vice versa. In Friday’s Asian session, the euro hit fresh lows, shedding 0.23%. The major currencies are trading down. Trading on the euro crosses is mixed. Considering that Standard & Poor’s is expected to downgrade Italy’s credit rating today, pressure on the single currency is set to remain at least until the US session. As such, we predict a drop to 1.0708 to the lower line of the channel and the 112th degree. If this drop takes the form of a wedge, we can expect a bounce from around 1.0700/710.

The Dollar index (DXY) was lifted back above the 100.7 psychological level, after the US House of Representatives passed a $484 billion package to support small US businesses. This latest round of funding brings the overall US fiscal response to the coronavirus outbreak to $2.9 trillion, or equivalent of 15 percent of GDP. The Dollar is strengthening versus all G10 currencies on Friday, with the DXY set to register a weekly gain of over 0.8 percent.

However, considering the steady stream of dire economic data, such as US jobless claims now exceeding 26 million in five weeks, it remains to be seen how effective these support measures are against Covid-19’s impact on the economy. Policymakers’ actions thus far can be likened to trying to fill a crater in the dark, as they keep shoveling in trillions without fully knowing the ultimate size of the economic chasm that needs to be filled. Risk-on sentiment may only make fleeting appearances amid such an uncertain environment, as evidence of the outbreak’s peak prove painstakingly hard to come by.

While the overall risk aversion in global markets is expected to fuel sustained demand for the Greenback, its upside appears capped as the Federal Reserve works in tandem with other central banks to keep Dollar-funding pressures in check. As such, the DXY is expected to trade within the 98.5 – 101 range over the near-term, serving as a relative anchor in FX markets amid tremendous volatility in other asset classes.

Euro slides as leaders haggle over EUR 2 trillion rescue plan

European leaders also signed off on a 540 billion Euro short-term package, although it wasn’t enough to support the ailing Euro, as policymakers stall over the larger and longer-term rebuilding plan worth two trillion Euros. The bloc’s currency is extending its decline against the US Dollar amid more signs of economic distress in the EU, with manufacturing activity and confidence levels reaching record lows. ECB President Christine Lagarde has warned that the EU could see an economic contraction of up to 15 percent this year. EURUSD is now pulling further below the 1.08 psychological level, and set to post a weekly loss of about one percent.

Disclaimer: The content in this article comprises personal opinions and should not be construed as containing personal and/or other investment advice and/or an offer of and/or solicitation for any transactions in financial instruments and/or a guarantee and/or prediction of future performance. ForexTime (FXTM), its affiliates, agents, directors, officers or employees do not guarantee the accuracy, validity, timeliness or completeness, of any information or data made available and assume no liability as to any loss arising from any investment based on the same.

– Weeks before the February top in the DJIA, the January Elliott Wave Theorist (Elliott Wave International President Robert Prechter’s monthly publication about financial markets and social trends since 1979) said:

Most economists believe the Fed can prevent financial crises and depressions. [EWI’s analysts] disagree. Socionomic theory proposes that naturally fluctuating waves of social mood regulate financial optimism and the economy. They are unconscious and cannot be managed. [emphasis added]

In case you’re unfamiliar with socionomic theory, socionomics is the study of how society’s changes in mood motivate social actions in realms that include the economy, political preferences, financial markets, actions of peace and war, and the fads and fashions of popular culture. Robert Prechter began formulating socionomic theory in 1976.

Now, let’s get back to the point that the January Elliott Wave Theorist makes about “naturally fluctuating waves of social mood” being unmanageable. Realize that if people’s psychology shifts from expansive to cautious, there’s nothing financial authorities can do about it.

That doesn’t mean that central banks don’t try.

On March 23, after the start of the swift financial downturn, Marketwatch had this headline:

Fed, saying aggressive action is needed, starts unlimited QE

Ironically, on that very day, the stock market declined even further.

But, looking beyond the action of the market, you can also get a good idea about the “fluctuating waves of social mood” from this chart and commentary from our April Elliott Wave Financial Forecast:

Changes in producer prices, a key deflationary indicator that tends to lead consumer prices, are already negative. The chart shows the persistent long-term slowing of U.S. producer prices on what Conquer the Crash maintains has been a steadily waxing precursor to deflation and depression. Noting PPI’s movement back and forth across the zero line, CTC observed that “economists have had difficulty explaining why producer prices have been so sluggish. The short answer is that deflationary psychology is creeping toward gaining the upper hand, no matter what the Fed does.”

It’s evident that a deflationary psychology is taking hold globally.

Consider that PPI measures from January-to-February declined in Germany, China, Japan, the U.K, South Korea, Canada, France and Italy.

The closest that the world has come to deflation in modern times was the 2007-2009 financial crisis. However, the last full-blown deflationary episode was in the early 1930s. As you know, this period is known as the “Great Depression.”

Robert Prechter’s book, Conquer the Crash, explains why deflation, which is a decrease in the total amount of money and credit, goes together with a depression:

A deflationary crash is characterized in part by a persistent, sustained, deep, general decline in people’s desire and ability to lend and borrow. A depression is characterized in part by a persistent, sustained, deep, general decline in production. Since a decline in credit reduces new investment in economic activity, deflation supports depression. Since a decline in production reduces debtors’ means to repay and service debt, a depression supports deflation. Because both credit and production support prices for financial assets, their prices fall in a deflationary depression. As asset prices fall, people lose wealth, which reduces their ability to offer credit, service debt and support production.

Deflation and depressions are rare.

Yet, the swift downturn in global financial markets strongly suggests that this is a time to prepare for the next ones.

This article was syndicated by Elliott Wave International and was originally published under the headline Deflationary Psychology Versus the Fed: Here’s the Likely Winner. EWI is the world’s largest market forecasting firm. Its staff of full-time analysts led by Chartered Market Technician Robert Prechter provides 24-hour-a-day market analysis to institutional and private investors around the world.

The new data are reviewed and updates are provided on Can-Fite BioPharma’s other clinical studies, including one for COVID-19, in this Dawson James research report.

In an April 20 research note, Dawson James analyst Jason Kolbert wrote that results from Can-Fite BioPharma Ltd.’s (CANF:NYSE.MKT) Phase 2 trial of Namodenoson for nonalcoholic fatty liver disease with or without nonalcoholic steatohepatitis “look pretty good.”

He added that “the consistency of the data from the studies (preclinical and clinical), should support business development interest.”

