By OilPrice.com – Nigeria has long been known for its oil riches.

Angola has too, but decades of entrenched corruption have chased foreign investors away.

Now Namibia is joining the African oil conversation with one of the most oil-friendly regimes on the continent. It’s offering 5% royalties on what might just be a very productive shale play in Reconnaissance Africa’s (RECO.V) Kavango Basin.

Emerging markets are where oil upside might be found these days but navigating them is a challenge.

Nigeria: How To Push Away Investors

Take Nigeria, for instance.

Free Reports:

Get Our Free Metatrader 4 Indicators - Put Our Free MetaTrader 4 Custom Indicators on your charts when you join our Weekly Newsletter

Get Our Free Metatrader 4 Indicators - Put Our Free MetaTrader 4 Custom Indicators on your charts when you join our Weekly Newsletter

Get our Weekly Commitment of Traders Reports - See where the biggest traders (Hedge Funds and Commercial Hedgers) are positioned in the futures markets on a weekly basis.

Get our Weekly Commitment of Traders Reports - See where the biggest traders (Hedge Funds and Commercial Hedgers) are positioned in the futures markets on a weekly basis.

As Africa’s largest producer of oil, Nigeria has outsized status in the hydrocarbons world. But the party is coming to an end from an investor’s standpoint.

Nigeria is home to about 37 billion barrels in oil reserves. And while it’s got some 32 active oil rigs out there, only 81 wells were completed last year – down from 141 in 2014.

Since oil prices started tumbling in 2014, the government has been taking more from oil companies, with back taxes and new legislation. Now, it wants majors Chevron, Shell and French Total SA to pay them around $62 billion. It claims in was short-changed under a revenue-sharing agreement dating back to the 1990s.

Chevron (NYSE:CVX) is seeking to sell several Nigerian oilfields, and it isn’t the first: Exxon and Shell (NYSE:RDS.A) have both been reducing their footprint in the country.

And it might get worse.

Now, Nigeria is proposing new legislation that would increase taxation on the oil industry. The bill would add another 3-10 percent in royalty rates at oil prices between $50 and $80 per barrel. Nigeria’s current system gives Nigeria between 60 percent and 70 percent of all deepwater revenues, which includes taxes, royalties, along with state-run Nigerian National Petroleum Corporation’s share of production.

Angola: Reforms That Might Not Be Enough

Angola, too, is a tough sell right now. Even though it’s Africa’s second-largest producer, it’s been mired in decades of highly entrenched corruption, and while there is a new regime in power and reforms are on the books, investors aren’t 100-percent sold on the idea.

Angola is hoping to sell stakes in state-run Sonangol oil company and a string of other energy companies. To do that, it’s banking on major economic reforms to attract investors and bring in much-needed cash.

No one’s forgotten the gross mismanagement of Sonangol under its previous leadership, though, so the Angolan government is going to have to make people believe things have changed. Sonangol has a history it needs to overcome.

The goal is an IPO for Sonangol in 2022. Beyond that, the government is also hoping to lure investors into stakes in Puma Energy, the China-Sonangol oil venture, and the Ivory Coast SIR refinery. But it’s only been two years since we saw a change of regime in Angola, and investors don’t seem thoroughly convinced just yet.

In 2017, Joao Lourenco took power, ending the four-decade power play of Jose Eduardo dos Santos, along with his daughter’s destructive leadership of Sonangol. But two years may not be enough time to convince investors.

The government has made it easier for investors to repatriate money via commercial banks; it’s made it possible to invest in the sector without a local partner; and it cut taxes on some oilfields by 50%, creating an independent body for managing oil and gas concessions. The first litmus test will likely come later this year with the attempted sale of stakes in the SIR refinery.

But in the meantime, some bigger potential has emerged on the continent:

Namibia: Starting From Zero

Namibia – a country that has never produced a barrel – is the newest venue reaching the investment radar screen.

That’s because it has potential for new discoveries at a time when they are increasingly hard to come by.

Even better when it’s in an investor-friendly regime.

The so-called “Land of the Brave” has has an oil and gas friendly regime with only 5% royalties.

That’s why Exxon (NYSE:XOM) recently acquired an additional 7 million net acres from the government for a block extending from the shoreline to about 135 miles offshore in water depths up to 13,000 feet, with exploration activities to begin by the end of this year.

What Exxon’s banking on is that Namibia, which according to theory once fit together with Brazil, shares the same geology as Brazil’s pre-salt basins, Santos and Campos, which have already proved resource-rich, according to Deloitte.

But there’s also something onshore that has good potential.

Shale, and a basin that’s similar in size to the Eagle Ford basin in Texas.

