At the H4 chart, the USD/CAD pair continues growing and forming the ascending channel with Long-Legged Doji, Hammer, Doji, Harami, and Engulfing reversal patterns at support and resistance levels to define its borders. Right now, after finishing another correction, the pair is trading close to the resistance level and may grow to reach 1.2455.

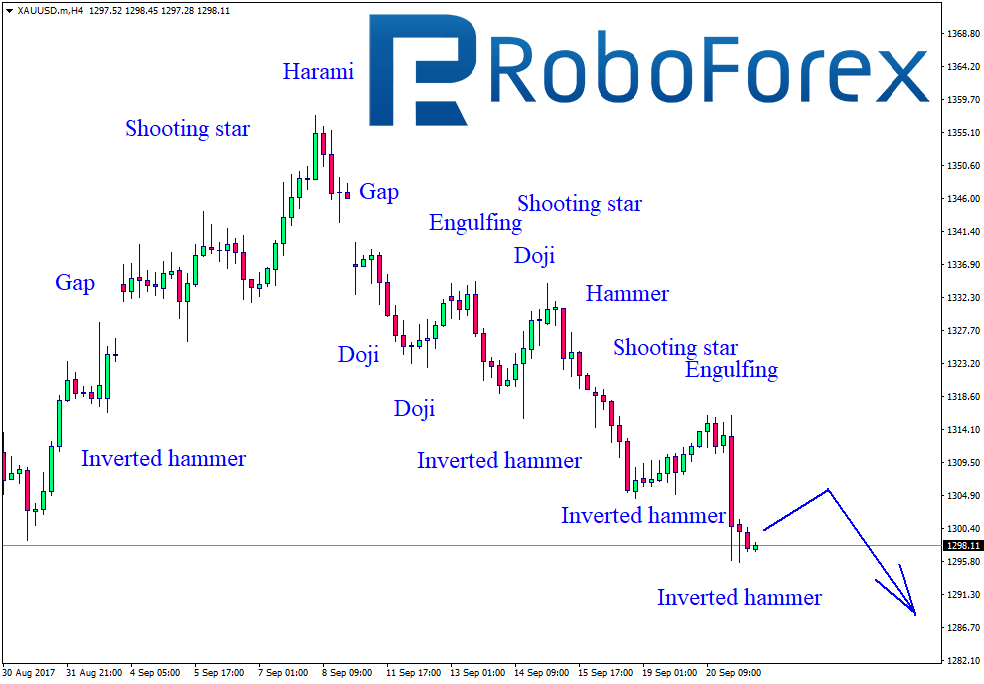

XAU USD, “Gold vs US Dollar”

As we can see at the H4 chart, the instrument continues forming the descending channel with Gap, Engulfing, Shooting Star, Doji, Hammer, and Inverted Hammer patterns to define its borders. After completing another correction, the price formed Engulfing patterns and returned to the support level. Yesterday, the pair failed to reach 1290.50 and by now it has finished Inverted Hammer pattern, which may indicate another correction towards the resistance level at 1313.00.

Attention! Forecasts presented in this section only reflect the author’s private opinion and should not be considered as guidance for trading. RoboForex LP bears no responsibility for trading results based on trading recommendations described in these analytical reviews.

EUR/USD: Fed did not deliver anything decisively hawkish, USD rally could be temporary

Macroeconomic overview: The Fed left its target interest rate unchanged, but announced that it will begin to gradually shrink its balance sheet in October. The monthly pace of the reduction will initially be USD 10bn and increase to USD 50bn in the course of next year. The updated Summary of Economic Projections did not contain any meaningful changes compared to June. The Fed officials continue to see one additional rate hike this year, followed by another three increases in 2018. The Committee did, however, further lower its estimate for the longer-run equilibrium rate.

We admit that we were surprised by yesterday’s reversal in USD and the drop of EUR/USD below 1.1900. We could not find anything decisively hawkish (relative to expectations) that could justify the dollar rally. In all likelihood some market participants may have been expecting a more cautious stance that did not materialize and responded by bidding the greenback higher as the probability of a rate hike in December has now risen. This may induce more two-way volatility in the FX market but does not change our fundamental stance. We still think EUR-USD corrections will remain contained and the area around 1.1850 should prove to be a strong support zone. We see no reason to change our constructive stance as nothing has changed in terms of relative fundamentals.

Technical analysis: The EUR/USD fall was stopped at 23.6% fibo of the 1.1119 to 1.2092 rise. This level was pierced on September 14, but there was no close below. The fact that the pair did not manage to break below that fibo yesterday may suggest that the bears are not strong enough to reverse the upward trend.

Short-term signal: Stay long for 1.2250.

Long-term outlook: Bullish

USD/JPY: BoJ keeps policy unchanged, new board member dissents

Macroeconomic overview: The Bank of Japan kept monetary settings steady on Thursday, but a board newcomer argued against the central bank’s view that current policy was sufficient to boost inflation to its 2% target in a sobering assessment of the outlook.

Goushi Kataoka, a vocal advocate of aggressive easing who joined the board in late July, dissented in an 8-1 vote – potentially exposing a fresh rift in the board that could further delay any plan by the BOJ to dial back its massive stimulus.

The BOJ decided to keep its short-term interest rate target at minus 0.1% and a pledge to guide 10-year government bond yields around zero percent under its yield curve control policy.

The BOJ also maintained a loose pledge to keep buying bonds so its holdings increase at an annual pace of 80 trillion JPY, diverting from the U.S. Federal Reserve’s plan to steadily pull back from crisis-era measures.

The announcement came hours after the Fed’s decision to leave interest rate unchanged and a signal it still expects one more increase by the end of the year, which pushed the dollar to a two-month high against the yen.

BoJ governor Haruhiko Kuroda commented on the diverging paths of Fed, ECB and BOJ: “Japan’s economy is recovering, as is the case of Europe and the United States. But in Japan, inflation expectations aren’t anchored around the BOJ’s price target … U.S. and European inflation expectations are anchored around their central banks’ price targets.”

