By Hussein Sayed, Chief Market Strategist (Gulf & MENA), ForexTime

Asian equities kicked off Monday trading on a positive note with most benchmarks rising more than 1%, led by a 2.5% rally in the Nikkei 225. US equities also indicated a higher open for the day with the Dow Jones Industrial Average and S&P 500 futures contracts rising 1% and 0.9% respectively at the time of writing.

The Bank of Japan took another step forward on easing monetary policy by announcing a commitment to buy an unlimited amount of government bonds, quadrupling its purchases of corporate debt and lowering the criteria for what debt qualifies.

Central banks’ readiness to ’do whatever it takes’ to save their economies has led to a steep rally in global equities with many major indices up more than 20% from their lows, in what qualifies as a bull market. However, to understand the real economy’s performance and how terrible the situation is at the moment, you only need to look at oil prices. WTI for June delivery declined 11% early this morning to fall below $15, while Brent is trying to hold above $20 after a 4.3% decline. Investors are worried that we will revisit the crash levels from last week when May’s WTI delivery contract plummeted to -$40 a barrel.

Storage capacity is being tested like never before and if demand doesn’t pick up in May, we’re likely to hit negative prices again as we approach the next delivery date. But with coronavirus death rates slowing in hard-hit cities in Europe and the US and governments moving to re-open economies, there is hope of some demand recovering. Whether it is enough to provide a boost to prices remains to be seen, but a slight pickup in demand along with the expected drop in supply may at least prevent prices from falling again into negative territory.

Investors are also keen to know what steps will be taken next by the Federal Reserve and European Central Bank later this week. For the ECB, it’s widely expected to raise its limits for asset purchases and continue to pressure Eurozone governments for further fiscal stimulus measures. We are also expecting to see further discussions related to creating a bad bank, which is clearly needed to confront the upcoming recession.

The Fed is not likely to announce anything new on Wednesday. After successfully calming the markets with several unscheduled policy decisions, it is time to hear the FOMC’s outlook on the US economy and what additional action can be taken if the situation deteriorates further.

Disclaimer: The content in this article comprises personal opinions and should not be construed as containing personal and/or other investment advice and/or an offer of and/or solicitation for any transactions in financial instruments and/or a guarantee and/or prediction of future performance. ForexTime (FXTM), its affiliates, agents, directors, officers or employees do not guarantee the accuracy, validity, timeliness or completeness, of any information or data made available and assume no liability as to any loss arising from any investment based on the same.

Global equities are advancing today with countries gradually relaxing lockdown measures. Reopening of economies boosts investors’ risk appetite as the week with busy corporate reporting schedule starts with resumed oil prices slides.

Forex news

Currency Pair

Change

EUR USD

+0.21%

GBP USD

+0.47%

USD JPY

-0.31%

AUD USD

+0.94%

The Dollar weakening accelerated today as former Minnesota Federal Reserve President Kocherlakota said over weekend Federal Reserve should take interest rates below zero for the first time ever. The live dollar index data show the ICE US Dollar index, a measure of the dollar’s strength against a basket of six rival currencies, lost 0.2% Friday as US orders for durable goods slumped 14.4% in March. The EUR/USD joined GBP/USD’s continued rising Friday with both pairs higher currently. AUD/USD continued climbing Friday while USD/JPY continued sliding with the dynamics intact for both pairs currently.

Stock Market news

Indices

Change

Dow Jones Index

+1.03%

Nikkei Index

+1.96%

Australian Stock Index

+1.28%

US Dollar Index

-0.24%

Futures on three main US stock indexes are higher currently after the Friday rebound. Investors are trying to gauge the possible path of US economy with mixed corporate results and weak data checking traders’ risk appetite. 3 million Americans are skipping mortgage payments and millions of credit card customers can’t pay their bills and lenders are bracing for the impact while Georgia, Oklahoma and Alaska began loosening coronavirus lockdown orders. US economy faces historic shock with 16% joblessness possible, Trump adviser said Sunday. More companies including United Technologies, Honeywell and Boeing will report quarterly results today. Stock indexes in US ended higher on Friday : the three main US stock indexes recorded gains ranging from 1.1% to 1.6% led by technology shares. European stock indexes ended lower Friday but are rising currently as European governments ease lockdowns. Germany is slowly reopening, Spain relaxed lockdown after seven weeks of home confinement. Asian indexes are solidly higher today after Bank of Japan said it will buy an additional 15 trillion yen ($140 billion) of government bonds, commercial paper and bank loans : Nikkei jumped 2.7%, leading the general trend.

Commodity Market news

Commodities

Change

Brent Crude Oil

-6.04%

WTI Crude

-13.03%

Brent is adding to Friday’s losses today on signs that worldwide oil storage is filling rapidly. Oil prices ended mixed last session. The US oil benchmark West Texas Intermediate (WTI) futures ended higher Friday: June WTI gained 2.7% but is falling currently. June Brent crude closed 0.5% lower at $21.44 a barrel on Friday, booking a 23.7% loss for the week.

Gold Market News

Metals

Change

Gold

-0.45%

Gold prices are edging higher today. June gold lost 0.6% to $1735.60 an ounce on Friday.

Note: This overview has an informative and tutorial character and is published for free. All the data, included in the overview, are received from public sources, recognized as more or less reliable. Moreover, there is no guarantee that the indicated information is full and precise. Overviews are not updated. The whole information in each overview, including opinion, indicators, charts and anything else, is provided only for familiarization purposes and is not financial advice or а recommendation. The whole text and its any part, as well as the charts cannot be considered as an offer to make a deal with any asset. IFC Markets and its employees under any circumstances are not liable for any action taken by someone else during or after reading the overview.

We have just witnessed an oil price crash like never before taking prices of West Texas Intermediate into deeply negative territory.

The spot price of West Texas, the US benchmark, reached minus US$40.32 a barrel and the May futures price (which is deliverable in a physical form) went to minus US$37.63 a barrel, the lowest price in the history of oil futures contracts.