Dawson James has a $9 per share target price on Can-Fite; the stock is currently trading at around $1.75 per share.

Kolbert recapped the study design and provided the results.

This purpose of this multicenter, randomized, double-blinded, placebo-controlled trial involving 60 patients was to determine dose efficacy and safety. Patients were treated twice a day with either 12.5 milligrams or 25 milligrams of oral Namodenoson or a placebo for 12 weeks.

The primary endpoint was effect on inflammation, measured by mean percent change from baseline in alanine transaminase blood levels and safety. The second endpoints included the percent change from baseline in liver fat, as determined by MRI proton density fat fraction.

In terms of safety, study participants tolerated Namodenoson at both doses, and no adverse events were reported. Otitis media occurred in two patients but was deemed to be unrelated to the drug. The four other events that occurred that were drug related were mild and self-limited.

Regarding efficacy of Namodenoson, Kolbert noted that “for a small Phase 2 exploratory study, there appears to be a significant efficacy signal.”

Kolbert provided updates on other Can-Fite clinical trials.

The company’s COVID-19 trial is now designed. Plans call for it to be randomized, open label, and double armed with Piclidenoson administered plus standard supportive care, compared to standard supportive care alone, in 40 hospitalized COVID-19-infected patients with moderate to severe symptomatic disease.

Patients are to be randomized at a 1:1 ratio to one of the trial arms and treated for up to four weeks. The primary efficacy measures will be time to resolution of viral shedding, time to resolution of clinical symptoms, respiratory function, need for ventilatory support and overall mortality.

Piclidenoson, Can-Fite’s lead drug candidate, also is in Phase 3 in two indications: moderate to severe rheumatoid arthritis (the ACROBAT study) and moderate to severe plaque psoriasis (the COMFORT study). Enrollment for both trials is more halfway complete. In both, Piclidenoson “hold great promise as alternative therapies with what appears to be a more favorable side effects profile,” Kolbert commented.

Dawson James has a Buy rating on Can-Fite BioPharma.

Disclosure: 1) Doresa Banning compiled this article for Streetwise Reports LLC and provides services to Streetwise Reports as an independent contractor. She or members of her household own securities of the following companies mentioned in the article: None. She or members of her household are paid by the following companies mentioned in this article: None. 2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. 3) Comments and opinions expressed are those of the specific experts and not of Streetwise Reports or its officers. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. 4) The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases.

Disclosures for Dawson James Securities, Can-Fite BioPharma Ltd., April 20, 2020,

The Firm does not make a market in the securities of the subject company(s). The Firm has NOT engaged in investment banking relationships with CANF in the prior twelve months, as a manager or co-manager of a public offering and has NOT received compensation resulting from those relationships. The Firm may seek compensation for investment banking services in the future from the subject company(s). The Firm has received other compensation from the subject company(s) in the last 12 months for services unrelated to managing or co-managing of a public offering.

Neither the research analyst(s) whose name appears on this report nor any member of his (their) household is an officer, director or advisory board member of these companies. The Firm and/or its directors and employees may own securities of the company(s) in this report and may increase or decrease holdings in the future. As of March 31, 2020, the Firm as a whole did not beneficially own 1% or more of any class of common equity securities of the subject company(s) of this report. The Firm, its officers, directors, analysts or employees may affect transactions in and have long or short positions in the securities (or options or warrants related to those securities) of the company(s) subject to this report. The Firm may affect transactions as principal or agent in those securities.

Analysts receive no direct compensation in connection with the Firm’s investment banking business. All Firm employees, including the analyst(s) responsible for preparing this report, may be eligible to receive non-product or service specific monetary bonus compensation that is based upon various factors, including total revenues of the Firm and its affiliates as well as a portion of the proceeds from a broad pool of investment vehicles consisting of components of the compensation generated by investment banking activities, including but not limited to shares of stock and/or warrants, which may or may not include the securities referenced in this report.

Analyst Certification: The analyst(s) whose name appears on this research report certifies that 1) all of the views expressed in this report accurately reflect his (their) personal views about any and all of the subject securities or issuers discussed; and 2) no part of the research analysts compensation was, is, or will be directly or indirectly related to the specific recommendations or views expressed by the research analyst in this research report; and 3) all Dawson James employees, including the analyst(s) responsible for preparing this research report, may be eligible to receive non-product or service specific monetary bonus compensation that is based upon various factors, including total revenues of Dawson James and its affiliates as well as a portion of the proceeds from a broad pool of investment vehicles consisting of components of the compensation generated by investment banking activities, including but not limited to shares of stock and/or warrants, which may or may not include the securities referenced in this report.

The ways in which Moderna is to use the funds are explained and an update on its coronavirus vaccine is provided in a ROTH Capital Partners report.

In an April 19 research note, ROTH Capital Partners analyst Yasmeen Rahimi reported that the Biomedical Advanced Research and Development Authority (BARDA) awarded Moderna Inc. (MRNA:NASDAQ) $483 million in funding, in part for development of its COVID-19 vaccine, mRNA-1273.

Rahimi discussed how Massachusetts-based Moderna will use the funds, which will be provided in tranches to reach certain milestones.

Half of the $483 million award will be used to help cover clinical development costs of mRNA-1273, from trial operations to the filing of a biologics license application.

Currently, the vaccine is in Phase 1 in the clinic. Recently, the biopharma decided to add to the study a cohort of patients aged 51 years and up, which “will be key for demonstrating mRNA-1273’s safety and immunogenicity in this vulnerable population,” Rahimi noted.

The analyst explained that for mRNA-1273 to advance to Phase 2, the results from Phase 1 must be optimal. The data must demonstrate the vaccine is safe and tolerable. They must show that the vaccine produced a sufficient number of neutralizing antibodies, crucial for stopping viral replication and proving the vaccine’s method of action. Phase 1 safety data from the group aged 1855 years are expected in spring followed by immunogenicity results, likely in mid-July or early August.

Rahimi relayed that as soon as safety data are available, Moderna plans to launch a Phase 2 study of mRNA-1273 rather than wait for the remaining results to become available, according to CEO Stéphane Bancel.

“Pending favorable safety data from Phase 1, we point out that a potential Phase 2 study would enroll hundreds of patients, and that the BARDA funding could potentially allow Moderna to pursue trials in patient populations who are at greater risk, such as patients who have underlying comorbidities, those who are overweight and patients with cancer,” commented Rahimi.

Moderna will spend the second half of the $483 million BARDA funding on the engineering and optimization work required to scale up the manufacturing of its messenger RNA (mRNA).

