June 1st – By CountingPips.com – Receive our weekly COT Reports by Email

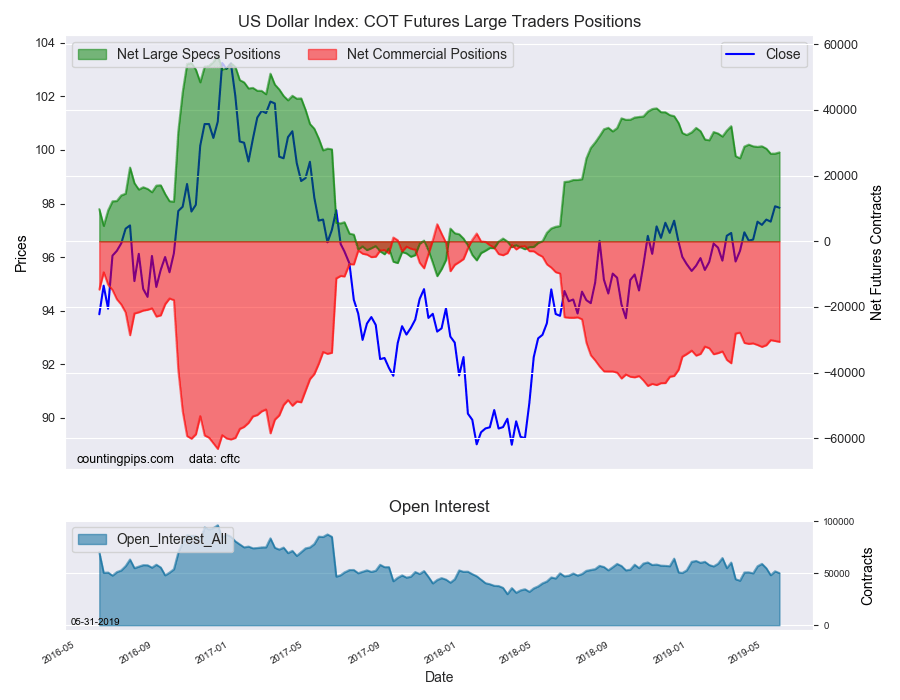

US Dollar Index Speculator Positions

Large currency speculators slightly lifted their net positions in the US Dollar Index futures markets this week, according to the latest Commitment of Traders (COT) data released by the Commodity Futures Trading Commission (CFTC) on Friday.

The non-commercial futures contracts of US Dollar Index futures, traded by large speculators and hedge funds, totaled a net position of 27,098 contracts in the data reported through Tuesday May 28th. This was a weekly rise of 386 contracts from the previous week which had a total of 26,712 net contracts.

This week’s net position was the result of the gross bullish position dropping by -1,481 contracts (to a weekly total of 41,919 contracts) while the gross bearish position fell by -1,867 contracts for the week (to a total of 14,821 contracts).

Speculator positions edged higher for a second week after having previously fallen for four out of the previous five weeks. Despite another week’s slight uptick, the recent trend of the USD Index bets steadily trending downward remains intact.

Overall, the current standing has now been under the +30,000 net contract level for eleven straight weeks after having been above that threshold for the previous thirty-two weeks in a row.

Free Reports:

Get Our Free Metatrader 4 Indicators - Put Our Free MetaTrader 4 Custom Indicators on your charts when you join our Weekly Newsletter

Get Our Free Metatrader 4 Indicators - Put Our Free MetaTrader 4 Custom Indicators on your charts when you join our Weekly Newsletter

Get our Weekly Commitment of Traders Reports - See where the biggest traders (Hedge Funds and Commercial Hedgers) are positioned in the futures markets on a weekly basis.

Get our Weekly Commitment of Traders Reports - See where the biggest traders (Hedge Funds and Commercial Hedgers) are positioned in the futures markets on a weekly basis.