There has been no better indicator of the extent of the economic impacts of coronavirus. With borders closed and much of the world’s population being urged to stay at home, transport has come to a near halt.

How can a price turn negative?

The industry has not been able to slow production fast enough to counter the drop in demand. The other mechanism that normally stabilises prices, US oil storage, appears to be nearing capacity.

West Texas Intermediate is typically stored at the Cushing facility in Oklahoma which is on the way to being full.

Cushing is said to be able to hold 62 million barrels of oil – enough to fill all the tanks of half the cars in United States.

That’s why prices have gone negative. Traders with contracts to take delivery of oil in May fear they won’t be able to store it. They are willing to pay not to have to take it and have nowhere to put it.

Not all oil contracts went negative. West Texas Intermediate contracts for June and subsequent months are still positive, reflecting a feeling that the supply and demand imbalance will soon be corrected.

Brent, the international price benchmark, remained positive, dropping to US$25.57 – a fall of about 9%. Unlike West Texas Intermediate, Brent deliveries can be put on ships and transported to storage facilities anywhere in the world.

Not confined to the US

There is no guarantee the problems of storage evident in the US won’t spread to other markets.

This is despite the decision of OPEC-Plus (the mainly Middle Eastern member of the Organisation of the Petroleum Exporting Countries plus Russia and other former Soviet states) to respond to the free fall by cutting output by 9.7 million barrels per day, ending the recent duel over production levels between OPEC and Russia.

Adding another element to the COVID-19 story, on March 9, the day of the Black Monday stock market crash, the Chicago Mercantile Exchange reported a new daily record for West Texas Intermediate trading, reaching 4.8 million contracts, surpassing the 4.3 million recorded on September 2019 following the drone attacks on Saudi oil facilities.

The future does not look good. With rising unemployment, stuttering economies, and collapsing financial markets the prospects for substantial recovery in the oil markets seems far away.

The US, these days an exporter itself through shale oil, will suffer in the same way as traditional exporters in the Middle East.

Historically, oil markets have been considered good at predicting recessions, although in this case the causation might go the other way.

At this point the industry might be starting to consider that the best place to store oil is a natural one – leaving it in the ground.

– Precious metals have become the focus of many researchers and traders recently. Bank of America recently raised its target to $3000 for gold (source: https://www.bloomberg.com). In December 2019, we published a research article suggesting precious metals were setting up a long-term pattern that should result in a big breakout to the upside for gold. Every trader must understand the consequences and market dynamics that may take place if Gold rallies above $2500 over the next few months.

An upside price breakout in precious metals that has been predicted by our researcher and dozens of other analysts suggests broad market concern related to future economic growth and global debt. There is no other way to interpret the recent upside price move in Gold. Back in 2015, Gold was trading near $1060 per ounce. Currently, the price of gold has risen by nearly 64% and is trading near $1740. If gold breaks higher on a big upside move (possibly to levels above $2100 initially), this would complete a 100% upside price move from 2015 lows and would set up an incredible opportunity for further upside price legs/advancements.

Before we continue, be sure to opt-in to our free market trend signals before closing this page, so you don’t miss our next special report!

Daily Gold Chart Fib Arcs & Tesla Price Amplitude Arcs

This Daily Gold chart highlights our proprietary Fibonacci/Tesla Price Amplitude Arcs and our Adaptive Fibonacci Price Modeling system. Although the chart may be a bit complicated to understand, pay attention to the GREEN ARC with the MAGENTA HIGHLIGHT near current price levels. This is a key price resistance arc that is about to be broken/breached. Once this level is breached with a new upside price advance, the $2100 price level becomes the immediate upside price target.

These Fibonacci Price Amplitude Arcs have become a very valuable tool for our researchers. They act as price resistance/support bubbles/arcs. When they align with price activity as price advances or declines, they provide very clear future price targets and levels where the price will run into resistance/support. Currently, the Price Amplitude Arc is suggesting that once Gold rallies above $1775, the next leg higher should target the $2000 price level, then briefly stall before rallying to levels above $2100.

Weekly Gold Chart

This Weekly Gold chart highlighting the longer-term price picture paints a very clear picture for Gold traders. Once $1775 has been reached and the Magenta level has been broken, Gold should rally very quickly to levels above $2000, then target levels above $2100 within a few more weeks.

It doesn’t matter what type of trader or investor you are – the move in Gold and the major global markets over the next 12+ months is going to be incredible. Gold rallying to $2100, $3000 or higher means the US and global markets will continue to stay under some degree of pricing pressure throughout the next 12 to 24 months. This means there are inherent risks in the markets that many traders are simply ignoring.

I keep pounding my fists on the table hoping people can see what I am trying to warn them about, which is the next major market crash, much worse than what we saw in March. See this article and video for a super easy to understand the scenario that is playing out as we speak.

If you want to learn more about the Super-Cycles and Generational Cycles that are taking place in the markets right now, please take a minute to review our Change Your Thinking – Change Your Future book detailing our research into these super-cycles. It is almost impossible to believe that our researchers called this move back in March 2019 in our book and reports.

As a technical analyst and trader since 1997, I have been through a few bull/bear market cycles in stocks and commodities. I believe I have a good pulse on the market and timing key turning points for investing and short-term swing traders. 2020 is going to be an incredible year for skilled traders. Don’t miss all the incredible moves and trade setups.

Subscribers of my ETF trading newsletter had our trading accounts close at a new high watermark. We not only exited the equities market as it started to roll over in February, but we profited from the sell-off in a very controlled way with TLT bonds for a 20% gain. This week we closed out SPY ETF trade taking advantage of this bounce and entered a new trade with our account is at another all-time high value.

