April 6th – By CountingPips.com – Receive our weekly COT Reports by Email

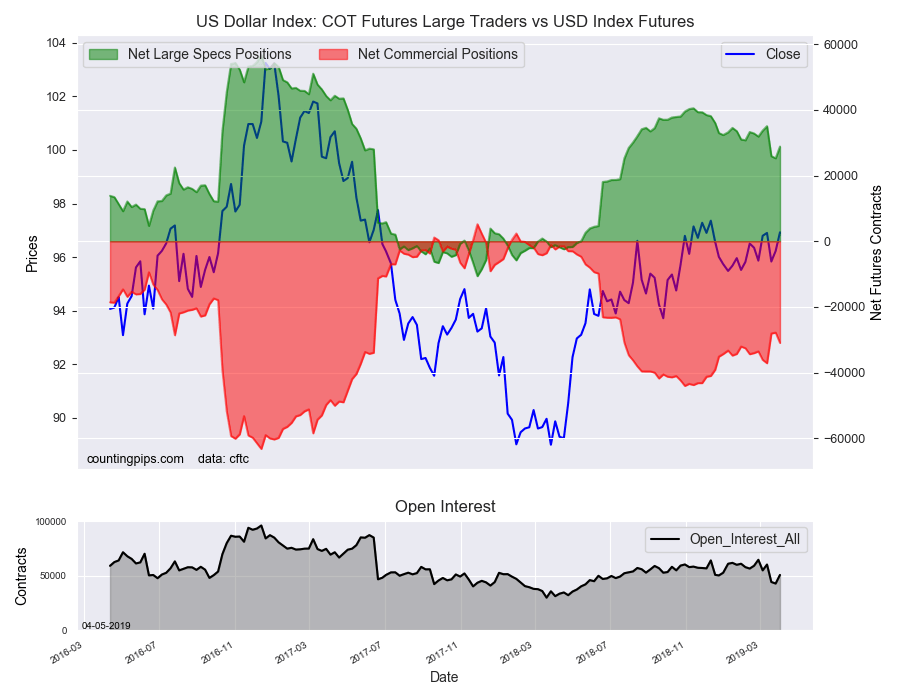

US Dollar Index Speculator Positions

Large currency speculators advanced their bullish net positions in the US Dollar Index futures markets this week, according to the latest Commitment of Traders (COT) data released by the Commodity Futures Trading Commission (CFTC) on Friday.

The non-commercial futures contracts of US Dollar Index futures, traded by large speculators and hedge funds, totaled a net position of 28,848 contracts in the data reported through Tuesday April 2nd. This was a weekly gain of 3,563 contracts from the previous week which had a total of 25,285 net contracts.

This week’s net position was the result of the gross bullish position (longs) advancing by 7,831 contracts to a weekly total of 44,774 contracts while the gross bearish position (shorts) rose by a lesser amount of 4,268 contracts for the week to a total of 15,926 contracts.

The USD net speculative futures position had fallen in the previous two weeks before this week’s turnaround. The current standing strongly remains in bullish territory for speculators but is under the +30,000 net contract level for a third straight week. The USD Index net standing had been above this level for the previous thirty-two straight weeks.

Individual Currencies Data this week:

In the other major currency contracts data, we saw just one substantial change (+ or – 10,000 contracts) in the speculators category this week.

Free Reports:

Get Our Free Metatrader 4 Indicators - Put Our Free MetaTrader 4 Custom Indicators on your charts when you join our Weekly Newsletter

Get Our Free Metatrader 4 Indicators - Put Our Free MetaTrader 4 Custom Indicators on your charts when you join our Weekly Newsletter

Get our Weekly Commitment of Traders Reports - See where the biggest traders (Hedge Funds and Commercial Hedgers) are positioned in the futures markets on a weekly basis.

Get our Weekly Commitment of Traders Reports - See where the biggest traders (Hedge Funds and Commercial Hedgers) are positioned in the futures markets on a weekly basis.