Individual Currencies Data this week:

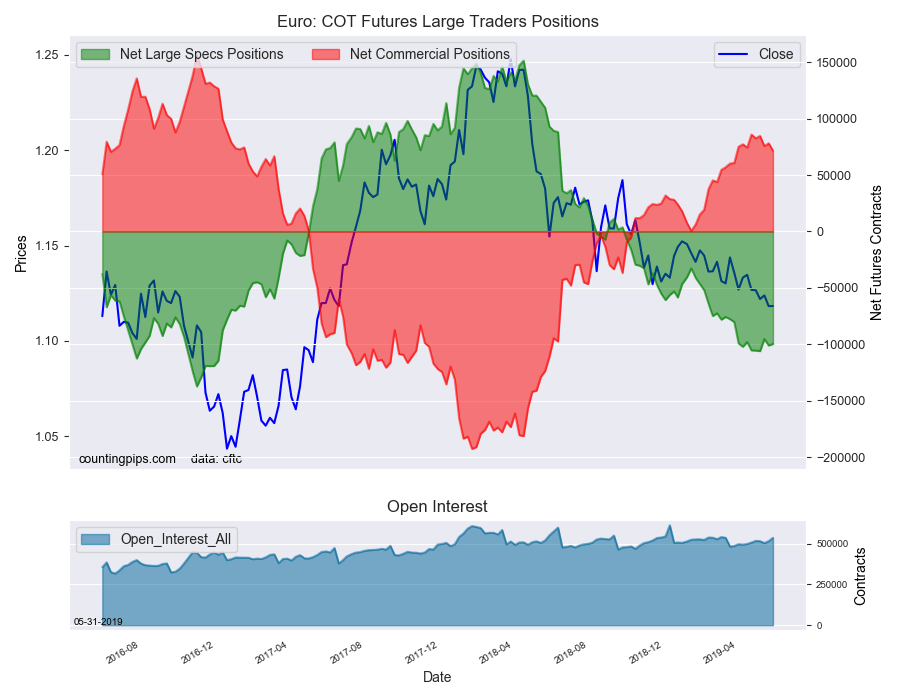

The major currencies that saw improving speculator positions this week were the US dollar index (386 weekly change in contracts), euro (1,411 weekly change in contracts), Swiss franc (2,820 contracts) and the Canadian dollar (2,813 contracts).