I hope you found this informative, and if you would like to get a pre-market video every day before the opening bell, along with my trade alerts. These simple to follow ETF swing trades have our trading accounts sitting at new high water marks yet again this week, not many traders can say that this year. Visit my Active ETF Trading Newsletter.

We all have trading accounts, and while our trading accounts are important, what is even more important are our long-term investment and retirement accounts. Why? Because they are, in most cases, our largest store of wealth other than our homes, and if they are not protected during a time like this, you could lose 25-50% or more of your entire net worth. The good news is we can preserve and even grow our long term capital when things get ugly like they are now and ill show you how and one of the best trades is one your financial advisor will never let you do because they do not make money from the trade/position.

If you have any type of retirement account and are looking for signals when to own equities, bonds, or cash, be sure to become a member of my Long-Term Investing Signals which we issued a new signal for subscribers.

Ride my coattails as I navigate these financial markets and build wealth while others lose nearly everything they own during the next financial crisis.

Hello again, and welcome to another edition of the Weekly Market Wrap Podcast, I’m Mike Gleason.

Well, just when you thought you’d seen it all in markets, this week brought something that was previously assumed by many to be impossible: a negative price for a physical commodity.

More on that in a bit. But first, let’s review this week’s market action in precious metals, which have been posting some positive gains since bottoming last month.

Gold prices are up 0.9% since last Friday’s close to bring spot prices to $1,720 per ounce. Silver shows a weekly decline now of 1.8% to trade at $15.13 an ounce as of this Friday recording. Platinum is putting off by 2.4% decline for the week to bring the per ounce price to $768. And finally, palladium looks lower this week by 6.4% and currently comes in at $2,074.

The metals complex showed relative stability this week as the oil market suffered a historic meltdown. West Texas Intermediate Crude crashed 70% at one point this week on the continuous contract, bringing prices briefly below $7 per barrel. By Thursday, prices were trading between $14 and $18 per barrel.

The volatility on the May futures contract was even more extreme. On Monday, May futures for crude oil crashed to one dollar, then to zero, then to a few pennies below zero, then to an unbelievable negative $37 per barrel.

With the world literally running out of places to store oil, oil contracts for immediate physical offtake represented a liability rather than an asset. Nobody wanted to take delivery of oil. That left speculators, hedge funds, and exchange-traded funds that hold oil futures as financial instruments only needing to unload their contracts at any price. They ultimately would rather pay buyers to take unwanted barrels of oil than assume the obligation and hassle of owning them.

Some traders cried foul over the apparent forced selling and filed complaints with the CME Group, which runs the world’s largest commodity exchange, and the U.S. Commodity Futures Trading Commission. Billionaire oil executive Harold Hamm of Continental Resources wrote a letter to the CFTC calling for the agency to investigate possible market manipulation.

CME Group Chairman Terry Duffy responded on CNBC by insisting the futures market was functioning just fine and had not mispriced oil contracts when they began trading below zero.

CNBC Anchor: There was one that comment he put in his letter to the CFTC. He asked them to investigate whether there had been market manipulation or failed systems or computer programs that played a part in our going negative. If they carried out that investigation, can you answer what they’d find for us now?

Terry Duffy: You know, the CME, we are a neutral facilitator of risk management, and we’re happy if people want to look into the markets. Futures contracts have been around for hundreds of years and I will tell you since day one, everybody knows that it’s unlimited losses in futures. So, nobody should be under the perception that it can’t go below zero.

Regardless of whether the market was manipulated, the deeply negative futures price was disconnected from physical reality.

Nobody could call up an oil producer and expect to be able to buy barrels of oil for less than nothing because of a negatively trading futures contract. No oil company announced to investors that its oil assets had suddenly become liabilities because of a negative futures quote. In fact, energy stocks traded higher this week.

Although many oil producers are losing money at the moment, it’s not because they are literally selling oil at a negative price. It’s because their production and storage costs are exceeding the real-world prices they can fetch for their product.

And that real-world price is now in the teens per barrel. The absurd negative $37 figure on a particular futures contract was never seen as a credible gauge of the global value of physical oil.

The credibility of the gold and silver futures markets is also being called into question. Earlier this month the spread between COMEX gold futures and the London so-called spot price grew to a record high of more than $80.

Something strange is going on. The COMEX and London markets curiously changed their rules to allow 400-ounce gold bars located in London to be substituted for delivery of 100-ounce gold bars in satisfaction of U.S. contracts, actions which have drawn the attention of Congressman Alex Mooney of West Virginia.

Rep. Mooney is now demanding the CFTC explain why U.S. markets are permitted to carry so little deliverable physical gold and silver to back the exchanges. If there are widespread defaults, it could throw the entire financial system into chaos.

At the same time, an enormous divergence between spot prices and the prices on bullion coins, bars, and rounds have developed.

So, what is the real price of gold? What is the real price of silver?

The answer is that it depends on the form in which it is traded. Paper contract settlements carry one price. Bullion bars carry another. And American Eagles carry yet another.

For example, while the silver spot price closed at $15.36 on Thursday, Silver Eagles were selling for $27 or more at Money Metals’ higher-priced competitors. Certainly a few of these dealers are getting greedy or struggling with insufficient capital, but the elevated premiums in general DO reflect extraordinarily strong retail demand on the one hand – and on the other, higher sourcing costs and U.S. Mint closures that threaten to crimp supply.

Coin values cannot be manipulated arbitrarily on a futures exchange. No physical bullion product will suddenly acquire a negative price because a handful of traders desperately need to unload contracts at a particular time and can’t find buyers.

As long as you aren’t using leverage, your downside risk in bullion is limited. That’s certainly not the case if you choose to play gold and silver futures. There, as you heard the head of the CME/COMEX admit, you could potentially lose more than 100% of the capital you deploy.

The upshot for holders of physical is that in the event the highly leveraged precious metals futures markets lose credibility, and especially if they melt down and default on obligations to deliver, a squeeze on available inventories of physical metal could push bullion prices explosively higher – regardless of what the paper quotes for gold and silver happen to be.