“With the current focus on SARS-CoV-2 and mRNA-1273, Moderna was now able to present BARDA its strategic plans (amount, time and people) of how to be ready for commercial launch,” wrote Rahimi. “This preparation was likely helpful in expediting discussions with BARDA and awarding of the grant.”

Also regarding mRNA production, Ginkgo Bioworks, a company with expertise in organism biology and genetically engineering bacteria to replace certain industrial applications, is helping Moderna optimize certain parts of the process.

Rahimi, who is closely tracking COVID-19 data, highlighted that April 18 was the first day in five on which the daily death tally, 1,867, was less than that predicted by Dr. Christopher Murray’s model, 2,194.

Disclosure: 1) Doresa Banning compiled this article for Streetwise Reports LLC and provides services to Streetwise Reports as an independent contractor. She or members of her household own securities of the following companies mentioned in the article: None. She or members of her household are paid by the following companies mentioned in this article: None. 2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. 3) Comments and opinions expressed are those of the specific experts and not of Streetwise Reports or its officers. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. 4) The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases.

Disclosures from ROTH Capital Partners, Moderna Inc., Company Note, April 19, 2020

Regulation Analyst Certification (“Reg AC”): The research analyst primarily responsible for the content of this report certifies the following under Reg AC: I hereby certify that all views expressed in this report accurately reflect my personal views about the subject company or companies and its or their securities. I also certify that no part of my compensation was, is or will be, directly or indirectly, related to the specific recommendations or views expressed in this report.

Within the last twelve months, ROTH has received compensation for investment banking services from Moderna, Inc.

ROTH makes a market in shares of Moderna, Inc. and as such, buys and sells from customers on a principal basis.

Within the last twelve months, ROTH has managed or co-managed a public offering for Moderna, Inc.

ROTH Capital Partners, LLC expects to receive or intends to seek compensation for investment banking or other business relationships with the covered companies mentioned in this report in the next three months.

Maurice Jackson of Proven and Probable speaks with Andy Schectman, president of Miles Franklin Precious Metals Investments, about the present situation with physical precious metals.

Maurice Jackson: Today, we’re going to discuss precious metals premiums, the COMEX and the big picture. Joining us for a conversation is Andy Schectman, the president of Miles Franklin Precious Metals Investments.

Andy, investors in physical precious metals are upset with high premiums over spot for precious metals. Can you discuss the reasoning behind the high premiums, the supply chain, and just a number of the intangibles that really go into what’s causing premiums to soar at records highs above and beyond the spot price?

Andy Schectman: I believe we are experiencing a realization of a very large fear that I have. And let me try to explain. I think most of the readers will have noticed the tremendous volatility in the stock market recently where the market may be up 1,000 or 2,000 points one day and down 1,000 or 2,000 points the next day.

When you look at the pre-market trading often and you’ll see things like Caribbean Cruise Line and Norwegian Cruise Line. Now, that to me, stinks of the Fed coming in and buying up the stocks as they said they would do via (MOPE), I call it Management of Perception Economics.

When the stock market isn’t crashing, it’s not the end of the world for all of us locked in our homes not working, at least we can feel the world is normal when the stock market is going higher, quite frankly. I think it’s very telling what the Federal Reserve is doing because it is supposed to be a reflection of the economy and the forward guidance of the economy.

But suffice it to say or let me say I digress. But let me tell you what I think is happening. That volatility is very scary to me for one reason. And if we look at what’s happened since 2008, the Federal Reserve has made money very easy and has flooded the world with dollars and low interest rates in an effort following the Keynesian economic model to spur economic activity.

The Keynesian economic model that the West it finds itself under is one based upon consumption, debt and spending. When you shut off the consumption and the spending and all you’re left with is a mountain of debt, you have problems.

And one of the reasons why I think the Federal Reserve is trying to keep things together by buying up the stock market amongst many other things that they’re buying these days, but suffice it to say, as the stock market moves up, what I believe we see happening is a culmination of 12 years’ worth of easy money has inflated all of the asset prices.

And so, when the stock market moves up now, when people have already watched 35% of their wealth vaporize in a matter of 10 days earlier in the month, there’s a great deal of fear and especially for the baby boomers. And what I see happening is a transition from asset price inflation, which we saw over the last 12 years in stocks, bonds and real estate, to price inflation.

We are witnessing it no better place than in the precious metals market. In other words, what I see happening is people, in particular the older people, who have made a lot of money over the last 12 years due to the Fed policy, that when the market shows any strength at all they’re selling.

They’re selling on strength, and they’re coming out and now they have money to do something with, which will translate into price inflation, and you’re seeing it with precious metals. In other words, you have a broken supply chain. You have a whole bunch of money chasing the items in the broken supply chain, pushing premiums up higher than I have ever seen in my 30-year career.

And I’m getting phone calls that go something like this. And by the way, in 30 years, I’ve never gotten any of these phone calls. But the call goes something like this. Mr. Schectman, I just cashed out of the stock market, I have $2 million to spend, what should I do? I’m hearing that every single day now repetitively. And I guess what I’m very concerned about is a tremendous amount of price inflation in this industry. Now the question becomes, is it too much or isn’t it? And I don’t know how to answer that simply to say this, if things don’t change very soon, I am very, very, very certain that within a couple of months, there’ll be nothing left in this industry for anyone to buy.

In 1980, the average allocation to precious metals was 8%; that was the last time we saw the Dow Jones and the price of gold cross at 800. Since then, the average allocation to precious metals amongst the United States portfolios is now 0.5%.

If everyone who had $100,000 were to pull just $2,500 out of their portfolio and buy gold with it, this industry would experience a fivefold increase in demand from what it already has right now. And within a few days there would be nothing left to buy.

We have a supply chain that from the very top is broken. Most of the mines across the globe or many of them are shut down. The refineries in Zurich are shut down. The Royal Canadian Mint and the U.S. Mint have had to close down operations.

So, you put it all together you have a tremendous amount of money fleeing financial assets and looking in search of somewhere safe. The first place they’re looking at is precious metals. And that price inflation, which means that we have to look harder, search further, and pay way more money to get the product to retail buyers just to have something to sell is a problem the industry is facing right now.