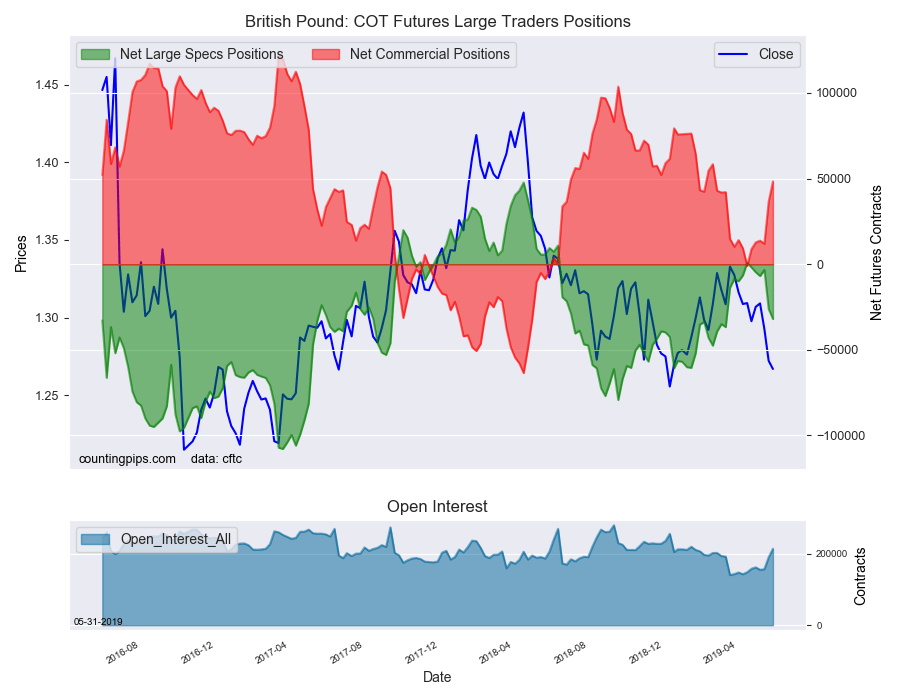

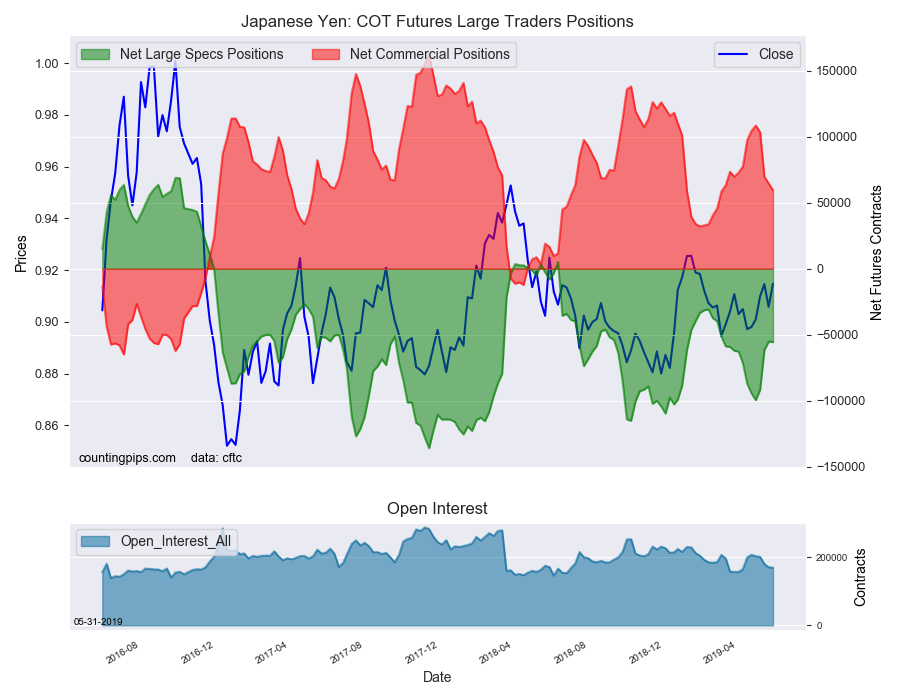

The currencies whose speculative bets declined this week were the British pound sterling (-5,844 contracts), Japanese yen (-385 contracts), Australian dollar (-282 contracts), New Zealand dollar (-5,284 contracts) and the Mexican peso (-4,018 contracts).

Notables for the week:

British pound positions declined for a second week and for the fifth time out of the past six weeks. The pound speculator position had recovered somewhat in early April after strong bearish levels leading up to the Brexit deadline. GBP bets even had a small bullish position on April 9th but have since turned downward again and now are at the most bearish level since March.

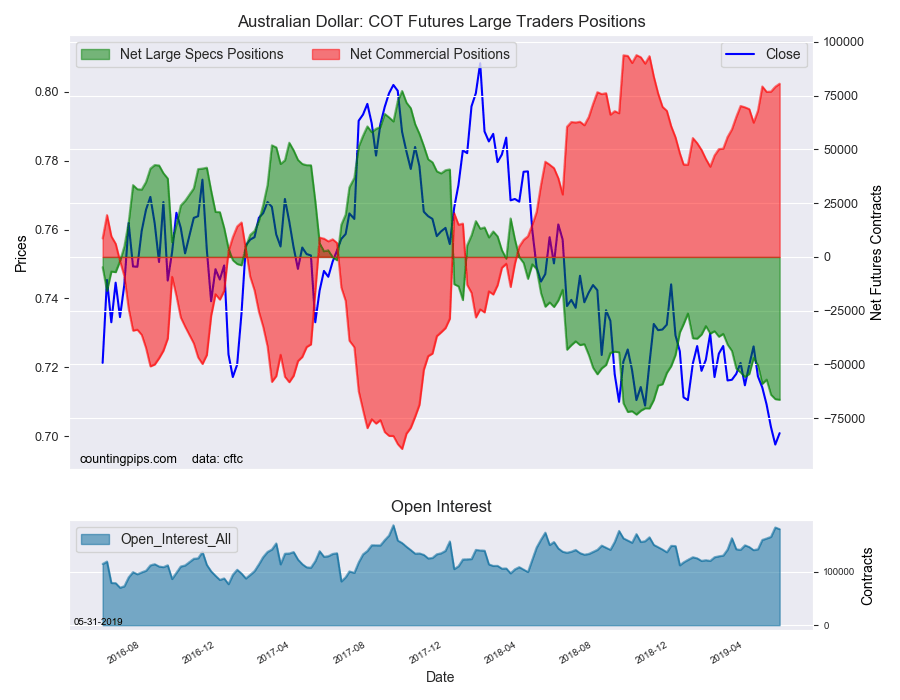

Australian dollar positions fell more bearish for a third straight week and for the fifth time out of the past six weeks. The net position is now at the most bearish level since November 6th of 2018.