Short-term signal: We opened USD/JPY short at 112.15 for 110.00. The stop-loss is at 113.20. The position is quite risky, so we recommend lower position size.

Long-term outlook: Flat

NZD/USD: 7-day ema remains a solid support for rising trend

Macroeconomic overview: New Zealand’s GDP jumped 0.8% in the three months to the end of June, up from a revised 0.6% the previous quarter. Annual GDP was left unchanged at 2.5%.

Services were the bright spot behind faster quarterly growth in the second quarter, as all service industries combined expanded 1.0% after growing 0.5% in the first quarter. Three service categories improved markedly in the second quarter, with retail trade and accommodation expanding 2.8% (vs. 2.0% in the first quarter); transport, postal and warehousing 3.5% (vs. -1.6%); and professional scientific, technical, admin and support 1.1% (vs. no change in the first quarter).

Thursday’s outcome is unlikely to divert the Reserve Bank of New Zealand from its firm path of keeping rates on hold at record lows of 1.75% for years to stoke inflation.

Despite accelerating economic growth, the NZD slipped against a broadly firmer USD today. We think that USD strength is temporary, because Fed’s monetary tightening had been widely expected and already priced in. In our opinion the strategy should be to use NZD/USD dips to buy the kiwi.

Technical analysis: The NZD/USD broke above 23.6% fibo of May-July rally yesterday, that is a resistance level now. But the pair did not manage to close above the above-mentioned resistance. Today the NZD/USD fell back to 7-day exponential moving average and stays above it. The short-term moving averages are positively aligned, which keeps bullish trend intact. We think the reaction to Fed’s statement would be short-lived and we stay bullish on the NZD/USD.

The EUR/USD pair has broken 1.1980 and is still falling inside the third wave towards 1.1855. We think, today the price may reach the predicted target at 1.1855. After that, the instrument may grow towards 1.1928 and then fall to reach 1.1830. the target of the third wave is at 1.1670.

GBP USD, “Great Britain Pound vs US Dollar”

The GBP/USD pair has finished the descending impulse along with the correction. Possibly, today the price may break 1.3444 to the downside. The target of the descending wave is at 1.3222.

USD CHF, “US Dollar vs Swiss Franc”

The USD/CHF pair has broken the range to the upside and right now is forming the third ascending structure towards 0.9817. After that, the instrument may be corrected to reach 0.9700 and then continue growing with the predicted target at 0.9841.

USD JPY, “US Dollar vs Japanese Yen”

Being under pressure, the USD/JPY pair is moving upwards. Possibly, the price may reach 112.90. Later, in our opinion, the market may continue falling with the target at 111.23.

AUD USD, “Australian Dollar vs US Dollar”

The AUD/USD pair is forming another descending wave. We think, today the price may reach 0.7982. After that, the instrument may grow towards 0.8040 and then fall with the target at 0.7929.

USD RUB, “US Dollar vs Russian Ruble”

The USD/RUB pair has broken the ascending channel to the downside and right now is trading to reach 57.48. Later, in our opinion, the market may grow towards 57.84 and then resume falling with the target at 56.55.

XAU USD, “Gold vs US Dollar”

Gold has rebounded from 1315 and started trading to the downside. The next target is at 1294. After that, the instrument may return to 1315 and then resume falling towards 1284.

BRENT

Brent has broken its consolidation range to the upside and may continue growing towards 56.22, which is considered as the main level for the entire wave. Later, in our opinion, the market may break it to the downside and start another consolidation range to reach 51.00.

Attention! Forecasts presented in this section only reflect the author’s private opinion and should not be considered as guidance for trading. RoboForex LP bears no responsibility for trading results based on trading recommendations described in these analytical reviews.

Yesterday, the US Federal Reserve softened its rhetoric with regards to monetary policy. The regulator left the key rate unchanged at 1.00% – 1.25%, although it did lower its long-term “neutral” interest rate from 3.0% to 2.8%. This was made known in the FOMC’s advance release of their economic projections, published on the Fed’s website yesterday, the 20th of September, at 21:00 (GMT+3):

Here, we can see that the Fed has downgraded its forecast for the “longer run” from 3.0% in June to 2.8% now. The “central tendency” ranges for 2018 and 2019 have also been downgraded, which could potentially slow down the trajectory of the rate hike cycle. The Fed also announced that they would start the process of normalising their balance sheet in October. The parameters of this process are outlined on the New York Fed’s webpage. At the FOMC press conference, Janet Yellen stressed that if the economic situation starts to worsen, the Fed is ready to halt the balance sheet reduction and even, if necessary, lower interest rates.

In my opinion, the reduction in the neutral rate projection and the potential trajectory of the cycle of interest rate hikes is a clear signal that the Fed is looking to raise rates more gradually, which should have a positive influence on the US economy and provide support to the US dollar as a result. After yesterday’s loosening of monetary policy, I reckon that this has opened the way for the dollar to recover some of its losses against the euro, pound, franc, yen, and gold in October and November.

I’ll be considering a long position on USDCHF and a short position on gold. At the time of writing, the USDCHF pair is trading at 0.9717, while XAUUSD is at 1,298.90 USD.

As the US policy has failed in the Korean Peninsula, dark scenarios cast a shadow over the region – but could also pave way for peace.

Recently, US President Donald Trump, in a historically bellicose debut speech to the UN General Assembly, threatened the “total destruction” of North Korea if it does not abandon its drive toward nuclear weapons.

“Rocket man is on a suicide mission for himself and his regime,” Trump said about the North Korean leader. He added: “If [the United States] is forced to defend itself or its allies, we will have no choice but to totally destroy North Korea.”

The menacing threats reverberated across Asia. If Trump truly threatens to resort to conventional weapons or a limited nuclear strike to annihilate more than 25 million North Koreans, he is endangering the lives of millions of South Koreans and Chinese. Pyongyang is more than 11,000 kilometers away from Washington DC but only 200 kilometers from Seoul and 800 kilometers from Beijing – not that different from Washington DC to Atlantic City or Atlanta, respectively.

President Donald Trump and his Chinese counterpart President Xi Jinping have jointly denounced North Korea’s recent nuclear test as “dangerous to the world.”