Are we paying too much to buy it? Am I my charging too much to clients when we have to pay three, four times what I normally do? And the answer, as far as I’m concerned, is no. But the bottom line is unless things change, the price really doesn’t matter. Investors should focus on the following: it’s not about the dollar value, it’s about having ounces of gold and silver. And if they cost more to buy now, I can only imagine what will happen if the demand continues to increase and the supply chain does not get fixed anytime soon. So that’s the question that people need to ask themselves.

Yes, the premiums are high. I’ve been buying it every two weeks for 30 years and my last purchase of Gold Eagles was the highest I’ve ever paid in 30 years premium wise, but didn’t bother me because what I see coming is a complete destruction of the supply chain.

And if that happens, then getting gold at any price will be next to impossible. So, that’s the dilemma we all have to face. Is it going to get fixed anytime soon? If the answer is yes, then premiums will come down. If the answer is no, premiums will only go higher and then disappear altogether.

Maurice Jackson: I’m glad you referenced that because I think sometimes someone who’s buying or looking to buy precious metals, they are forgetting that you and I are active buyers. We don’t want to pay that premium.

Andy Schectman: No, we don’t.

Maurice Jackson: In regards to premiums, readers may wish to consider the following: what can you buy that’s below its 1980 high? If you put that into proper perspective, I’m referring to silver in this case. Even with the premium as it is, you’re still purchasing below its 1980 high. That to me still is a great value proposition.

Andy Schectman: Well, I can’t think of another asset on the planet you can say that about.

Maurice Jackson: If buyers factor in the aforementioned catalysts and are not satisfied with the premiums now, I can only imagine as things continue to progress this way a period of time, we will look back in 6 to 10 months from now and say premiums were low in April 2020.

Andy Schectman: I agree with you 100%, They say there’s no bull market like a gold bull market for one reason, and that is that every other bull market appeals to people’s greed. They want to make money. And very often it’s conventional wisdom that when you double your money in equities, you pull your initial principal out and play with the house money that’s smart, and I agree with that.

But in this industry, the higher the price goes only reinforces people’s concern and fear and so nobody sells. We’ve done record volume of business over the past six weeks, nearly six months-plus worth of business. And in that time, there have been less than five people who have sold anything. There is no one selling anything. This is all people buying. And so, I’m concerned for the long-term viability if indeed this doesn’t get better anytime soon.

Something we all need to consider. When we look to the 1918 Spanish flu pandemic, the second wave killed six times as many people as the first.

There’s a big push by a lot of people to get everyone back to work and get the economy going and I understand that. And, gosh, I would give up so much of everything I’ve done over the past six weeks, all of it if we could go back to normalcy and sit at a bar with a buddy and watch the NCAA tournament and I 100% mean that.

But the bottom line here is that if things don’t get any better anytime soon, I am all about convinced that gold and silver will be near if not completely and totally impossible to find.

Interesting to note, this is not the first time that mints have not been able to meet demand. There have been several instances in my career when nobody was buying gold but we ran into major problems with the five major mints of the world, U.S., Canada, South Africa, Australia and Austria, where they just could not keep up with demand. So things have the potential to get ugly really fast based on these demand levels. You start putting a lot of mainstream demand on this fear on top of that, and supply chain problems on top of that, and literally, there’ll be nothing to get. And I’m concerned about that because nobody’s selling product. I have to pay way more to find anyone who will be willing to sell it.

And when that ends, look, you’ve got mints in North America, the United States and Canada. Canada was shut down for two weeks and the U.S. mint is in New York. So, the potential of those all but just ceasing operation to me is fantastic; it could totally happen. So, these are real issues, let alone the infrastructure here in the United States, delivering packages into Seattle, into Manhattan. How does that work?

I’m not sure how this plays out. We’ve never experienced anything like this, nobody has. In 2008, when the precious metals markets behaved this way, premiums went to the moon, product disappeared, people were scared with plunging markets, the Fed stepped in, goosed the markets, lowered interest rates and flooded the market with money, and it should have stopped shortly thereafter but it continued unabated until now. I don’t see a soft landing in this anytime soon.

And I guess I will just simply say that the premiums right now are not the issue. The issue is what makes this end? How does this end? When does it end? And if de-dollarizing and mitigating exposure to the dollar in the equity markets is important to people, if they’re waiting for the price to pull back, waiting for premiums to come down, I think they’re making a monumental mistake.

And I hope I’m wrong, I really do. Let me put through this way, if someone wanted to spend $10 million right now, and we are one of the only companies who has had product, I don’t think we could place the order right now other than locking in the metal price on the COMEX market with futures contracts and filling it as product came in.

Now, that’s almost embarrassing. We’re a company that in a bad year does $200 million in sales. We did almost $100 million in sales in the last six weeks. So, I would say to you, what has been normal is no longer normal, and it’s concerning me greatly.

Maurice Jackson: Speaking of the COMEX, how does the COMEX play into this?

Andy Schectman: The COMEX is breaking. And this is another thing to be worried about. People always used to say the COMEX will default because of the rehypothecation. And the term rehypothecation, means that each bar is sold multiple times over to different people.

And the reason you could do that on the COMEX market is that most people don’t stand for delivery. Almost everything is legitimate, hedge and it’s cash settled. What happened for the April contract is really very enlightening and illuminating.

I think it could be the beginning of the end for the COMEX. Let me explain. Typically, 5,000 to 6,000 contracts stand for delivery out of all the contracts they have and the COMEX deals in hundred-ounce gold bars. So, that’s still a lot of gold, 50,000, 60,000 ounces of gold that stand for delivery, that’s a lot of gold.

But this time, it was 28,000 contracts, 2.8 million ounces of gold stood for delivery, and the COMEX market didn’t have all the bars. And so, they changed the rules in midstream. Now, if I were one of those people that stood for delivery, I’d say, where’s my 100-ounce bar that it says that I own?

Now, coincidentally, this is what the Hunt brothers did in 1980 when they realized there were more contracts issued than bars in the vault. But suffice to say what the COMEX did was they changed the verbiage saying, you may have to settle for a fractional interest in the 400-ounce gold bar, then those are traded in London.

London trades 400-ounce gold bars supposedly where there’s more gold and a big stash, and Chicago trades 100-ounce gold bars. But the point of it is that when 28,000 plus contracts stood for delivery, many of them were not granted and it had to be settled in a fractional interest in the 400-ounce gold bar.

I’m not sure how they plan on doing that, cutting it with a saw or recasting it into 100-ounce bars. But when that happened, the two markets decoupled. And I have seen it over the last couple of weeks as the price diverged $50 an ounce.