Well that will do it for this week. Be sure to check back next Friday for our next Weekly Market Wrap Podcast. Until then this has been Mike Gleason with Money Metals Exchange, thanks for listening and have a great weekend everybody.

The Money Metals News Service provides market news and crisp commentary for investors following the precious metals markets.

US oil is suffering unprecedented distress, as demonstrated by the benchmark West Texas Intermediate (WTI) crude price crashing into negative territory. This is a “triple black swan” of an oversupply of oil driven by Opec and Russia, COVID-19 demand destruction, and having nowhere to store it.

Oil traders reacted on April 20, the day that May forward contracts for WTI crude were due to settle. Many offloaded their contracts at any price to avoid taking delivery of oil they couldn’t store, and the May WTI price plunged to US$-37.53 (£-30.36). Now attention has turned to the June price, which is just under US$15, still the lowest in decades.

Though prices will rebound, the bigger question concerns long-term viability. US oil companies have feasted on a decade-long diet of rampant liquidity thanks to very low short-term interest rates and quantitative easing. With many able to finance and refinance drilling with a breakeven price of US$40 and above per barrel?, this brought into play lots of shale oil, whose fracking requirements are far costlier than basic onshore oil.

This tripled US oil production in the past decade to become world number one, overtaking Russia and Saudi Arabia. Around two-thirds is shale, which is now in big trouble. Of the 16% of US companies that are “zombies”, meaning cash flow doesn’t cover their debts, a good proportion will be in oil. Oil companies’ loans will be based on assumptions about prices that definitely won’t include the current levels. Companies also finance themselves by issuing corporate bonds at the lowest investment grade. These are vulnerable to being downgraded to junk, causing borrowing costs to rise sharply.

Even “normal” onshore drilling looks challenging today, with over two-thirds of Texas wells uneconomic at prices below US$25 by some estimates. Rigs are shut down as there is nowhere for oil to go, globally.

The value of US energy companies in the S&P 500 has halved in 2020 to US$633 billion, less than half that of Microsoft. Research firm Rystad Energy predicts up to 533 bankruptcies by the end of 2021 if WTI prices average US$20, a massive increase from 2019. So where do things go from here?

The road to Black April

Opec, led by the Saudis, controls substantial portions of global oil. It tries to set oil prices by raising or cutting production. For the past three years, Opec has been making these decisions in a formal alliance with Russia and other nations that is known as Opec Plus.

Two events caused the current crisis. Saudi Arabia flooded the market with oil in March after Russia refused to sanction any further Opec action to raise the price. This caused a price war just when COVID-19 was crushing world oil demand. Prices fell hard.

To some, the Russians and Saudis were playing a “good cop, bad cop” routine to drive US shale out of business, with the Saudis playing protector of global prices and the Russians, wounded by US economic sanctions, refusing to play ball. Either way, both have much to gain by knocking out pricier US shale. Meanwhile, China has been buying up Saudi and Russian oil on the uber cheap, while delaying on promises to buy US oil.

Some say the Saudi-Russia price warriors miscalculated America’s response. President Trump used threats like hefty oil tariffs to secure a new Opec Plus deal to cut production by 10% on April 12. This was bolstered by production cuts from other G20 countries. Yet prices kept falling: arguably the deal was more about allowing Americans to save face rather than seriously committing to production cuts, and therefore higher prices and stability.

With a sniper’s precision, some believe, Saudi oil tankers are timed to reach New Orleans in May to unload a 50 million barrel “oil bomb” into Saudi-owned US refineries. There is precious little space for existing American crude, much less Saudi imports, hence the April 20 historic price drop.

Uncle Sam to the rescue?

Trump has said the US is devising a rescue plan to save its oil industry. As part of its US$2 trillion stimulus package, rescue moves could even include buying stakes in firms, though negotiating with congressional Democrats looks difficult.

An alternative is to “virtually” buy more US oil and await better days, paying production companies to keep it in the ground – possibly by designating this part of the US strategic petroleum reserve. This would help contain jobs devastation and help Trump in vote-rich Texas and other key areas, while pleasing contributors to his campaign war chest. Another option is retaliatory tariffs on Saudi oil refined in America, or even a full ban.

Oil companies are restructuring hastily – assessing the value of reserves, and asking creditors for debt waivers. The US government has helped by extending companies’ ability to offset losses against future tax liabilities, which can make them more attractive to buyers.

Nonetheless, some companies sitting on the priciest oil will get liquidated. In other cases, big creditor banks could take over businesses, or demand mergers and acquisitions, including consolidations.

The biggest uncertainty is how long until the oil price rebounds? With the economy only likely to reopen gradually, demand will stay low for some time while supply remains too high. The futures markets expect WTI to bounce back to the high US$20s by the end of the year, but don’t foresee a return to even US$40 oil until December 2024.

How much US shale oil is worth saving in these straitened circumstances is key. Some estimate as many as 70% of firms will go out of business overall, with some never coming back until oil stabilises above US$50. Others may be taken over by companies prepared to wait for higher prices. As oil historian Daniel Yergin says, “Rocks don’t go bankrupt”. US shale is in a sort of death pageant, and will probably remain that way for the foreseeable future.

Peter Epstein of Epstein Research discusses the macro picture for precious metals prices and one junior who he believes will benefit from higher prices.

Timing is everything. Precious metals are up when almost everything else is down. Gold has soared 38% from last year’s low. This is a big move, but few investors seem to appreciate its significance. Earlier this week, Bank of America announced a gold price target of US$3,000/oz by the end of 2021. While that might sound too aggressive, today’s price of US$1,740/oz. = ~C$2,463/oz. is already quite strong.

The current price is more than enough for well managed juniors, with attractive projects, in safe and prolific jurisdictions, to thrive. Right now, some of the best precious metal jurisdictions, as measured by low-costs plus ample exploration upside, include parts of Mexico, Canada and Australia.