Recently, U.S. UN Ambassador Nikki Haley called for “the strongest sanctions” to pressure North Korea into giving up its nuclear arsenal “before it’s too late.” Now President Trump’s rhetoric is taking the conflict with North Korea to an entirely new level – assuming that the White House will walk the talk.

And yet, in a sense, it is already too late. Decades of U.S. policies have strengthened Pyongyang’s determination to exploit the deterrent value of its nuclear arsenals – as evidenced by its intermediate range ballistic missile on September 15; the second time that Japan has come in North Korean missile’s targeting range within a month.

That is not to say that the game is over; only that it is time to play a different game. Dealing with the “Rocket man” is not rocket science.

Decades of policy failures

Ever since the 1953 Armistice Agreement, Washington has seen North Korea as a “rogue state.” Even with the Soviet Union, Washington supported “peaceful coexistence”; with North Korea, only a “temporary ceasefire” – which has nurtured fears of imminent intrusion in Pyongyang.

In the postwar era, both China and North Korea opted for socialism. But when Deng Xiaoping opted for economic reforms and opening-up policies, Kim Il-sung (1972-94) chose precisely the reverse; a self-reliance (Juche) doctrine that translated to political consolidation and international insulation.

When Kim Jong-il (1997-2011) succeeded his father, he chose not to reform the economy and kept the country closed. While the West celebrated the “end of history,” Pyongyang was obsessed with the U.S.-led “big bang democracy” in Russia and the consequent Great Depression. It served as a compelling negative demonstration effect.

For years, Beijinghad encouraged Pyongyang to emulate Chinese lessons in economic reforms. Kim Jong-il listened, but initiated few reforms. Kim Jong-un (2012-) is a different story. In a televised 2013 New Year’s address, he advocated “a radical turn in the building of an economic giant on the strength of science and technology by fanning the flames of the industrial revolution in the new century.” These economic efforts should “be manifested in the people’s standard of living.” In the Obama White House, it was seen as just another ploy.

Instead of rapprochement, Washington pushed for a Terminal High Altitude Area Defense (THAAD) anti-ballistic missile system in South Korea. THAAD would kill two birds with one stone: it would subdue Pyongyang and it would contain China. The stance was predicated on President Park (who would soon be impeached), a “realistic” Kim Jong-il (who has not given in), accommodating Beijing (not President Xi Jinping’s firm leadership) – and an imperial White House that would “speak softly but carry a big stick” (until the failure of the Clinton campaign).

In a year, all these assumptions collapsed. In the Korean Peninsula, the new status quo offers potentially disastrous scenarios but also a way out.

South Korea’s strategic U-turn

As Seoul is trying to cope with North Korea’s nuclear blackmail, it is amid a great domestic shift. In March, Park Geun-hye, the conservative daughter of South Korea’s former strongman Park Chung-hee was impeached for corruption. In turn, Moon Jae-in, the incumbent president began his career as student activist against Park’s dictatorship and his presidency could result in a new geopolitical momentum for peace. He worked closely with President Roh Moo-hyun (2003-8), who pursued rapprochement with North Korea.

In his first months, President Moon has been promoting income-led domestic policies to reduce social inequality, tax hikes for large companies and the wealthy and trying to cool the overheated property market. While public debt has expanded, his approval ratings remain very high at around 80 percent.

In foreign relations, Moon seeks stability with China and the U.S., even if he and most Koreans have great doubts about Trump. In fall 2013, South Korea approached the Pentagon about the anti-missile system, which it opted for toward the end of the Park era. Obviously, Beijing’s concern is that the real target of the THAAD is China. Moon has sought to slow THAAD’s deployment.

But the balancing act between Washington and Beijing is challenging, especially as Trump insists on renegotiating a bilateral free trade agreement with Korea, which remains on watchlist for “unfair currency practices.”

Moreover, President Park’s conservatives were able to postpone the repeal of the Operation Control agreement (OPCON), which allows the Pentagon – not Seoul – to control its military fate. The mission statement of the South Korea/US Combined Forces Command (CFC) is to “deter hostile acts of external aggression” South Korea by a “combined military effort.” The CFC is commanded by a U.S. General and it has has operational control (OPCON) over more than 600,000 active duty military personnel both countries.

As President Rho failed to implement transfer, the latter was delayed; in turn, President Park managed to defer it to 2022. In the event of war, U.S. interests will thus override the interests of South Koreans – in their own country.

Washington’s ominous tone

The talks over North Korea’s nuclear weapons have been lingering since they were initiated by the Clinton Administration in the 1990s. After the George W. Bush presidency and the first term of the Obama Administration, the negotiations shifted from mainly bilateral to the multilateral Six-Party Talks among the US, China, South and North Korea, Japan and Russia.

The expansion reflected progressive shifts in the world economy. Just as the G7 nations – the US, Europe and Japan – could not resolve the global crisis without support by large emerging economies, regional conflicts that have global implications cannot be resolved by the “West” anymore. In the Six-Party Talks, some key agreements were reached for North Korea’s aid and recognition in exchange for denuclearization. But since 2009, the talks have been suspended, while concern about nuclear proliferation to other strategic actors has increased.

Following false starts in talks and aborted policy postures, the White House has opted for new sanctions and building alliances against Pyongyang. Meanwhile, President Trump and Pyongyang have engaged in the kind of rhetoric that has not been heard since the Cuban Missile Crisis. Recently, President Vladimir Putin stated that the U.S. strategy under Trump, Obama, Bush – forcing North Korea to give up its nuclear program – has conclusively failed.

Since Pyongyang believes that its nuclear arsenal is the best deterrent against U.S. invasion, which President Trump’s “fire and fury” threats have only reaffirmed, it is now less likely to reconsider its nuclear stance.

From Pyongyang’s perspective, U.S. threat is existential, extending from regime plans that would top the Kim Jong-un leadership to a limited nuclear strike that threatens the entire nation – as precipitated by the THAAD system.