In other words, COMEX says the price is $1,688. London says the price is $1,733, and London has the bars. And so, in reality, what that is saying is that the COMEX market is being exposed for being a fraud. And the price that they say that it is, which is, by the way, the world Western mechanism, the price setting mechanism of the West is being exposed for being a scam and not what it is.

Now, if I were a trader, I would suspect you’ll see in the next delivery month, which I think is in June, I would think you would see a massive amount of people try to stand for delivery. And if that happens, my expectation is of force majeure and cash settlement.

And really the beginning of the end of the COMEX market, maybe you see price set at the Shanghai Gold Exchange, or maybe it moves to London, or maybe they just change the rules all over again and try to become a little bit more accurate with what’s going on with the price. But anyway, the bottom line is the COMEX market is beginning to break and here’s another reason to be concerned.

Maurice Jackson: Now, does that favor someone who currently owns physical precious metals right now?

Andy Schectman: Yeah, absolutely. Because right now, the actual price of gold is $1,702.40. If you go to Kitco, it will still show it at 1,687, or somewhere in that neighborhood. The point of it is that London is telling us right now that the price is higher than what COMEX is saying it is. And if COMEX doesn’t have the gold and London does, then what is the real price?

Maurice Jackson: Interesting dynamics. Now, we started off at the 10,000-foot level with premiums and then we moved up to the 20,000 with the COMEX. Let’s take it now to the big picture to the 30,000-foot level. What can you talk to us about the big picture that you see? Because you’re a big thinker. You’re exposed to a lot of information that many of us wish we only had access to. So, just give us a glimpse of what you’re seeing.

Andy Schectman: Well, I’ll tell you, I’m here again. And I don’t mean to be a purveyor of doom and that’s why I wanted to preface things by saying I don’t speak this way, but I’m very concerned. I’m working 20-hour days since mid-February because I really believe this is an important time to be working hard and helping people.

And the thing is this, the Western economies are based upon a Keynesian economic model. Now, gold bugs would prefer a model that was Austrian based, which is you build a society like a brick house with investment, savings and reinvestment.

And if you do that, it’s got a solid footing, like the three little pigs. Our house in the West, Keynesian model is based out of straw, it is based out of debt, consumption and spending. And there’s record debt over $285 trillion in global debt, which doesn’t even take into account the derivatives, which are a big problem all together.

The Keynesian based system works just fine when the engine of growth is working, you can go into debt. And as long as you’re able to finance that debt and service that debt, everything is fine. And look around you, no one really owns anything anymore.

It seems everyone’s got auto debt and student debt and mortgage debt and credit card debt. And well, that’s how you get record levels of debt. And not to mention the national debt of $24 trillion, the tremendous amount of stimulus that the Fed is putting in and the Treasury is putting in, pushing our deficit to $7 trillion this year.

A trillion seconds ago was nearly 32,000 years ago. So, we have so much debt that is being carried by spending and consumption throughout the entire Western world. If you shut off spending and consumption, lock it in its house for two, three months at a time, that debt collapses upon itself.

And what makes me very, very nervous is that we’re entering a period of time where that debt cannot be serviced by anyone. And so we are heading toward what appears to be a massive depression. What frightens me is what I started out with earlier, big money pulling out of the stock market, looking for a safe place to put their funds, and it will translate into price inflation across the board.

It may manifest itself in precious metals first, but you’ll see it in things like food and medicine and things that we need will become harder to get in a compromised supply chain with tons of money looking for somewhere safe to put it.

Not to mention the tremendous amount of monetization of assets and printing of money by the Federal Reserve, which will find its way into the real economy creating a hyperinflationary scenario, which I am afraid will turn into hyper-stagflation, which has little or no economic growth characterized by rising prices.

It’s a horribly painful experience. It’s a depression meeting hyperinflation. No one has a job. No one has any money. Everyone has debt that’s collapsing upon itself. And the big money that is pulling out of the collapsing equity market is looking for somewhere safe to put it.

They’ll buy up everything they can in this compromised supply chain, and all of that money will push the prices of the few items available too high for most of us to afford. It’s very concerning, Maurice. This is very concerning. It’s no joke. This is different than anything we’ve ever seen before.

So, the bottom line is, I really hope I’m wrong. But in that scenario, it doesn’t get any better before it gets probably a whole lot worse. And I think that all we can do right now is trying to mitigate our exposure to the dollar, go to cash, get out of harm’s way of the stock market.

Remember that the second wave of Spanish flu killed six times as many people as the first wave. So, if people are jumping back into the market and they sounding you’re all clear this spring, God forbid, we see it come back stronger for the second wave. You can only imagine what that would do to the stock market. And I think that what this is doing is breeding a whole generation of people who are terrified.

The stock market is based on spending and consumption. And if spending and consumption die, all you have is world-record debt that will collapse. And with that, our standard of living will as well. So, I hope I’m wrong, but something tells me I’m not and that’s the reason it doesn’t matter what the premiums are and what you’re paying, you need to get out of harm’s way.

One should really consider buying gold and silver. It should have been bought before when it was cheap, but it’s not anymore. And now, you have to ask yourself, is this the beginning of a new extended reality or isn’t it? And if it’s not, sit back and wait for the correction and the lower premiums.

But if you think that it is, it’s time to move now. And if nothing else, get out of harm’s way of financial assets and go to cash. To me, that is the best advice I could give anyone because the traditional wisdom of waiting for this to correct, you have time on your side, don’t worry, it always comes back. The old term normalcy bias, this isn’t normal anymore. This is not anything like we’ve ever experienced ever, ever, ever before. All of the corrections and problems we’ve seen before were issues of liquidity. This is anything but a liquidity problem. I don’t care if they drop bundles of $1,000 bills out of a helicopter. It’s not going to stop people from being terrified to go and spend it.

It’s not going to open up the small businesses or the restaurants or the movie theaters or any of the things that once were and we took for granted; it’s going to take a long time to get back to that. And until that happens, our economy is in big trouble. And to expect it to go back to normal anytime soon I think is foolhardy. I wish it were. But here again, hopefully, we all survive this healthy. But what it’s going to do to the economy I’m afraid will take a long time to come back from. And you know what, it may never ever come back the way that it was.

Maurice Jackson: You reference so much here. Let’s talk about reality. I have an 11-year-old son and nine-year old twins. And they ask my wife and I, when was the last time this happened when you couldn’t go outside? Our reply: Never. This is unprecedented. This is unprecedented.