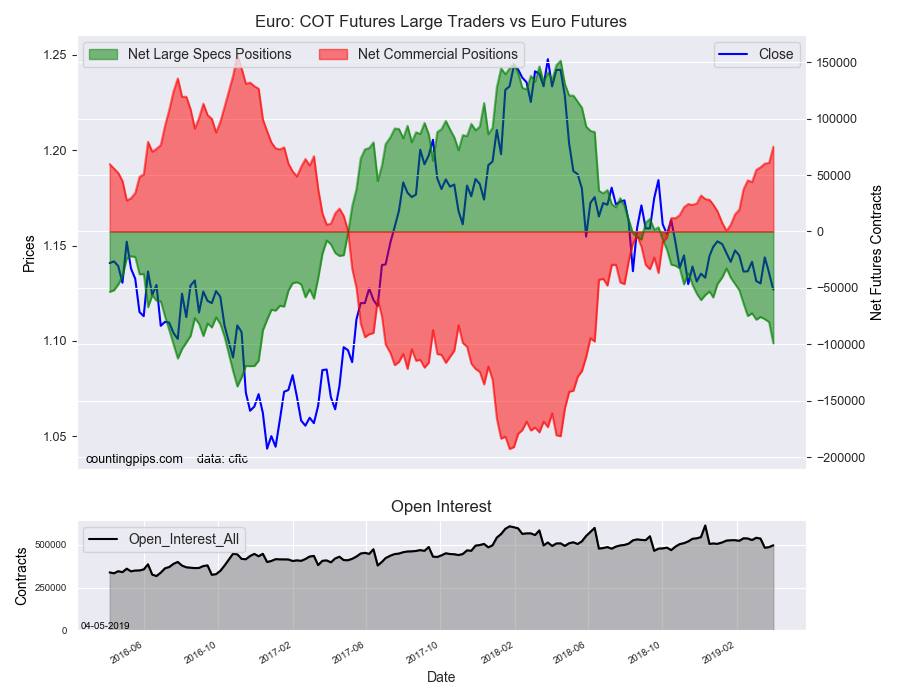

Euro currency positions dropped by over -18,000 bets this week and declined for a third straight week. The overall euro position is currently at the most bearish level since December 6th of 2016 when the net position totaled -114,556 contracts.

Overall, the major currencies that saw improving speculator futures positions this week were the US dollar index (3,563 weekly change in contracts) and the Swiss franc (1,029 contracts).