From Pyongyang’s perspective, U.S. threat is existential, extending from regime plans that would top the Kim Jong-un leadership to a limited nuclear strike that threatens the entire nation – as precipitated by the THAAD system. Undeniably, the timeline of North Korea’s intensified nuclear and missile tests correlates with efforts to sustain THAAD and joint US-South Korean war games in the region.

On September 17, the Pentagon’s 14 bombers and fighters over the Korean Peninsula – which included South Korean and Japanese aircraft and a drop of live bombs in a massive show of force – merely confirmed the severity of existential threat among North Koreans.

Chinese unease

While Washington has never had diplomatic relations with Pyongyang, China has been North Korea’s close, though increasingly ambivalent ally. The conditions that once gave rise to the partnership have progressively diminished. Nevertheless, both Koreas are located in close proximity to the mainland, which remains vital to Beijing.

In Washington, Beijing’s role is regarded as invaluable to contain Pyongyang’s nuclear weapons and ballistic missiles, to prevent nuclear proliferation, to enforce economic sanctions, and to support North Korean refugees that cross into China. But Beijing does not see itself as the enforcer of U.S. foreign policy, particularly one that’s considered misguided.

Moreover, Beijing opposes Trump’s attempt to couple sanctions against North Korea with sanctions against Chinese companies and against North Korean people. If Trump persists in the current approach, he will risk alienating China.

Washington’s stated interest is denuclearization and human rights, but in Beijing’s view U.S. actions have escalated nuclearization and weakened human rights in the region. Neither Kim Jong-un’s disruptive actions nor Trump’s aggressive rhetoric serve China’s interest in peace and stability in the region.

On September 3, after North Korea claimed that it has successfully tested a hydrogen bomb designed to fit into an intercontinental ballistic missile (ICBM), the U.S. Geological Service and the China Earthquake Administration recorded a 6.3 magnitude earthquake as a result of the detonation. It was followed by a 4.1 magnitude quake, due to a suspected cave collapse resulting from the explosion. Chinese scientists warn that North Korea’s nuclear test site is at risk of imploding, which has a potential for a massive environmental disaster.

Neither Chinese nor South Korean policymakers want another Fukushima and a massive humanitarian crisis within their borders.

Only one viable scenario

So what can be done and what is likely to happen next? There are a few potential scenarios, fewer probable ones – but only one that’s sustainable.

Walk the war talk. Recently, US Secretary of Defense Jim Mattis threatened North Korea with an “effective and overwhelming military response.” But in the Korean Peninsula, hostilities cannot be limited to a conventional conflict. Under threat, Pyongyang will opt for a nuclear strike, even if that would result in massive devastation. It would be a Pyrrhic victory.

Hollow rhetoric/”Total destruction” threats. If the Trump administration will continue to promise shock and awe but won’t deliver any, it will risk being perceived as a paper tiger. Moreover, as Pyongyang is likely to continue its tests and target provocative destinations vital to South Korea, Japan and the U.S., the THAAD would be perceived as an expensive but useless deterrent. Unless, of course, the administration will choose to execute Trump’s “total destruction” threat, but that would have even darker consequences across the world.

Broader sanctions. As Washington resorts to sanctions, it is now also trying to corner China by extending sanctions to Chinese companies. While China accounts for 90 percent of trade with North Korea, much of the remaining 10 percent can be attributed to India, the Philippines, Taiwan and France. If they are not included within the sanctions, the latter will be seen as containment against China. If they are included, the White House will frustrate it’s allies.

Peace agreement. While there are all kind of short-term scenarios, there is only one longer-term option. As the stakes are mounting for regional devastation, so are the chances for a peace agreement. It would be the most effective way to subdue North Korea’s nuclear stance over time. As long as it remains threatened, Pyongyang will rely on its nuclear strategy. But if that threat is defused, nuclear scenarios will be undermined.

A peace treaty would mean reduced U.S. presence in the region, which has been highly objectionable to Washington. However, despite its hawkishness, the Trump administration does not see itself as bound by previous defense arrangements. In Beijing’s view, peace agreement would pave way for pacification and stability; delimit nuclear threat in the region, while North Korea’s sovereignty would prevail.

Bilateral peace in denuclearized Korean Peninsula

In August, former U.S. President Jimmy Carter, who has negotiated with several North Korean leaders, noted that, for a long time, Pyongyang has sought a “peace treaty to replace the [1953] ceasefire.” In his experience, North Koreans want peaceful relations with the U.S. and regional neighbors but are convinced that Washington is planning a preemptive military strike against their country. In view of U.S. record of regime changes, that’s not a futile concern.

A true peace agreement would have to be a bilateral agreement with two sovereign Koreas – not one imposed by Washington, or by nuclear blackmail.

A true peace agreement would have to be a bilateral agreement with two sovereign Koreas and the acceptance of Pyongyang as a nuclear power. Since North Korea accounts for only 0.6% of global nuclear forces, that translates to affirming realities.

Figure World nuclear forces: The Role of North Korea

(% of world total by country, 2016 (SIPRI)

The old nuclear regime that prevailed in the Cold War and the post-Cold War era is history. In addition to current nuclear powers – US, Russia, India, Pakistan, China, France, UK, Israel, North Korea – proliferation is likely to increase in the multipolar era.

In the 21st century, sustained peace is not ensured by restricting nuclear capability to one, two or half a dozen nations, but by collectively- monitored certainty that nuclear proliferation will be limited for peaceful purposes only.

About the Author:

Dr. Steinbock is Guest Fellow of Shanghai Institutes for International Studies (SIIS), see http://en.siis.org.cn/ . The commentary is part of his SIIS project “China in the Era of Economic Uncertainty and Geopolitical Risk.” For his global advisory activities and other affiliations in the US and Europe, see http://www.differencegroup.net/

The original, shorter commentary was released by China-US Focus on Sept 18, 2017.