The psychological warfare that goes on here with the markets, with the people, you’re absolutely correct. I believe you’re being 100% responsible. And anyone that follows our work is aware that I don’t believe in using fear tactics to sell precious metals.

I believe in being responsible. And just using the ratios and trying to buy something that’s on sale, and what’s the best value proposition and try to keep it simple. If you study monetary history, it is difficult to refute what you have been conveying.

In reference to precious metals, there’s one more thing I want to ask you about, because again, I know you’re in these discussions and you know people that that have so much influence on the world. Will there be a country that will create a currency backed by precious metals, most likely gold. Who would it be? And do you think that’s a likely outcome?

Andy Schectman: I’m so glad you asked that question. And, I mean, I don’t want to talk conspiracy. I know how you feel about that. And I’m not going to but let’s just talk coincidental.

So, if we understand that the whole Western world is Keynesian based, how do you blow up a system that is so far indebted, accumulated at the lowest interest rates in human history without really blowing it up? You keep everyone from spending and then the debt absolutely collapses upon itself, and everyone’s debt collapses at the same time.

Everyone faces the same misery and pain at the same time. If you notice, when Nancy Pelosi a couple of weeks ago came out with her House Finance Subcommittee proposal, in it was the digital dollar proposal, a Fed wallet of sorts.

Because evidently, the virus is enabled to live on currency, I guess. And I don’t know for how long or the veracity of that. But that’s the general thought that the virus can live on currency. And so, now, that gives them the ability to go to a digital dollar, something that everyone’s always talked about, I could never figure out how they would get rid of cash.

Well, certainly the whole Western world would be happy to get rid of cash if they felt that the virus lived on it. And I think you could very well see that. But more ironic than that is the reclassification of gold as the only other tier one asset in the world by the Western central banks a year ago almost to the day, Basel III.

I find it interesting that in April of 2019, the Bank of International Settlements, the central bank of central banks, reclassified gold and not a Special Drawing Rights from the International Monetary Fund or euros or anything else, they chose gold. So, you have rumblings of a digital currency, you have unrefutable tier one assets of gold after 80 years receiving the same classification as the U.S. dollar and Treasuries.

So, if you told me that all debt in the Western world would be forgiven because it all implodes at the same time, culpability of the people who arguably did this with the repeal of Glass-Steagall, the trade act that allowed the savings and loan banks like JP Morgan and Goldman Sachs to become investment banks at the same time.

The high frequency trading, the derivatives, all of these financial instruments that have created the mess that we are finding ourselves in, not to mention all of the record debt, $285 trillion in global debt, which doesn’t include the many hundreds of trillions of derivatives, all accumulated at ultra-low interest rates.

The only way to blow it up is to keep everyone from spending in the collapses all at the same time. The misery both physically and financially is felt the same across the globe. All debt then be forgiven a new digital currency free from the virus backed by gold.

If you told me that was going to happen, I would believe that. And one of the things I’ve believed for a long time is in that scenario, the East will come out with a currency backed by gold as well. We’ll have two currency systems, one in the east, one in the west.

The BRICS nations, for someone that’s not familiar with the term that’s Brazil, Russia, India, China and South Africa, are financial allies and they’re looking to make a new currency basically to compete with the Federal Reserve note. They have already taken steps to ensure this with a system that mirrors the SWIFT system that the BRICS nations have created that much of Europe is signing on to. And let’s not forget about the Shanghai Gold Exchange and the Chinese petroyuan.

The Chinese petroyuan is already taking steps to usurp the U.S. petrodollar. Chinese petroyuan is a bond that the Chinese buy oil with from countries like Iran and natural gas from countries like Russia. They pay for it in a bond denominated in yuan that is then immediately convertible into gold on the Shanghai Gold Exchange.

And that’s probably why the Shanghai Gold Exchange has delivered over 90 times more gold than the COMEX says in the past two years. So, you’re seeing countries try to usurp the dollar in trade agreements, in purchasing energy, setting up a system that usurps the SWIFT system, which is if you transact in dollars, you have to be in the SWIFT system.

And I would think that the likelihood of the currency in our pocket that we call dollar bills, hanging from a museum frame in the Smithsonian Museum in the next few years is likely. Whereby, everything is digital. Everything is monitored and tracked and followed.

And the gold backing would enable people to be able to swallow the Kool Aid once again. Because I don’t think you would have mass adoption certainly without resistance of a new currency after what is happening right now based upon the mismanagement of the dollar over all these years.

But again, the virus gives all of the mismanagement to cover of culpability. There is no culpability for the people who did this because it never would have happened if it weren’t for the virus. And it happens throughout the entire world. So, everyone experiences the same pain all at the same time.

Now, if you really want to go down the rabbit hole and make the assumption that this was released and this isn’t from a bat in the wet market, then you probably would also agree that they already havewhoever “they” area vaccine.

Now, there are rumblings if you watch the Bill Gates’ TED talk that just came out, they took a part of it out. And there are people on YouTube who have the original video. And at the very end of it, Bill Gates is saying, everyone will need a digital certificate of vaccination in order to get on airplanes and do all sorts of stuff.

That’s his opinion of what’s happening. And in that scenario, the vaccine would be sold to the pharmaceuticals enriching whomever released it for generations, and everyone would have to be vaccinated every single year. Now, I don’t say that I subscribe to this ideology, but I will simply just say this that there are a lot of coincidences here.

And in particular, the thoughts of a digital dollar, the reclassification of gold as a tier one asset for the first time in the last 80 years, and the possibility of all debt being forgiven. And if you believe this was done intentionally, then you have to believe that whoever did this unintentionally as God awful as that is, probably already has the cure, God willing.

And again, please, I am not saying I believe this, I’m just simply saying I talk to people all day long who do believe this. And the rabbit hole can take you to some deep, dark places. But there is no other better answer as to how to stop a Keynesian based society than to lock everyone in from spending and consuming.

And the mountain of debt just collapses upon everyone at the same time. And so, forgiveness would be accepted if everyone suffered at the same time. There is no, well, that country didn’t suffer and we did, this as we all suffered. Let’s start over. Let’s have a new system and start fresh.

If you told me that was going to happen, I believe it, And I hate to even think this way. But when you’re locked up in your house and have nothing but time on your hands and talk to people all day long who are very concerned and believe a lot of this to be true, I think there’s a fine line between conspiracy in reality and somewhere the truth lies somewhere between that and what you see on CNN. There is some conspiracy in every bit of reality these days, I believe.