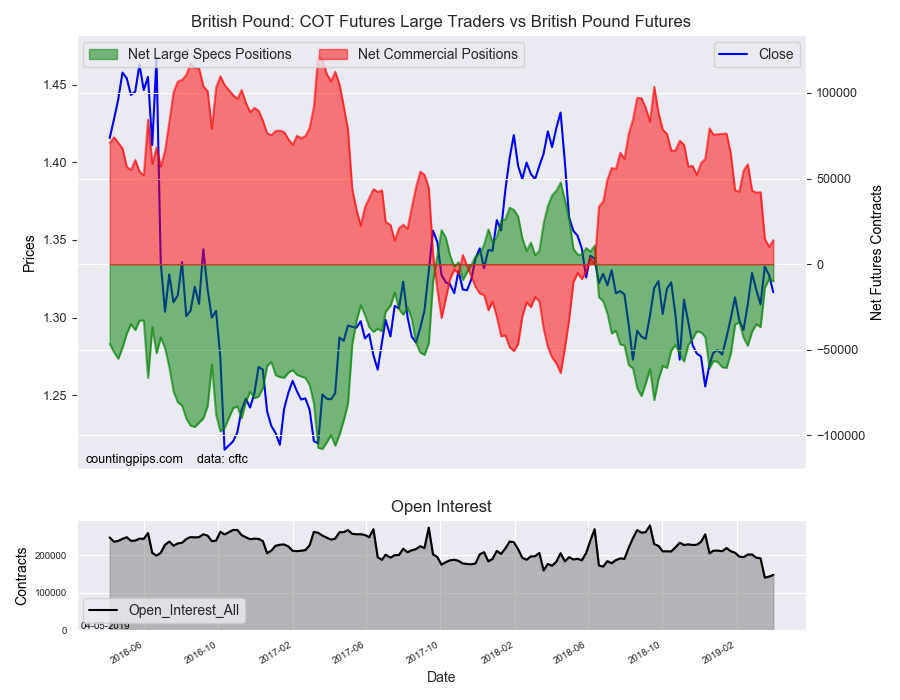

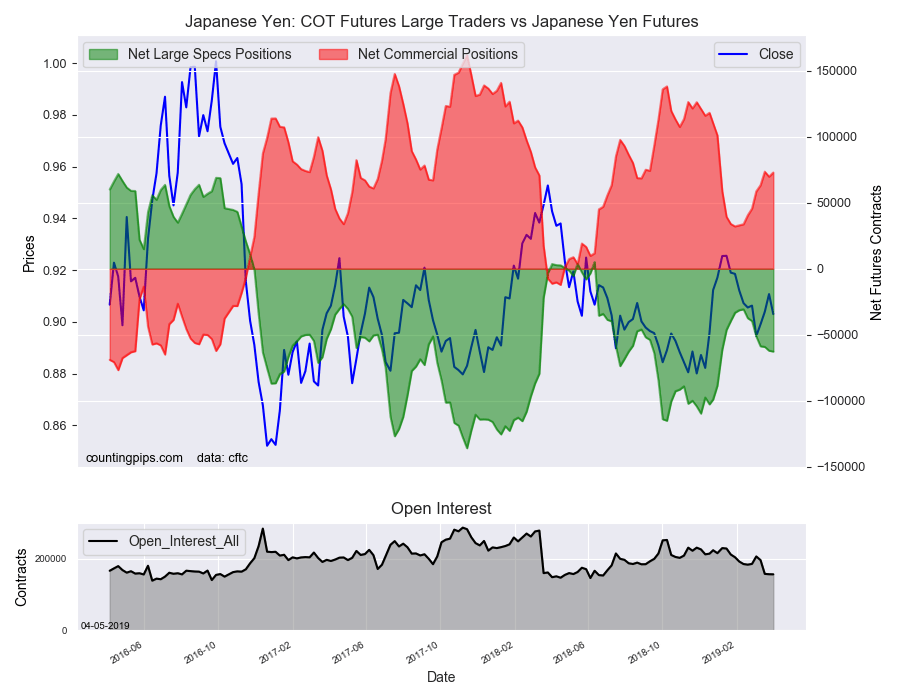

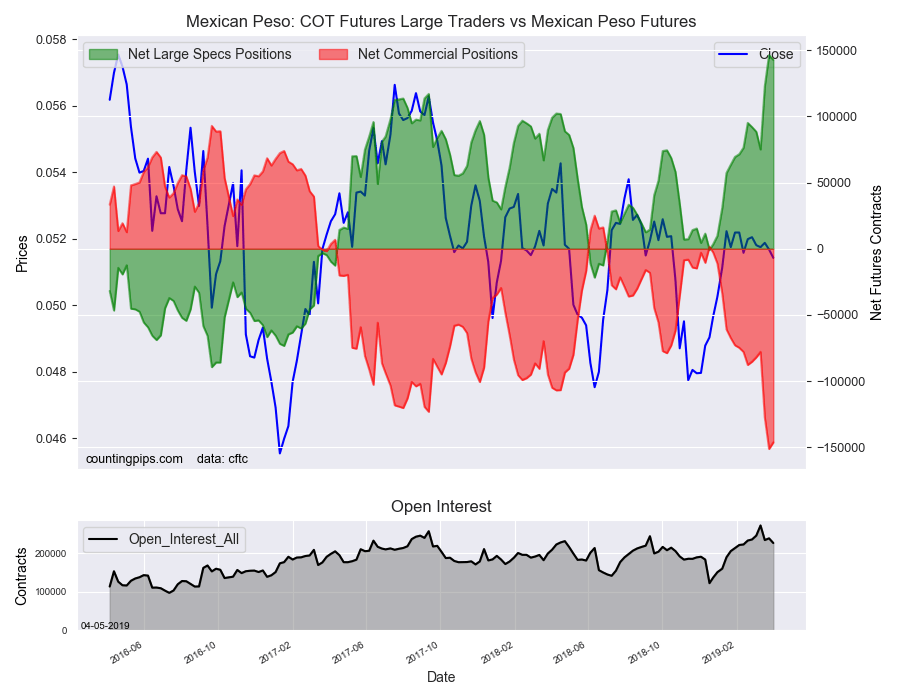

The currencies whose speculative bets declined this week were the euro (-18,906 weekly change in contracts), British pound sterling (-1,349 contracts), Japanese yen (-620 contracts), Canadian dollar (-4,752 contracts), Australian dollar (-2,073 contracts), New Zealand dollar (-203 contracts) and the Mexican peso (-3,611 contracts).