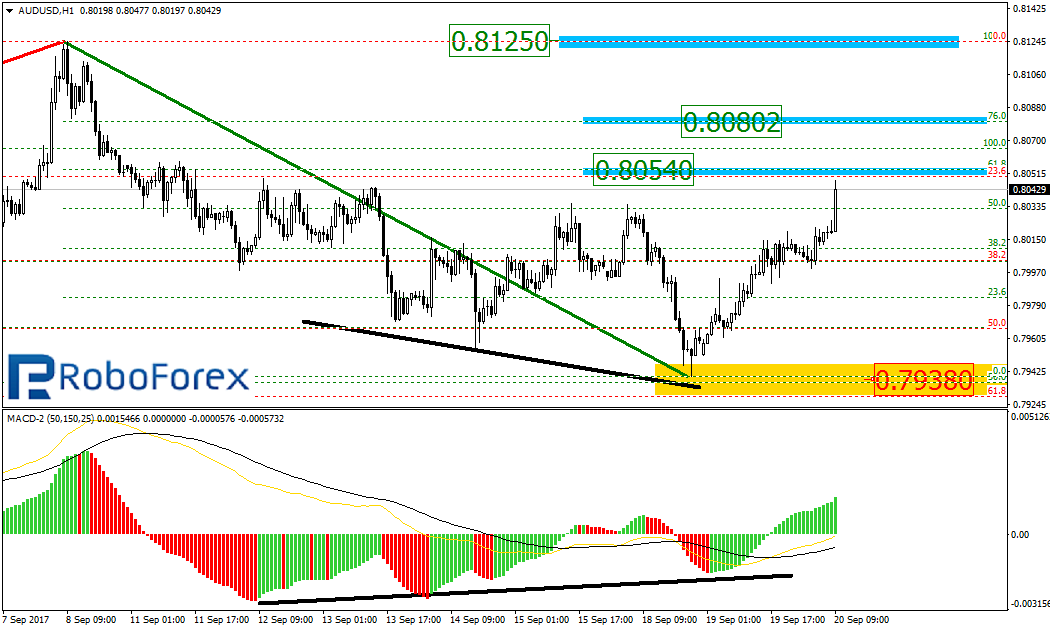

At the H4 chart, the AUD/USD pair is forming another ascending impulse. The short-term support is at 0.7938. The possible upside targets may be inside two the post-correctional extension areas between the retracements of 138.2% and 161.8%, the long term one – 0.8165 and 0.8225, the short-term one – 0.8192 and 0.8240 respectively.

At the H1 chart, the pair is forming the convergence and about to finish its descending movement. The closest targets of the current growth are close to the retracements of 61.8% and 76.0% at 0.8054 and 0.8080 respectively, and the high at 0.8125.

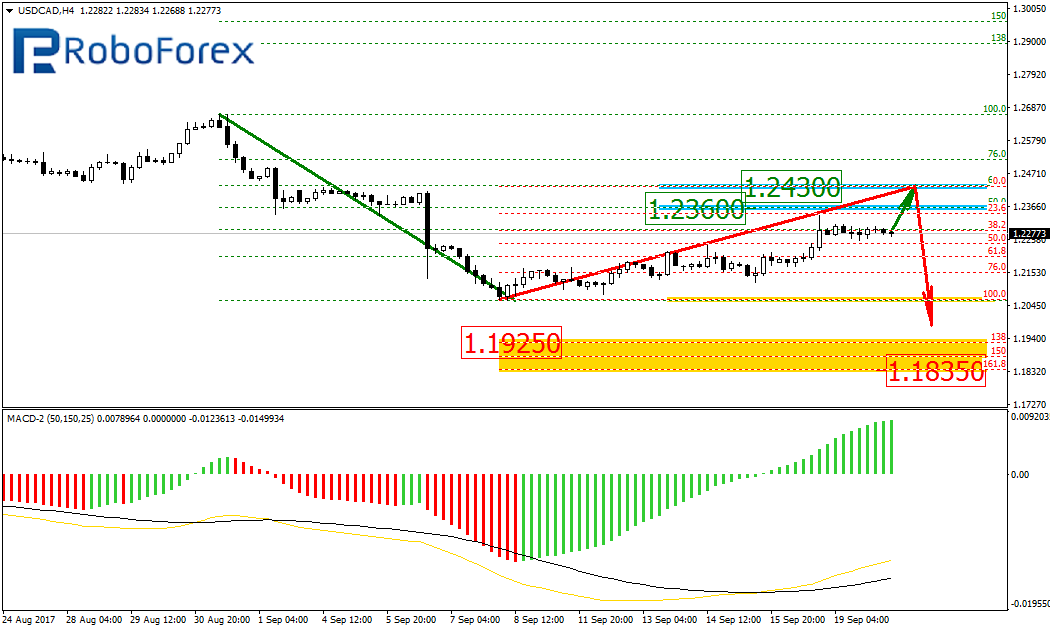

USD/CAD, “US Dollar vs Canadian Dollar”

At the H4 chart, the USD/CAD pair is being corrected to the upside. The targets of this correction may be the retracements of 50.0% and 61.8% at 1.2360 and 1.2430 respectively. After finishing the correction, the price may resume falling to test the local low. If the pair breaks it, the instrument may fall towards the post-correctional extension area between the retracements of 138.2% and 161.8% at 1.1925 and 1.1835 respectively.