In an April 13, 2020, Myrmikan Research investment letter, manager Daniel Oliver made strong arguments that gold and silver prices are headed higher, perhaps much, much higher. Mr. Oliver has been published in Forbes, The Wall Street Journal, The Washington Times, Real Clear Markets, National Review, among others. He has a J.D. from Columbia Law School and an MBA from INSEAD.

“ the magnitude of the dollar debt overhang is so largetens of trillionsthat policy makers cannot practically prevent the inverted credit pyramid from tipping over. The result is a panic more intense by magnitudes than 2008 or 1929. Gold does well on a relative basis, but falls in nominal terms.”

In the second scenario,

“ .trillions of dollars does little to help local businesses and the working class. Wall Street, however, is not just saved, but levers up bailout largess to create spectacular increases in asset prices. Gold spikes in nominal terms as it did from 2009 to 2011 under similar conditions. Gold mining equities soar .”

Finally, in the third scenario,

“ .the Fed’s helicopter drop of dollars precipitates a currency crisis. Gold bullion rockets toward $10,000 per ounce. Gold miners (especially marginal, higher risk players) have breath-taking increases, last experienced from 1978 to 1981.”

Oliver believes the first scenario is by far least likely to unfold, an end-of-the-world type of event that we need not focus on because the world would be over . The remaining two paths are bullish, and extremely bullish, respectively for physical gold and silver and precious metals juniors.

Make no mistake, just because Dan Oliver and a growing cadre of investment experts are talking up precious metals doesn’t guarantee the price will shoot to the moon or even rise from current levels. However, giant hedge, mutual and generalist funds are looking closely at precious metals and the companies that explore for, develop and mine them.

Relative value funds have plenty of industry sectors to avoid, but only a few that offer potential upside combined with low correlation to, and diversification from, the overall market. Glowing reports of precious metals’ fabulous future are a lot more palatable given that a tsunami of global debt obligations will be issued, with no end in sight.

As bad, or perhaps even worse, is governments’ willingness, in a blink of an eye, to direct their central banks to print absurd amounts of money out of thin air. Combined, debt plus unfunded and under-funded liabilities will explode much higher. Not by tens or hundreds of billions, but by trillions of dollars. It’s no longer just a theory (ongoing unbelievably large and unsustainable debt), the pandemic has made it a certainty.

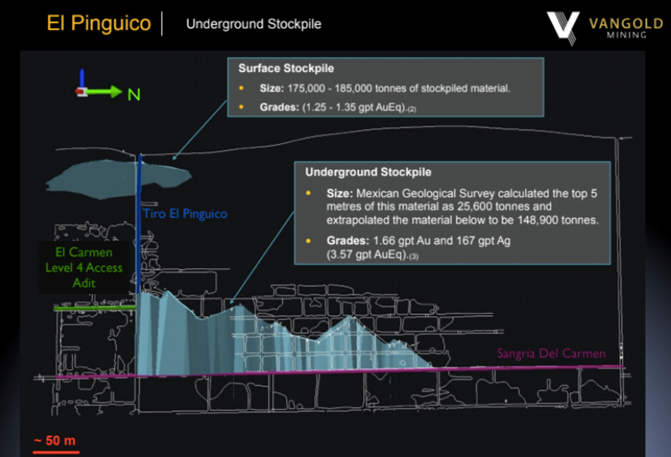

Vangold Mining has many positive attributes. Its 100%-owned silver-gold project is in a safe and desirable location in central Mexico, the state of Guanajuato. At its peak in the 18th century, the mines of Guanajuato, especially the world famous Valenciana mine, were considered the largest and richest on the planet. In the 50 years from 1760 to 1810, Guanajuato (mostly from Valenciana) often accounted for 20% of global silver production, primarily from a single extraordinarily rich vein. {corporate presentation}

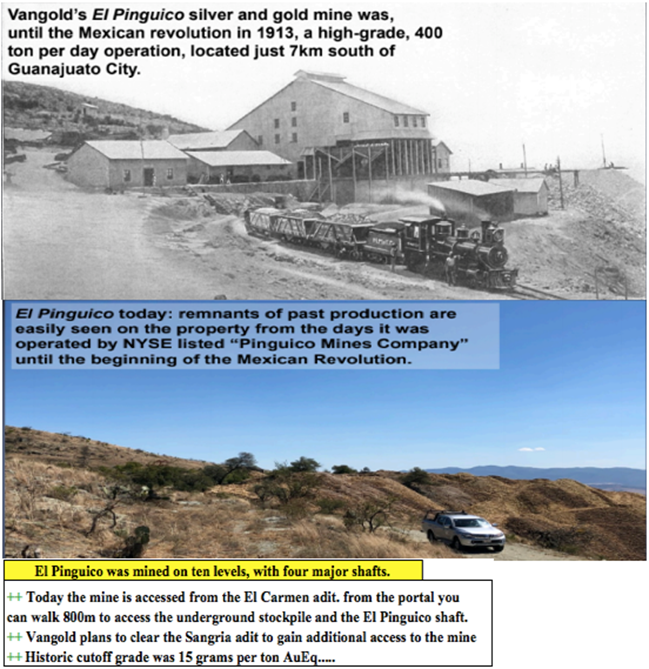

The company’s flagship property hosts the high-grade, past-producing El Pinguico mine that was only shut down due to the Mexican Revolution in 1913 (it wasn’t mined out). The mine operated on ten levels with four major shafts. From the early 1890s until 1913, El Pinguico was one of the highest grade mines in Guanajuato.