Maurice Jackson: All right, Andy. We’ve gone to the 10,000-foot level, the 20,000 and the 30,000. Let’s descend the interview back down to 10,000 feet. And let me ask you again, you referenced it earlier. What are you buying right now and why?

Andy Schectman: I’m buying Gold Eagles. I’m buying one-ounce silver bars and coins. Partially because there’s not a lot to choose from. Also, because I think that you want to keep it as simple as possible and if it’s available. But one-ounce Gold Eagle is the most recognized coin in the world.

And quite frankly, I wouldn’t keep a large amount of money in the banks. We haven’t even talked about the repo market prices. But the Federal Reserve is putting $1 trillion per night into the repo market, which is the overnight lending system between the banks because the banks don’t trust one another.

Here again, rehypothecation of assets. They don’t trust each other’s collateral; they’re backing away from each other. The Federal Reserve to keep the banks liquefied and the hedge funds from blowing up. And these massive derivative books that are all based upon a set of assumptions in interest rates and counterparties ability to perform while interest rates are at the lowest level in human history.

And counterparty risk is growing exponentially by the day with all these corporate entities in lockdown and business suffering, derivatives are going to blow up. The Federal Reserve is putting as much as we spent in over 15 years in the Gulf War, every single night into the overnight lending market.

Things are very, very upside down and in disarray. And I think the worst thing to do is have the huge amount of exposure to the banks or to the dollar or to the stock market. So, I don’t care if I had $2 million to spend right now. I wouldn’t put it in the bank. I wouldn’t put it in the bond market. I wouldn’t put it in the stock market. I would put it into gold and I wouldn’t care what I paid to do it. I can put it into silver and I wouldn’t care what I paid to do it. Silver is the most undervalued commodity on the planet.

As you said, it’s the only asset on the planet that is trading at a third of what it was in 1980. And gold, because it was reclassified as the tier one asset because the central banks are accumulating the crap out of it. To me, the only thing that I have confidence in for the long game, I don’t have confidence in the dollar as we know it, and don’t have confidence in the stock market as we know it.

And I certainly don’t have confidence for the mother of all bubbles, that’s the bond market, which can only go one of two ways negative and then their bonds will go up, or interest rates go up for some unforeseen reason like a new gold backed currency from the BRICS.

And overnight you would see interest rates spike so high you couldn’t believe it. So, for me, I’m buying gold and silver in any form I can get, currently some Gold Eagles and silver bars and one-ounce Eagles.

Maurice Jackson: Interesting. And just for the record, what I’m buying, I’m buying those Australian Dragons and my strongest allocation the last 3-4 years and continues to be towards platinum.

Andy, please share how someone may contact you and or Miles Franklin Precious Metals Investments.

Andy Schectman: I can be reached at andy@milesfranklin or call 800-255-1129. Please reference you read this interview with Maurice. I pride myself at accessibility. We do publish a daily newsletter. Sometimes, it’s three or four days a week but a semi-daily newsletter, which can be found at our website, www.milesfranklin.com.

We do not sell online so you will have to contact Maurice ([email protected] or call 855.505.1900) or myself. And I understand that frustrates some people because I believe identity theft, online fraud is only a problem that’s getting worse. I believe gold and silver acquisition it belongs in the analog world, not in the digital world.

I think in a world that as rapidly changing as it is, relationships are very important. And you never realize how important it is until there’s a problem, which I’d like to mention one more thing. I’m sorry, to do this. But one last thing. There’s been a big slowdown in the industry from all of the companies in delivering product that is not anywhere near fraud on all of our parts.

All of the shipping departments across the whole spectrum are practicing social distancing, what normally is 20 or 30 or 40 or 50 people boxing things up are now 2, 3, 4, or 5 now working 30, 40, 50 feet apart. And that same thing goes with the major mints.

And that’s because if one person gets it, the whole place gets shut down for a few weeks and deep cleaned and then the whole thing goes pear shaped. So, please understand. Delays in shipping are normal right now. But everything will be delivered.

Maurice Jackson: And you referenced some good points here something that I think we didn’t reference yet. And I want you to just clarify the importance of being licensed, insured and bonded.

Andy Schectman: The precious metals industry, it’s federally nonregulated. That means it’s the wild west. Minnesota is the only state in America where you have to be licensed, bonded and background checked. We have a very large 30 bond annual background checks of everyone, Maurice, myself, all employees annually.

And some clients and continuing education that no other state in the United States mandates. Whether you own a company in Minnesota, or own one in another state doing it and selling into Minnesota, you would have to be subservient to the same set of regulations, we are to the Commissioner of Commerce.

Therefore, most of the companies outside of Minnesota won’t sell into the state because of that licensing requirement. What it means is, you cannot do business in this industry in a more safer manner than with a company in Minnesota. And hopefully, it will be with ours.

Maurice Jackson: A lot of us that are shopping around that are reading to this program. You may see a fancy website, but there’s some things that you need to make sure they before you purchase. Are they licensed? Are they insured? Are they bonded? And another thing is, are they providing you education? Are they preparing you, other than just price? And that’s something to consider. And it goes without saying, we are more than happy to price match an online competitor if there is a rare occasion where they have a lower price.

I welcome the opportunity to earn your business. Please call me, Maurice Jackson at 855-505-1900, or you may email [email protected]. And ladies and gentlemen to my clients. They all know this, I am available to them 24 hours a day, 7 days a week.

Finally, we invite you to subscribe to www.provenandprobable.com. We provide mining insights and bullion sales.

Andy Schectman of Miles Franklin Precious Metals Investments, thank you for joining us today on Proven and Probable.

Andy Schectman: Thank you, Maurice. You take care of yourself and your family. And I hope to talk to you again real soon.

Maurice Jackson is the founder of Proven and Probable, a site that aims to enrich its subscribers through education in precious metals and junior mining companies that will enrich the world.

Disclosure: 1) Statements and opinions expressed are the opinions of Maurice Jackson and not of Streetwise Reports or its officers. Maurice Jackson is wholly responsible for the validity of the statements. Streetwise Reports was not involved in the content preparation. Maurice Jackson was not paid by Streetwise Reports LLC for this article. Streetwise Reports was not paid by the author to publish or syndicate this article. 2) This article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 3) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases.