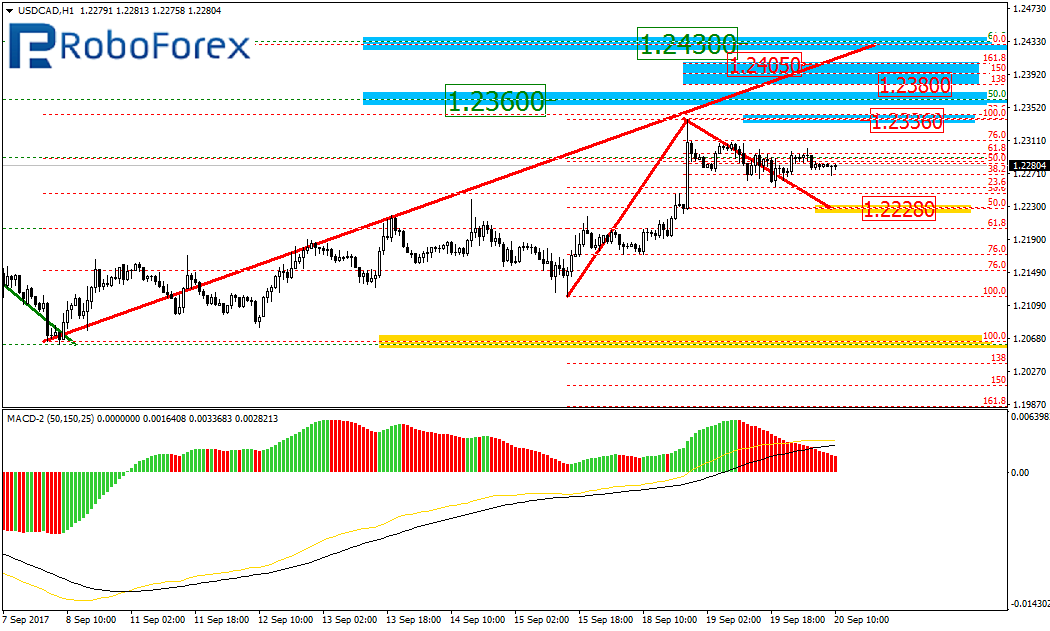

As we can see at the H1 chart, after completing the short-term ascending impulse, the pair is also being corrected to the downside. The main target of this correction may the retracement of 50.0% at 1.2228. After the correction is over, the uptrend may continue towards the area between 1.2380 and 1.2405.

Attention! Forecasts presented in this section only reflect the author’s private opinion and should not be considered as guidance for trading. RoboForex LP bears no responsibility for trading results based on trading recommendations described in these analytical reviews.

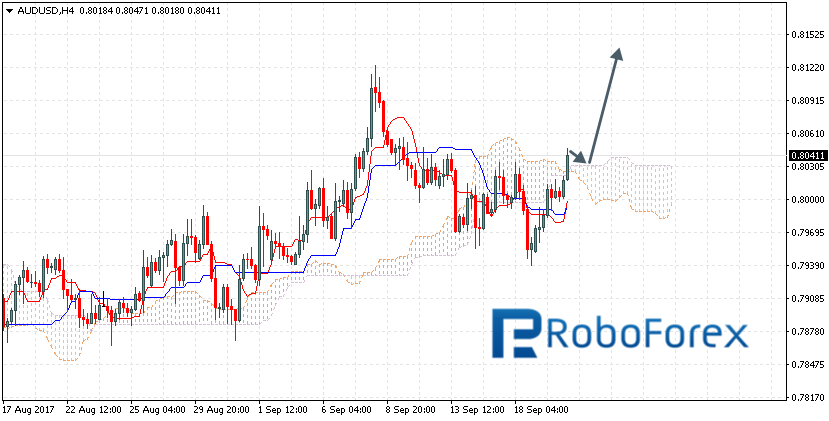

The AUD/USD pair is trading at 0.8041; the instrument is still moving above Ichimoku Cloud, which means that it may continue growing. We should expect the price to test the upside border of the cloud at 0.8030 and continue moving upwards to reach 0.8135. However, this scenario may be cancelled if the price breaks the downside border of the cloud and fixes below 0.7990. In this case, the pair may continue falling towards 0.7880.

NZD/USD, “New Zealand Dollar vs US Dollar”

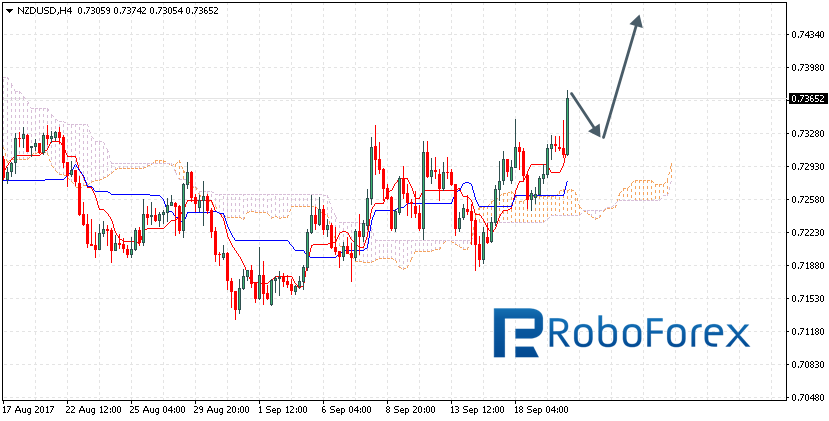

The NZD/USD pair is trading at 0.7365; the instrument is still moving above Ichimoku Cloud, which means that it may continue growing. We should expect the price to test Tenkan-Sen and Kijun-Sen at 0.7325 and then continue moving upwards to reach 0.7440. However, the scenario that implies further growth may be cancelled if the price breaks the downside border of the cloud and fixes below 0.7225. In this case, the pair may continue falling towards 0.7130.

USD/CAD, “US Dollar vs Canadian Dollar”

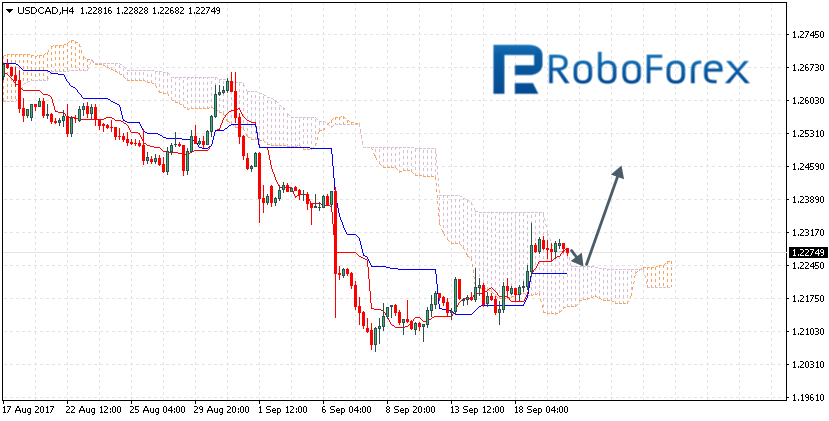

The USD/CAD pair is trading at 1.2274; the instrument is still moving above Ichimoku Cloud, which means that it may continue growing. We should expect the price to test the upside border of the cloud at 1.2245 and then continue moving upwards to reach 1.2460. However, this scenario may be cancelled if the price breaks the downside border of the cloud and fixes below 1.2150. In this case, the pair may continue falling towards 1.2050.