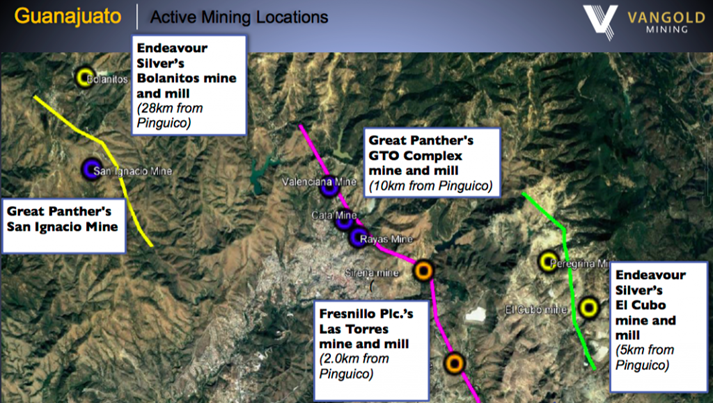

The cut-off grade was reportedly 15 g/t (0.48 oz./t) gold equivalent. Mining was done exclusively at the El Pinguico and El Carmen vein systems, which are thought to be splays off of the Mother Vein. El Pinguico is surrounded by well-known players, including Fresnillo PLC, Endeavour Silver, Great Panther and Argonaut Gold.

Modest near-term cash flow is possible from exploiting a surface stockpile this year, but more meaningful profit potential exists from extracting (and getting toll-milled) meaningful underground stockpiles grading ~3.6 g/t Au eq in 2012, the Mexican Geological Society estimated there were ~174,500 tonnes of material stockpiled underground. Assuming an 85% recovery, that equates to about a 20,000-ounce Au eq opportunity.

The plan is to reinvest net cash flow into new exploration and development activities at El Pinguico. It’s critical for readers to understand that Vangold has substantial exploration upside above and beyond monetization of stockpiles. Interestingly, the company stands to benefit from at least three things due to the global pandemic.

First, significantly lower energy costs, second, a favorable move in FX rates (weaker CAD$ and Mexican peso vs. the US$), and third, lower project costs (drilling, mining equipment and services, labor) as people will, presumably, be anxious to get back to work. Globally, unemployment rates are likely to remain elevated for an extended period.

Vangold has a substantial database of valuable exploration data including historical underground channel sampling and drilling. Samples from around the year 1909 include blockbuster grades. The best were; 0.7m @ 23.0 g/t Au + 3,858 g/t Ag, {~61.6 g/t Au Eq.}, another one of 0.8m @ 16.7 g/t Au + 3,054 g/t Ag, {~47.2 g/t Au eq}, and a third, 0.7m @ 15.7 g/t Au + 1,793 g/t Ag, {~33.6 g/t Au eq}.

As mentioned, prior mining at El Pinguico was from two vein systems (El Pinguico and El Carmen) thought to be offshoots of the Veta Madre (“Mother Vein”). The Veta Madre has been, and continues to be, incredibly important to the region. It stretches at least 25 km and has reportedly produced upwards of 1.2 billion ounces of silver.

From Endeavour’s website, “Silver was originally discovered by Spanish explorers in 1548 and subsequently at Guanajuato in 1552. Guanajuato is considered one of the top three historic silver mining districts in Mexico, having produced an estimated 1.0 to 1.2 billion ounces silver, plus 5 to 6 million ounces gold.”

The Veta Madre is also highly prospective for Vangold as it is known to extend to within 250 meters of the company’s border. Management believes it likely crosses through their property at between 400 and 600 meters depth. Importantly, Vangold is not the only company chasing the Mother Vein.

With a much higher gold price, silver not so much (yet), especially in Mexican peso terms, the region has become one of the hotter mining jurisdictions in North America. C$10 billion Fresnillo PLC is reopening a prolific (1970’s to 2002) mine that will bring additional workers, equipment and mining services to the area. The mine reopening is happening next year, just 2 km from Vangold’s project.

In addition to director Daniel Oliver, Vangold has a tremendous team for a company with a market cap of just C$2.7 million. Led by the highly experienced and well-connected James Anderson, who’s been working hard for the past year to revitalize this story, the company’s ship may have just come in. And, I should add, a rising (gold-silver) tide lifts all boats!

Readers should strongly consider taking a few minutes to review Vangold Mining’s (TSX-V: VGLD) / (OTCQB: VGLDF) brand new corporate presentation. Please visit the last two pages which extoll the considerable talents and experience of the management team.

Peter Epstein is the founder of Epstein Research. His background is in company and financial analysis. He holds an MBA degree in financial analysis from New York University’s Stern School of Business.

Disclosures / disclaimers: The content of this article is for information only. Readers fully understand and agree that nothing contained herein, written by Peter Epstein of Epstein Research [ER], (together, [ER]) about Vangold Mining, including but not limited to, commentary, opinions, views, assumptions, reported facts, calculations, etc. is to be considered implicit or explicit investment advice. Nothing contained herein is a recommendation or solicitation to buy or sell any security. [ER] is not responsible for investment actions taken by the reader. [ER] has never been, and is not currently, a registered or licensed financial advisor or broker/dealer, investment advisor, stockbroker, trader, money manager, compliance or legal officer, and does not perform market making activities. [ER] is not directly employed by any company, group, organization, party or person. The shares of Vangold Mining are highly speculative, not suitable for all investors. Readers understand and agree that investments in small cap stocks can result in a 100% loss of invested funds. It is assumed and agreed upon by readers that they will consult with their own licensed or registered financial advisors before making any investment decisions.

At the time this article was posted, Peter Epstein owned stock and warrants in Vangold Mining, and the Company was an advertiser on [ER].

While the author believes he’s diligent in screening out companies that, for any reasons whatsoever, are unattractive investment opportunities, he cannot guarantee that his efforts will (or have been) successful. [ER] is not responsible for any perceived, or actual, errors including, but not limited to, commentary, opinions, views, assumptions, reported facts & financial calculations, or for the completeness of this article or future content. [ER] is not expected or required to subsequently follow or cover any specific events or news, or write about any particular company or topic. [ER] is not an expert in any company, industry sector or investment topic.