Proven and Probable LLC receives financial compensation from its sponsors. The compensation is used is to fund both sponsor-specific activities and general report activities, website, and general and administrative costs. Sponsor-specific activities may include aggregating content and publishing that content on the Proven and Probable website, creating and maintaining company landing pages, interviewing key management, posting a banner/billboard, and/or issuing press releases. The fees also cover the costs for Proven and Probable to publish sector-specific information on our site, and also to create content by interviewing experts in the sector. Monthly sponsorship fees range from $1,000 to $4,000 per month. Proven and Probable LLC does accept stock for payment of sponsorship fees. Sponsor pages may be considered advertising for the purposes of 18 U.S.C. 1734.

The Information presented in Proven and Probable is provided for educational and informational purposes only, without any express or implied warranty of any kind, including warranties of accuracy, completeness, or fitness for any particular purpose. The Information contained in or provided from or through this forum is not intended to be and does not constitute financial advice, investment advice, trading advice or any other advice. The Information on this forum and provided from or through this forum is general in nature and is not specific to you the User or anyone else. You should not make any decision, financial, investments, trading or otherwise, based on any of the information presented on this forum without undertaking independent due diligence and consultation with a professional broker or competent financial advisor. You understand that you are using any and all Information available on or through this forum at your own risk.

The Wuhan virus outbreak, and the economic lockdowns that spread globally because of it, have accelerated the trend toward a digital economy.

Suddenly millions more people are working from home, through their internet connections. Millions more are also relying on Amazon for their shopping needs.

Jeff Bezos’ empire had already put most brick-and-mortar bookstores out of business. Now Amazon, together with Walmart, threaten to put most other retailers out of business – especially those that have been deemed “non-essential” during this crisis.

Even pizza delivery is being forever changed. “Contactless delivery” has entered our lexicon. Germophobes and others who fear infection from their fellow human beings will likely continue to expect and demand contactless ordering and payment methods even after this virus pandemic has run its course.

New shopping habits being developed during the crisis will be slow to revert. Particularly when there is newfound convenience.

Government and corporate technocrats, meanwhile, are accelerating their push to ultimately replace all physical cash transactions with contactless digital payment methods.

They may now claim it’s about public health (viruses and bacteria can be transferred by paper banknotes), but for years, the “powers that be” have been waging a war on cash for other reasons – chiefly to eliminate the privacy afforded by cash transactions.

For years leading up to this opportunistic moment, an organized campaign to ban cash has been spearheaded by the so-called Better Than Cash Alliance. It includes financial companies, government agencies, billionaire globalists, and NGOs that are all eager to abolish cash transactions.

Citi is a member of the Better Than Cash Alliance, as are the Bill & Melinda Gates Foundation, Clinton Development Initiative, and various groups linked to the United Nations where the Better Than Cash Alliance is based.

“As the tragic human costs of COVID-19 mount, the need for practical, scalable, quick and effective solutions is urgent. Now more than ever, it’s time to put digital payments to work,” wrote Ruth Goodwin-Groen, Managing Director of the Better Than Cash Alliance.

If this cabal gets its way, then it will be difficult for anyone to earn a living or even buy groceries outside of the purview of the digitally integrated banking system. Since it may become nearly impossible to take withdrawals from a bank account in cash, those who want to purchase anything without connecting electronically to the financial matrix may have to learn how to barter.

“Clearly digital channels deliver vast benefits in terms of speed, accuracy, efficiency, and are best when delivered responsibly,” Goodwin-Groen continued.

Who decides what “responsible” payment technologies are? The bankers and bureaucrats who are ushering in centralized cashless, contactless systems.

Presumably, decentralized, peer-to-poor blockchain systems such as Bitcoin are “irresponsible.” Some members of Congress have openly called for it to be banned.

Unfortunately for Bitcoiners, the cryptocurrency hasn’t gained any ground in terms of price or acceptance during this pandemic. Bitcoin and other cryptos remain speculative digital assets more than practical means of payment for everyday things.

With much of the world’s population being locked down and relegated to online activities, it could have been Bitcoin’s moment to break out into the mainstream. Instead, it has languished while a more ancient form of money – gold – has outperformed.

While few people use precious metals in transactions, the primary function of gold and silver in the digital age is to serve as a real store of value. All purely digital currencies and government-issue fiat currencies lack any intrinsic value.

The touted speed and efficiency with which digital money can be deployed is also a liability.

If the Federal Reserve can run its digital printing press to create trillions of new U.S. dollars overnight during a crisis, the well-founded fear that it will be undertaken again and again until finally the currency loses credibility.

Unbacked digital currencies are even more prone to abuse than unbacked paper currencies.

Communist China is now testing a blockchain-based digital currency to better track and control social behavior.

Whether it’s the People’s Bank of China or the U.S. Federal Reserve, central bankers are keen on giving themselves more power to manipulate economic outcomes.

According to Bloomberg Tax, “Some economists say that without cash, central banks could fight recessions more effectively because they’d have an effective way to impose negative interest rates — basically a tax on savings meant to spur spending. Critics say that in a digital-only economy, governments and banks could take control of your financial life, leaving you penniless with a flick of a switch.”

Precious metals held in physical form are the perfect antidote to the digital-only future now being pushed by our self-appointed overlords in the name of combatting the novel virus.

Silver coins, in fact, naturally repel pathogens and are far more sanitary than paper bills, plastic credit cards, and smartphone surfaces.

Silver and gold are also likely to increase exponentially in value versus the Federal Reserve Note and other national currencies as the push to replace physical cash with electronic digits ushers in a great debasement.

The Money Metals News Service provides market news and crisp commentary for investors following the precious metals markets.

With the supply/demand balance moving in favor of miners, the outlook for uranium stocks is the brightest it has been in years, according to McAlinden Research Partners.

SUMMARY: Uranium has been enjoying a stealth bull market due to the coronavirus outbreak. Temporary mine closures to slow the spread of the virus at production facilities have triggered an unexpected supply squeeze, sending the price of uranium up nearly 30% since the beginning of March. According to one analyst, half of global production has been cut. With the supply/demand balance moving in favor of miners, the outlook for uranium stocks is the brightest it has been in years.

An ongoing supply shock is moving the uranium market’s demand/supply balance in favor of miners, strengthening their pricing power in the process.

2020 Supply Shock

The world relies on four countries for 75% of its uranium supply: Kazakhstan (40% of global supply), Canada (13%), Australia (12%) and Namibia (10%). What’s more, about 65% of global output is sourced from just six mines. Following the example of millions of other businesses around the planet, some of those mines have temporarily suspended operations to slow the spread of COVID-19 infections at their facilities.