Attention! Forecasts presented in this section only reflect the author’s private opinion and should not be considered as guidance for trading. RoboForex LP bears no responsibility for trading results based on trading recommendations described in these analytical reviews.

EUR/USD: Fed balance sheet unwinding is largely priced in

Macroeconomic overview: We expect the Committee to announce the gradual normalization of its balance sheet today. Despite lower inflation readings and other headwinds – increased geopolitical risk, fiscal fights in Washington and the unknown economic consequences of the latest natural disasters – Fed officials have, until recently, reiterated that the announcement should be made “relatively soon”. In our view, this means the announcement will be made today. The most relevant comments in this respect were made at the beginning of this month by the Fed’s vice chair, William Dudley, and by usually dovish governor Lael Brainard. As laid out before, balance-sheet normalization is to be achieved by decreasing the amount of maturing debt that will be reinvested. In this process the Fed will reinvest maturing bonds only to an extent that they will surpass a defined cap level. The initial monthly cap is USD 10bn (USD 6bn of USTs and USD 4bn of MBS). This will increase on a quarterly basis by USD 10bn until it reaches USD 50bn per month (USD 30bn of USTs and USD 20bn of MBS). That means that, after the initial announcement, balance-sheet normalization will be on autopilot.

With the balance-sheet announcement being broadly expected, the bigger question may actually be whether the FOMC will adjust its outlook for short-term interest rates. We do not think it will and anticipate that FOMC members’ median interest-rate projections (the “dots”) will continue to show another rate hike occurring this year, followed by three more in 2018 and another three in 2019. To be sure, a few individual members may downgrade their rate expectations, but this is unlikely to be enough to move the median. If anything, the biggest risk is for a downward revision of the 2019 “dot”. The newly introduced 2020 forecast is likely to show no, or only very limited, further tightening beyond 2019. This is because the median dot for 2019 should be confirmed at 3% or slightly below, which is in line with the Fed’s estimate for the equilibrium rate, and the FOMC probably does not want to indicate tightening beyond that level at this point. The Fed’s economic and inflation forecasts should remain pretty much unchanged as well compared to June. That implies ongoing GDP growth of around 2%, a decline in the unemployment rate to 4%-4.25% and, most importantly, a return to 2% inflation by the end of 2018.

Similar to the Fed’s Summary of Economic Projections, the post-meeting statement is unlikely to contain important changes either. Most importantly, it will reiterate that the FOMC expects that “economic conditions will evolve in a manner that will warrant gradual increases in the federal funds rate”, while it “is monitoring inflation developments closely”. With all written releases almost unchanged, Fed Chair Janet Yellen’s press conference will remain an important wildcard. While Janet Yellen is also likely to reiterate the baseline outlook, she will certainly acknowledge the increased risks and may sound a tad more cautious about the timing of the next rate hike. For now, we continue to see the next move as occurring in December.

We do not think the Fed announcing the start of its balance sheet normalization will be a game changer for EUR/USD. The unwinding of the balance sheet is largely priced in as, other than the start date, we already know a fair amount of detail.

As far as the dot plot is concerned, any dovish changes may be taken as a confirmation of the market’s skepticism regarding the Fed’s rate hike intentions. That said, the drop in yields since the last FOMC meeting – and the generally low probability of a rate hike priced in by the market over the next two years – suggests that this is also at least partly in the price.

We see the risks for EUR/USD as balanced.

Technical analysis: EUR/USD extends to a new recovery high today at 1.2019 and the time spent above the 14-day exponential moving average gives hope to EUR/USD bulls. September 11 high at 1.2039 is the next resistance.

Short-term signal: Stay long for 1.2250.

Long-term outlook: Bullish

EUR/CHF at its highest since January 2015

Macroeconomic overview: The Swiss franc fell to its lowest level in over two years against the euro on Tuesday, as relative calm over North Korea eased demand for perceived safe-haven currencies.

The franc, which tends to gain in times of crisis, fell as much as half a percent to 1.1565 francs per euro in London trade. That was its lowest level since January 15, 2015, when the Swiss central bank dropped the franc’s “cap” against the euro.

In a move only punctuated by short-lived spikes on geopolitical tensions, the Swiss currency has weakened more than 8% against the euro this year.

That prompted the Swiss National Bank last week to temper its view of the franc’s over-valuation. The central bank ditched its nearly three-year mantra that the franc was “significantly over-valued”, saying instead that the currency remained “highly valued”.

But we think the shift in language should not be taken as heralding a departure from the SNB’s ultra-loose monetary policy. While the SNB is in no rush to tighten policy, other central banks (ECB, BOE) are moving closer to tightening policy, that is starting to feed through some downward pressure on the CHF.

Technical analysis: The EUR/CHF remains above 14-day exponential moving average and broke above August 4 high of 1.1537. This opens the way to further gains, as fundamentals supports stronger EUR/CHF.

Short-term signal: We stay long. Target raised to 1.1690.

Today, before the opening of the European session, gold was trading at 1,313.54 USD per Troy ounce. This is the second day in a row that gold has traded below the trend line on the 4-hour timeframe.

It’s still unclear whether the recent breakout of the trend line is false or not. I reckon that we could find out after the Federal Reserve meeting has ended. So, I’ll be looking either to buy or sell depending on the Fed’s decision. I’m considering the following two options:

First option

If the Fed decides to keep the key rate at its current level today, and maintain, or reduce, the current trajectory of rate hikes, I’ll be looking to sell. From a technical point of view, I’ll be looking to sell if gold follows the following trajectory on the H4 timeframe:

Conditions: After the Fed’s meeting ends, the price continues to fall, rebounds from the “double top” level or lower, subsequently forms a top lower than 1,320 – 1,325 USD, and continues to move downwards. If this scenario plays out, I’ll open a short position. I’d like to add that the more the Fed softens its stance on monetary policy, or its rhetoric, the better it will be for the US dollar in the short term, and worse for gold.