Streetwise Reports Disclosure: 1) Peter Epstein’s disclosures are listed above. 2) The following companies mentioned in the article are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. 3) Statements and opinions expressed are the opinions of the author and not of Streetwise Reports or its officers. The author is wholly responsible for the validity of the statements. The author was not paid by Streetwise Reports for this article. Streetwise Reports was not paid by the author to publish or syndicate this article. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy.

4) The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases.

Shares of West Pharmaceutical Services traded higher and established a new 52-week high price after the firm reported Q1/20 earnings that included a 10.8% increase in YoY revenues.

Global healthcare packaging components manufacturer company West Pharmaceutical Services Inc. (WST:NYSE) today announced financial results for its first quarter ending March 31, 2020 and provided updated full-year 2020 financial guidance.

The company reported that net sales in Q1/20 increased to $491.5 million, a 10.8% increase from $443.5 million in Q1/19. During the same corresponding period, the firm stated that non-GAAP diluted earnings per share (EPS) increased by 36% to $0.99 and non-GAAP adjusted-diluted EPS increased by 36% to $1.01.

West Pharmaceutical Services advised that it is maintaining its FY/20 net sales guidance, which is expected to be in a range of $1.95-1.97 billion. The company stated that it is updating FY/20 adjusted-diluted EPS guidance to a new range of $3.52-3.62, compared to the prior estimated range of $3.45-3.55.

The company’s President and CEO Eric M. Green commented, “During these unprecedented times, our priorities are focused on the well-being and safety of our team members as well as ensuring the supply of critical, high-quality components and solutions to our customers…I am extremely pleased that we delivered a strong performance in the first quarter given the challenging environment that the COVID-19 pandemic has had on our customers, our suppliers and our team members. In particular, we continued to deliver strong sales growth in high-value products, as demand trends from our worldwide customer base were similar to trends we saw last year. Our teams are partnering with a broad range of customers working to support efforts to develop solutions that address the global COVID-19 pandemic such as diagnostics, anti-viral therapeutics and vaccines.”

The firm outlined sales in the most recent quarter by product line. The company reported that in Q1/20, net sales in its Proprietary Products segment grew by 9.7% to $373.5 million and that this segment “saw good demand for Westar®, Daikyo®, NovaPure® and FluroTec® components as well as for devices such as Daikyo Crystal Zenith® syringes and cartridges and our self-injection platforms.”

The firm noted that net sales from its Contract-Manufactured Products segment grew by 14.5% to $118.1 million led by sales of components for diagnostic devices and drug-injection delivery devices.

The company added that the Biologics market unit enjoyed double-digit organic sales growth, the Generics market unit achieved high-single digit organic sales growth and the Pharma market unit registered mid-single digit organic sales growth.

The firm additionally noted that during Q1/20 under its share repurchase program, it repurchased 761,500 shares for $115.5 million at an average share price of $151.65.

West Pharmaceutical Services is headquartered in Exton, Pa., roughly 35 miles west of Philadelphia, and is a designer and manufacturer of injectable pharmaceutical packaging and delivery systems.

West Pharmaceutical has market capitalization of around $13.5 billion with approximately 73.84 million shares outstanding. WST shares opened 5.25% higher today at $179.05 (+$8.93, +5.25%) over yesterday’s $170.12 closing price and reached a new 52-week high price this morning of $190.27. The stock has traded today between $177.13 and $190.27 per share and is currently trading at $187.04 (+$17.17, +10.11%).

Disclosure: 1) Stephen Hytha compiled this article for Streetwise Reports LLC and provides services to Streetwise Reports as an independent contractor. He or members of his household own securities of the following companies mentioned in the article: None. He or members of his household are paid by the following companies mentioned in this article: None. 2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. 3) Comments and opinions expressed are those of the specific experts and not of Streetwise Reports or its officers. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. 4) The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases. 6) This article does not constitute medical advice. Officers, employees and contributors to Streetwise Reports are not licensed medical professionals. Readers should always contact their healthcare professionals for medical advice.

Bob Moriarty of 321gold discusses recent developments at three junior mining companies that have done deals with majors.

I’ve been pretty quiet about mining shares lately as I try to get a handle on what the real story is on the Corona Virus. That doesn’t mean the companies have been quiet and indeed they have not been. The Corona Virus story looks more and more like a scam on the part of big Pharma with each passing day so I will be doing more writing on it.

Three of our advertisers have done deals lately with majors and are showing the next trend in the junior market. Behind the scenes, the majors and mid-tier mining companies are beginning to realize that they need to be doing deals with the best and brightest of the juniors right now.

The efforts of the US government to bail out a totally insolvent financial system just put gold and silver into what will be the ultimate afterburner. I would be perfectly happy with a correction soon to clean out some of the deadwood that like to buy at tops but down the road, the dollar, the bond market and the stock market are toast.

What else is left to invest in?

The CRB Commodity Index has crashed by 75% from its peak in 2008. It is at the lowest level since 1972. Yes, we are in a depression and prices have plummeted but we still need commodities. Everything is cheap.

The long oil positions crashing this week to minus $37 a barrel show just how dysfunctional our financial system is right now. I don’t know when gold and silver will kick into high gear, it isn’t here yet.

But could we see gold up $200 in a day and silver up $10? Yes and I think we will. The door to investing into resource shares is a little tiny door. When everyone wants to go through at the same time, it’s going to get pretty crowded.

They also eat a lot of money. Newcrest put about $5 million into Rattlesnake and drilled a deep hole that hit a lot of rock. Even very big, very well run companies like Newcrest hit dusters on a regular basis. Did I mention that alkaline systems tend to be very big and very rich? And eat a lot of money.

I can’t fault Newcrest. I do still think they are one of the finest mining companies in the world. Their geos had a theory. They poured a lot of money into the ground and hit SFA.