Euro bearish positions decreased this week after having risen in eight out of the previous ten weeks. The current position is under the -100,000 contract level for just the second time in the past six weeks as speculator sentiment remains at very bearish levels.

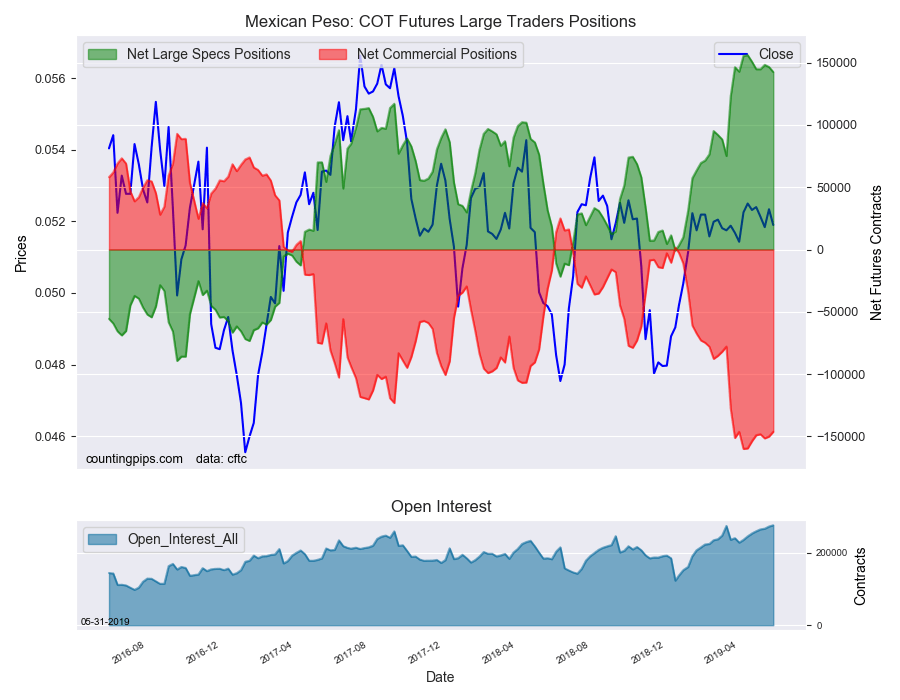

Mexican peso positions dipped for a second week this week and has now retreated in five out of the past six weeks. The peso position raced to an all-time record high bullish position on April 16th before turning lower recently.

See the table and individual currency charts below.

Table of Large Speculator Levels & Weekly Changes:

| Currency | Net Speculator Position | Specs Weekly Change |

| USD Index | 27,098 | 386 |

| EuroFx | -99,691 | 1,411 |

| GBP | -31,996 | -5,844 |

| JPY | -55,577 | -385 |

| CHF | -34,675 | 2,820 |

| CAD | -39,423 | 2,813 |

| AUD | -66,393 | -282 |

| NZD | -16,148 | -5,284 |

| MXN | 142,467 | -4,018 |

This latest COT data is through Tuesday and shows a quick view of how large speculators or non-commercials (for-profit traders) were positioned in the futures markets. All currency positions are in direct relation to the US dollar where, for example, a bet for the euro is a bet that the euro will rise versus the dollar while a bet against the euro will be a bet that the dollar will gain versus the euro.

Weekly Charts: Large Trader Weekly Positions vs Price

EuroFX:

The Euro large speculator standing this week resulted in a net position of -99,691 contracts in the data reported through Tuesday. This was a weekly boost of 1,411 contracts from the previous week which had a total of -101,102 net contracts.