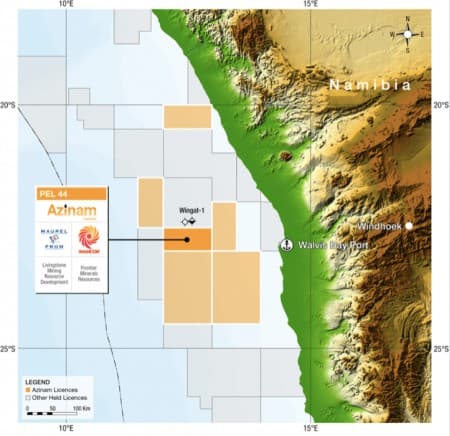

Welcome to the Kavango Basin.

Namibia’s Kavango Basin is part of the Karoo SuperGroup geology, and it’s also considered to have the same depositional environment as Shell’s Whitehill Permian shale play in South Africa.

Kavango is a 6.3-million-acre basin that potentially holds undeveloped shale and conventional plays. The entire basin is owned by a junior company called Reconnaissance Energy Africa (RECO.V) that recently received a 90% interest in the Petroleum Exploration Permit for the Kavango basin. The remaining 10% is owned by the Namibian state petroleum company.

When Reconnaissance Energy Africa took aeromagnetic data from the basin to the go-to geophysical interpreter Bill Cathey, according to Reconnaissance, Cathey said the data showed up to a 30,000 foot sedimentary basin.

The exploration permit is for 25,000 square kilometers (6.3 million acres). Usually, many companies hold the rights to such a large area whereas the Kavango is held by one company, Reconnaissance Energy Africa.

The reason for Reconnaissance Energy Africa (RECO.V) to take a chance on this is the fact that Kavango likely holds similar geology, deposited by the same Permian seaway, as Shell’s massive Permian shale play in South Africa, one of the top 10 shale plays in the world.

Recon is targeting for the same Permian shales at the lower portion of the Karoo Supergroup.

So far, Recon’s interpretation suggests that Kavango could be a big shale play in the Karoo Supergroup of rocks.

When it comes to exploration, Africa is one of the final frontiers for oil investors. And if it’s a junior explorer who makes a discovery and ends up sitting on a viable shale play, that becomes leverage for investors.

There are a lot of new companies in Namibia, but none with an entire basin as large as this.

Not only do they own the entire basin, but Reconnaissance Energy Africa (RECO.V) also has a 4-year exploration license for the basin, leading to a 25-year production license if there is a commercial production discovery.

Sproule–a tier 1 resource assessment company–estimated that Kavango has a potential 12 billion barrels of oil and 119 trillion cubic feet of natural gas. That’s for the shale, and there is also conventional potential.

The first well at Kavango is planned to be drilled in the second quarter of 2020, and this junior explorer Recon (RECO.V) is hoping for good results.

Other companies looking to find the next oil frontier:

Halliburton (NYSE:HAL) is one of the largest oilfield services companies in the world. The company has secured its place in the oil and gas industry. But it didn’t happen overnight.

The oilfield services sector is highly competitive and ripe with innovation. In order to stay ahead, companies must be on the absolute cutting edge of technology. And that’s exactly what Halliburton has done.

Schlumberger (NYSE:SLB) posted strong financials for the second quarter, with both revenue and earnings beating expectations. The oilfield services giant was hit hard by the oil market downturn, but will be one of the biggest beneficiaries of the rebound.

The international market is set to improve, meaning Schlumberger will profit on the shale drilling rush, but also on more drilling around the world.

Husky Energy Inc (TSX:HSE): This integrated oil and gas company out of Western Canada lives up to its name, fierce and driven for success. It’s already got a presence in some of the most well-known oil regions on the planet, but it hasn’t stopped there. It’s even positioned itself in Europe, Africa and as remote as the South China Sea.

Suncor Energy (TSX:SU): As one of the biggest names in energy, Suncor has adopted a number of high tech solutions for finding, pumping, storing, and delivering its resources.

While its primarily based out of North America, its assets in Africa and the Middle East should not be ignored. Though the oil downturn has weighed on the company’s share price this year, many analysts are pointing to a turnaround, from which Suncor is likely to benefit.

Tourmaline Oil Corp (TSX:TOU) is another Canadian resource producer focusing on exploration, production, development and acquisition within Western Canadian Sedimentary Basin. The company is in possession of an extensive undeveloped land position with long-term growth opportunities and a large multi-year drilling inventory.

Tourmaline’s strong leadership make the company a promising pick for investors looking to take advantage of the tremendous Canadian oil opportunities which are due for a strong rebound as oil prices inch higher.

Imperial Oil (TSX:IMO) still has some of the lowest cost producing oil sands in Canada and that is going to pay off as oil prices continue to rise and new tech breakthroughs bring breakeven prices even lower.