I’ll be really charitable and say that I think the really negative press release and the really positive press release came out at about the same time by coincidence because when I start thinking that companies are massaging their stock price in the face of bad news I get really snarky. If it was a coincidence I would like to see it be a solo coincidence.

When I wrote about GFG a long time back, I said that having a Plan B was a great idea. Because if one project doesn’t pan out, you have a backup. The Eastern Canada operations have turned out to be brilliant and will more than support the value of the company regardless of what happens to Rattlesnake.

Rattlesnake is still a high potential project. There have been a lot of good hits there and the feeders are there somewhere. Gold going up makes the odds of failure go down so Rattlesnake is still a great project for GFG. Someone will want to do a deal. Geos have more theories than Starbucks has flavors of coffee.

But meanwhile on the strength of the PEN monster hit, Alamos Gold Inc. (AGI:TSX; AGI:NYSE) has stepped up to the plate to inject enough money into a non-brokered PP to bring them up to 9.9%. It will be about $5 million in flow-through shares at $0.291 and non-flow through shares at $0.19. Not only is Alamos putting money into the company at a premium, there are zero warrants.

Darn, I want in the PP as well and I love warrants.

I’ve written about TriStar Gold Inc. (TSG:TSX.V) before. They have a conglomerate gold system in Brazil. Quinton Hennigh, Erik Wetterling of the Hedgeless Horseman and I snuck in a visit to Brazil in February just before the Iron Curtain came down all over the world.

It was a really great visit. TriStar has a smoothly functioning team with very nice and highly qualified geos. And some are quite attractive.

Erik gives Fernanda panning lessons at TriStar

Quinton gave a 30-minute brief talking about how they have three different styles of gold in three different horizons. I though I understood conglomerate gold systems before but he made it very simple.

He and I made a ten-day scouting trip to New Zealand in 2009 before going to Perth to meet with Mark Creasy on the deal that became Novo Resources. In any case, we actually visited a beach on the west coast of the South Island of New Zealand. Under certain wind and tide conditions, the beach would become covered with a thin layer of gold brought in from the sea floor just off shore. I had seen gold in sand but didn’t understand it in context until Quinton spoke in Brazil.

Quinton’s lecture

Different layers of conglomerate

Conglomerate

TriStar Gold is yet another junior that has a major betting on their success. In August of last year TriStar announced an $8 million deal with Royal Gold where Royal put in money in different tranches and got some warrants as well. Royal was buying a 1.5% NSR on production. Nobody bets $8 million on production unless they have a high degree of confidence that the company will actually get into production.

Not to be outdone, Precipitate Gold just announced a funding deal with Barrick Gold. Barrick is willing to pay up to $10 million in exploration on Precipitate’s Pueblo Grande project and conduct a pre-feasibility study to earn 70% of the property. In addition Barrick will invest $1.39 million CAD into Precipitate shares at $0.11.

I went to see the Pueblo Grande project about ten years ago. It is belly to belly with Barrick’s Pueblo Viejo Gold Mine. That was in construction when I was there and now in production at a rate of nearly 600,000 ounces for Barrick with right at 1 million ounces a year total. Pueblo Viejo is owned 60% by Barrick and 40% by Newmont. As a tax source, the mine is the most important industry in the Dominican Republic. It is also the largest gold mine in the Americas.

I like to keep investing simple. Barrick knows what they are producing per year. They know the grade and the cost. They also fully understand the geology. By buying the right to own 70% of Pueblo Grande from Precipitate, they know exactly what they are getting and what the cost is and what the value is.

I love reading the chat boards because the vast majority of posters all believe they know better than the companies as to what they should do. Most posters know in their hearts that they could do a much better job of running the company. That’s daft of course and I rarely come across deep or really thoughtful discussion. But if the biggest mining company in the country wants to put money into your project, the project is probably worth having. It’s not a bit more complicated than that.

If Barrick funds $10 million in exploration they will find gold. They have the mill right next door so the only cost of production for Precipitate is paying 30% of hauling the gold to the mill. I’m not quite sure how the math works; Barrick would own 70% of Pueblo Grande but only 60% of the mill at Pueblo Viejo. Newmont is a part owner and they will have to be compensated for use of the mill.

Precipitate still has other projects and now will be fully funded to do exploration on them.

I own shares in all three companies both bought in the open market and participation in private placements. All three companies are advertisers so naturally I am biased. Do your own due diligence.

Bob Moriarty founded 321gold.com, with his late wife, Barbara Moriarty, more than 16 years ago. They later added 321energy.com to cover oil, natural gas, gasoline, coal, solar, wind and nuclear energy. Both sites feature articles, editorial opinions, pricing figures and updates on current events affecting both sectors. Previously, Moriarty was a Marine F-4B and O-1 pilot with more than 832 missions in Vietnam. He holds 14 international aviation records.

Disclosure: 1) Bob Moriarty: I, or members of my immediate household or family, own shares of the following companies mentioned in this article: GFG Resources, TriStar Gold and Precipitate Gold. My company has a financial relationship with the following companies mentioned in this article: GFG Resources, TriStar Gold and Precipitate Gold are advertisers on 321 Gold. I determined which companies would be included in this article based on my research and understanding of the sector. 2) The following companies mentioned are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. 3) Statements and opinions expressed are the opinions of the author and not of Streetwise Reports or its officers. The author is wholly responsible for the validity of the statements. The author was not paid by Streetwise Reports for this article. Streetwise Reports was not paid by the author to publish or syndicate this article. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy. 4) The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases. As of the date of this article, officers and/or employees of Streetwise Reports LLC (including members of their household) own securities of GFG Resources, Royal Gold and Newmont Goldcorp, companies mentioned in this article.

Falling credit card spending in New Zealand bearish for NZDUSD

New Zealand’s consumers cut credit spending in March: credit card spending fell 8.2% over year after 2.2% growth in February. This indicates deteriorating consumers’ confidence in financial prospects. This is bearish for NZDUSD.