British Pound Sterling:

The large British pound sterling speculator level came in at a net position of -31,996 contracts in the data reported this week. This was a weekly decrease of -5,844 contracts from the previous week which had a total of -26,152 net contracts.

Japanese Yen:

Large Japanese yen speculators resulted in a net position of -55,577 contracts in this week’s data. This was a weekly decline of -385 contracts from the previous week which had a total of -55,192 net contracts.

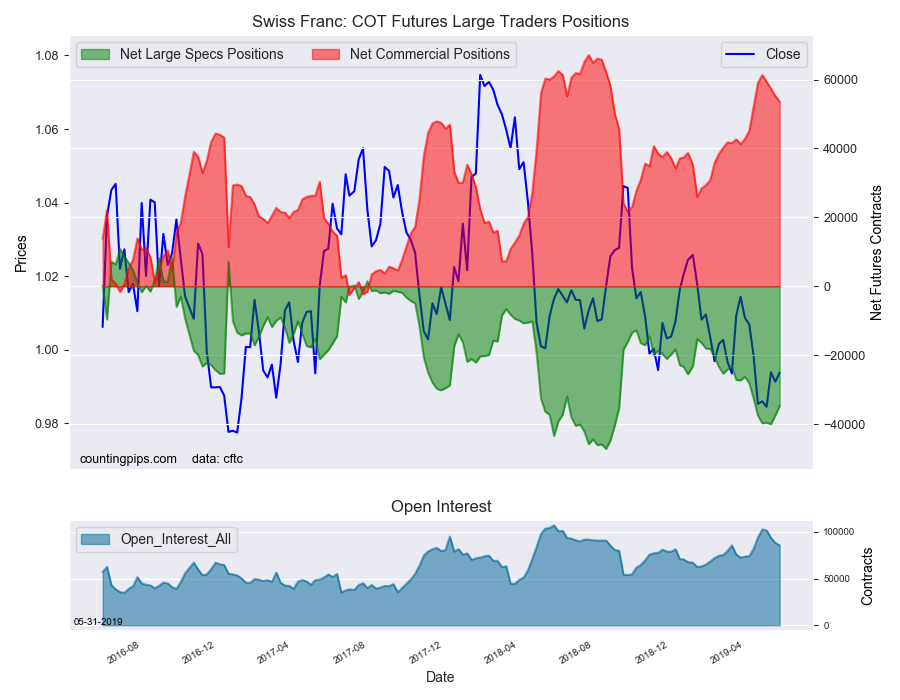

Swiss Franc:

The Swiss franc speculator standing this week was a net position of -34,675 contracts in the data through Tuesday. This was a weekly gain of 2,820 contracts from the previous week which had a total of -37,495 net contracts.