Second option

If the Fed decides today to raise the key rate, or maintain it at its current level of 1.00% – 1.25%, but significantly raises the trajectory of rate hikes (i.e. tightens its rhetoric on monetary policy), I’ll be looking to buy. From the technical side, I’ll be looking to open a trade if gold prices follow the scenario outlined in this 4-hour chart:

Conditions: The price continues to grow after the Federal Reserve’s meeting ends, before which it mustn’t dip below the double top level of 1,290 – 1,293 USD (so as not to break the upwards trend on H4). If growth continues, I’ll open a long position. The stronger the Fed tightens its monetary policy, or its rhetoric on the subject, the higher the price of gold will rise.

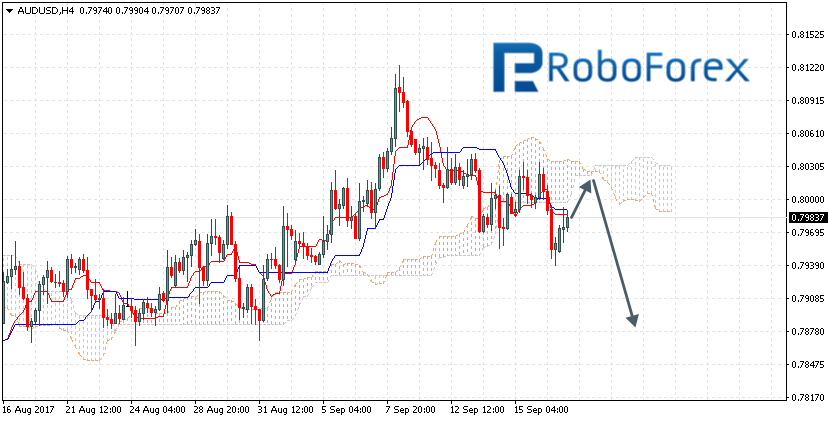

The AUD/USD pair is trading at 0.7983; the instrument is still moving below Ichimoku Cloud, which means that it may continue falling. We should expect the price to test the downside border of the cloud at 0.8025 and continue moving downwards to reach 0.7885. However, this scenario may be cancelled if the price breaks the upside border of the cloud and fixes above 0.8050. In this case, the pair may continue growing towards 0.8150.

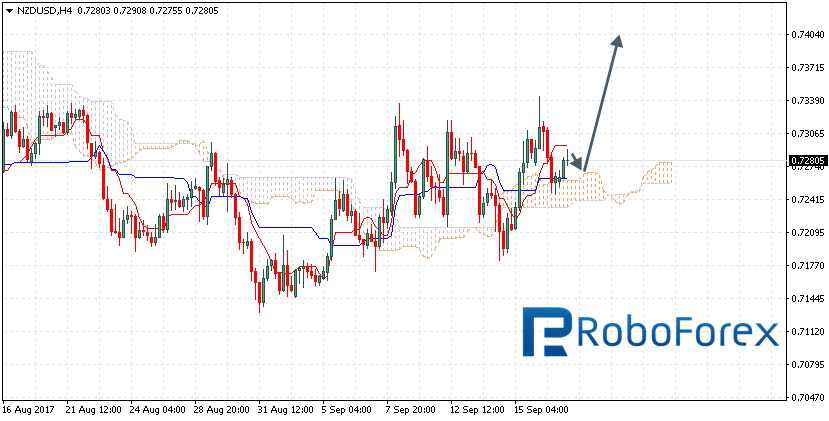

NZD/USD, “New Zealand Dollar vs US Dollar”

The NZD/USD pair is trading at 0.7280; the instrument is still moving above Ichimoku Cloud, which means that it may continue growing. We should expect the price to test the upside border of the cloud and then continue moving upwards to reach 0.7405. However, the scenario that implies further growth may be cancelled if the price breaks the downside border of the cloud and fixes below 0.7225. In this case, the pair may continue falling towards 0.7130.

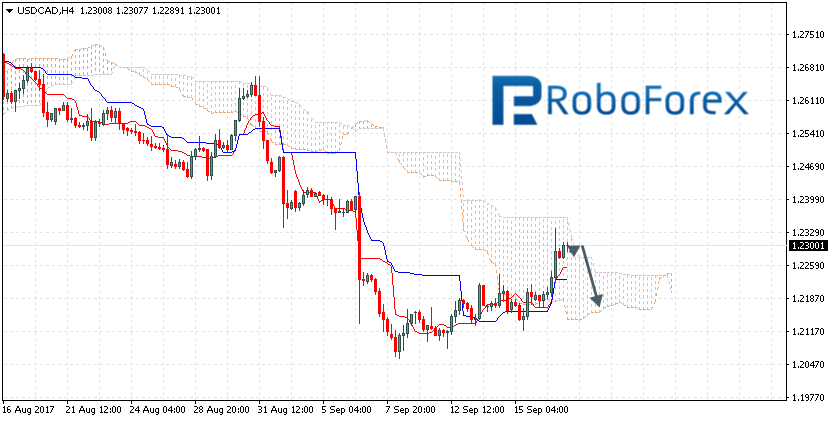

USD/CAD, “US Dollar vs Canadian Dollar”

The USD/CAD pair is trading at 1.2180; the instrument is still moving inside Ichimoku Cloud, which means that it is moving sideways. We should expect the price to test the upside border of the cloud at 1.2310 and then continue moving downwards to reach 1.2170. However, this scenario may be cancelled if the price breaks the upside border of the cloud and fixes above 1.2330. In this case, the pair may continue growing towards 1.2450.

Attention! Forecasts presented in this section only reflect the author’s private opinion and should not be considered as guidance for trading. RoboForex LP bears no responsibility for trading results based on trading recommendations described in these analytical reviews.