The management is well known for being conservative, but that certainly shouldn’t put investors off in a time when recovery is the buzzword of the day and consistency is sure to be rewarded.

Gibson Energy (TSX:GEI): has a long history in Canada’s oil and gas game. Established in 1953, Gibson knows the industry inside and out. The company has a diverse portfolio which includes transportation, storage, processing, marketing and distribution of oil, condensates, oilfield waste, refined products and natural gas.

With Gibson’s huge array of assets and its multi-platform sales strategies, investors look to Gibson with confidence.

Link to article: https://oilprice.com/Energy/

By Meredith Taylor

**IMPORTANT! BY READING OUR CONTENT YOU EXPLICITLY AGREE TO THE FOLLOWING. PLEASE READ CAREFULLY**

Forward-Looking Statements. Statements contained in this document that are not historical facts are forward-looking statements that involve various risks and uncertainty affecting the business of Recon. Such statements can be generally, but not always, identified by words such as “expects”, “plans”, “anticipates”, “intends”, “estimates”, “forecasts”, “schedules”, “prepares”, “potential” and similar expressions, or that events or conditions “will”, “would”, “may”, “could” or “should” occur. All estimates and statements with respect to Recon’s operations, its plans and projections, oil prices, recoverable oil, production targets, production and other operating costs and likelihood of oil recoverability are forward-looking statements under applicable securities laws and necessarily involve risks and uncertainties including, without limitation: risks associated with oil and gas exploration, development, exploitation and production, geological risks, marketing and transportation, availability of adequate funding, volatility of commodity prices, imprecision of reserve and resource estimates, environmental risks, competition from other producers, government regulation, dates of commencement of production and changes in the regulatory and taxation environment. Actual results may vary materially from the information provided in this document, and there is no representation that the actual results realized in the future will be the same in whole or in part as those presented herein. Other factors that could cause actual results to differ from those contained in the forward-looking statements are also set forth in filings that Recon and its technical analysts have made, We undertake no obligation, except as otherwise required by law, to update these forward-looking statements except as required by law.

Exploration for hydrocarbons is a speculative venture necessarily involving substantial risk. Recon’s future success will depend on its ability to develop its current properties and on its ability to discover resources that are capable of commercial production. However, there is no assurance that Recon’s future exploration and development efforts will result in the discovery or development of commercial accumulations of oil and natural gas. In addition, even if hydrocarbons are discovered, the costs of extracting and delivering the hydrocarbons to market and variations in the market price may render uneconomic any discovered deposit. Geological conditions are variable and unpredictable. Even if production is commenced from a well, the quantity of hydrocarbons produced inevitably will decline over time, and production may be adversely affected or may have to be terminated altogether if Recon encounters unforeseen geological conditions. Adverse climatic conditions at such properties may also hinder Recon’s ability to carry on exploration or production activities continuously throughout any given year.

DISCLAIMERS

ADVERTISEMENT. This communication is not a recommendation to buy or sell securities. Oilprice.com, Advanced Media Solutions Ltd, and their owners, managers, employees, and assigns (collectively “the Company”) may in the future be paid by the profiled company to disseminate future communications if this communication proves effective. In this case the Company has not been paid for this article. But the potential for future compensation is a major conflict with our ability to be unbiased, more specifically:

This communication is for entertainment purposes only. Never invest purely based on our communication. We have not been compensated but may in the future be compensated to conduct investor awareness advertising and marketing for TSXV:RECO. Therefore, this communication should be viewed as a commercial advertisement only. We have not investigated the background of the company. Frequently companies profiled in our alerts experience a large increase in volume and share price during the course of investor awareness marketing, which often end as soon as the investor awareness marketing ceases. The information in our communications and on our website has not been independently verified and is not guaranteed to be correct.

SHARE OWNERSHIP. The owner of Oilprice.com owns shares of this featured company and therefore has an additional incentive to see the featured company’s stock perform well. The owner of Oilprice.com will not notify the market when it decides to buy more or sell shares of this issuer in the market. The owner of Oilprice.com will be buying and selling shares of this issuer for its own profit. This is why we stress that you conduct extensive due diligence as well as seek the advice of your financial advisor or a registered broker-dealer before investing in any securities.

NOT AN INVESTMENT ADVISOR. The Company is not registered or licensed by any governing body in any jurisdiction to give investing advice or provide investment recommendation.

ALWAYS DO YOUR OWN RESEARCH and consult with a licensed investment professional before making an investment. This communication should not be used as a basis for making any investment.

PAST PERFORMANCE IS NOT INDICATIVE OF FUTURE RESULTS. Investing is inherently risky. Don’t trade with money you can’t afford to lose. This is neither a solicitation nor an offer to Buy/Sell securities. No representation is being made that any account will or is likely to achieve profits similar to those discussed.