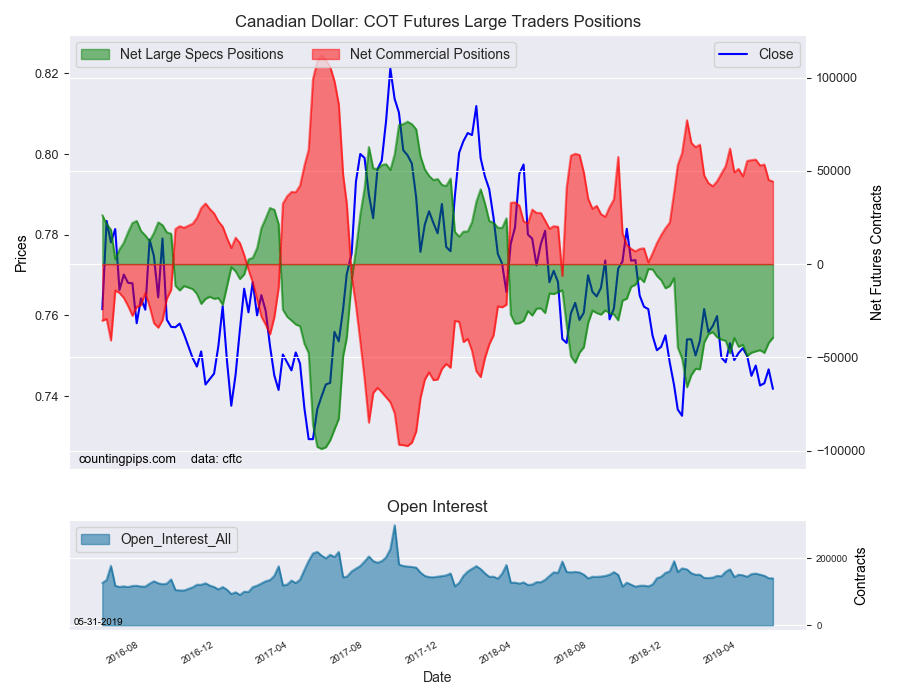

Canadian Dollar:

Canadian dollar speculators recorded a net position of -39,423 contracts this week. This was a advance of 2,813 contracts from the previous week which had a total of -42,236 net contracts.

Australian Dollar:

The large speculator positions in Australian dollar futures equaled a net position of -66,393 contracts this week in the data ending Tuesday. This was a weekly decline of -282 contracts from the previous week which had a total of -66,111 net contracts.

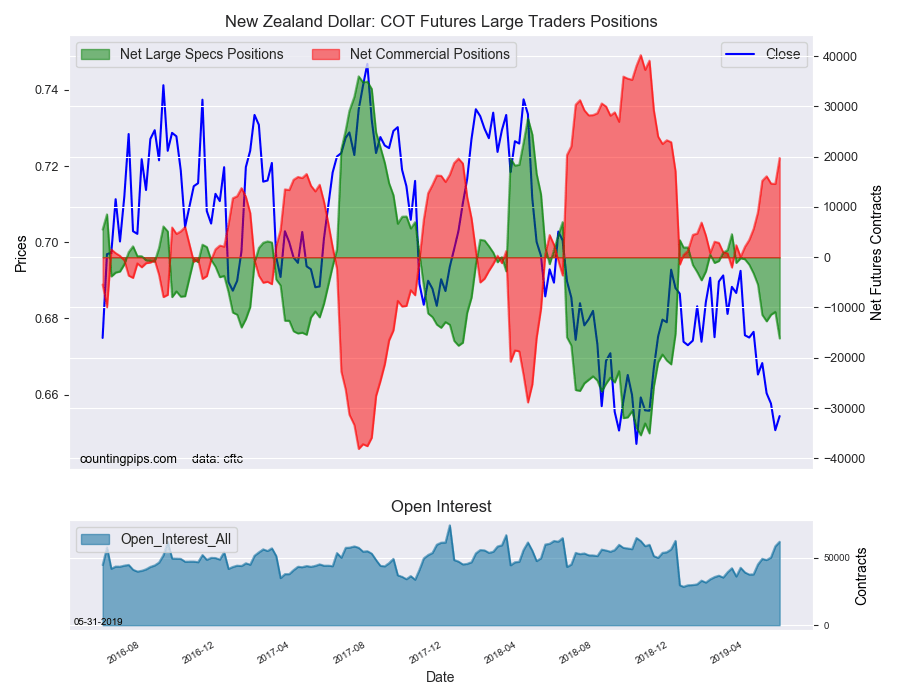

New Zealand Dollar:

The New Zealand dollar speculative standing came in at a net position of -16,148 contracts this week in the latest COT data. This was a weekly fall of -5,284 contracts from the previous week which had a total of -10,864 net contracts.

Mexican Peso:

Mexican peso speculators resulted in a net position of 142,467 contracts this week. This was a weekly lowering of -4,018 contracts from the previous week which had a total of 146,485 net contracts.

Article By CountingPips.com – Receive our weekly COT Reports by Email

*COT Report: The COT data, released weekly to the public each Friday, is updated through the most recent Tuesday (data is 3 days old) and shows a quick view of how large speculators or non-commercials (for-profit traders) were positioned in the futures markets.

The CFTC categorizes trader positions according to commercial hedgers (traders who use futures contracts for hedging as part of the business), non-commercials (large traders who speculate to realize trading profits) and nonreportable traders (usually small traders/speculators).

Find CFTC criteria here: (http://www.cftc.gov/MarketReports/CommitmentsofTraders/ExplanatoryNotes/index.htm).