See the table and individual currency charts below.

Table of Large Speculator Levels & Weekly Changes:

| Currency | Net Speculator Position | Specs Weekly Change |

| USD Index | 28,848 | 3,563 |

| EuroFx | -99,184 | -18,906 |

| GBP | -9,931 | -1,349 |

| JPY | -62,741 | -620 |

| CHF | -26,266 | 1,029 |

| CAD | -44,323 | -4,752 |

| AUD | -55,743 | -2,073 |

| NZD | -405 | -203 |

| MXN | 142,723 | -3,611 |

This latest COT data is through Tuesday and shows a quick view of how large speculators or non-commercials (for-profit traders) were positioned in the futures markets. All currency positions are in direct relation to the US dollar where, for example, a bet for the euro is a bet that the euro will rise versus the dollar while a bet against the euro will be a bet that the dollar will gain versus the euro.

Weekly Charts: Large Trader Weekly Positions vs Price

EuroFX:

The Euro large speculator standing this week was a net position of -99,184 contracts in the data reported through Tuesday. This was a weekly decrease of -18,906 contracts from the previous week which had a total of -80,278 net contracts.

British Pound Sterling:

The large British pound sterling speculator level was a net position of -9,931 contracts in the data reported this week. This was a weekly fall of -1,349 contracts from the previous week which had a total of -8,582 net contracts.

Japanese Yen:

Large Japanese yen speculators recorded a net position of -62,741 contracts in this week’s data. This was a weekly decrease of -620 contracts from the previous week which had a total of -62,121 net contracts.

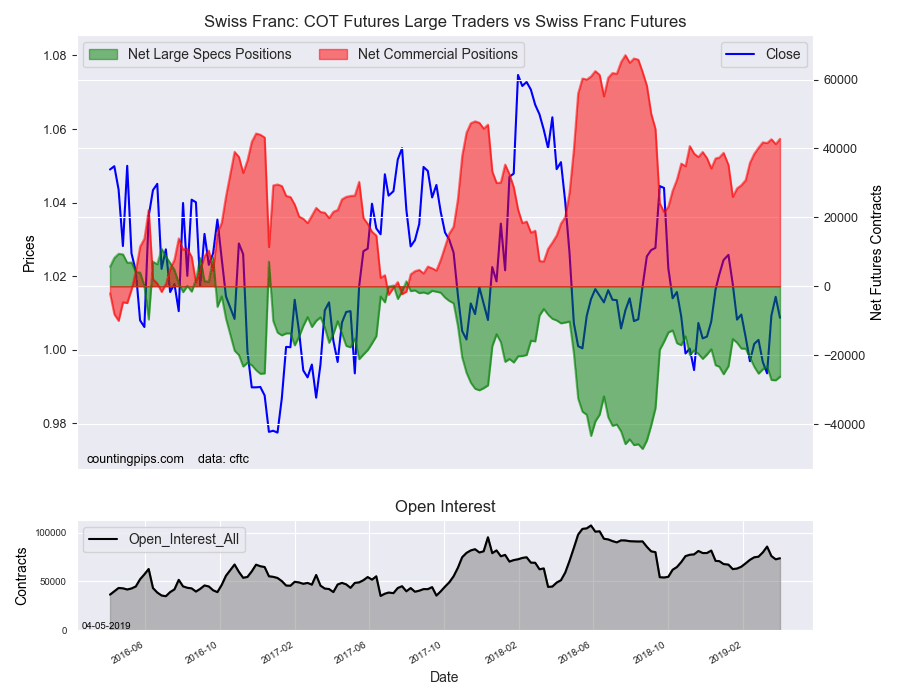

Swiss Franc:

The Swiss franc speculator standing this week recorded a net position of -26,266 contracts in the data through Tuesday. This was a weekly rise of 1,029 contracts from the previous week which had a total of -27,295 net contracts.

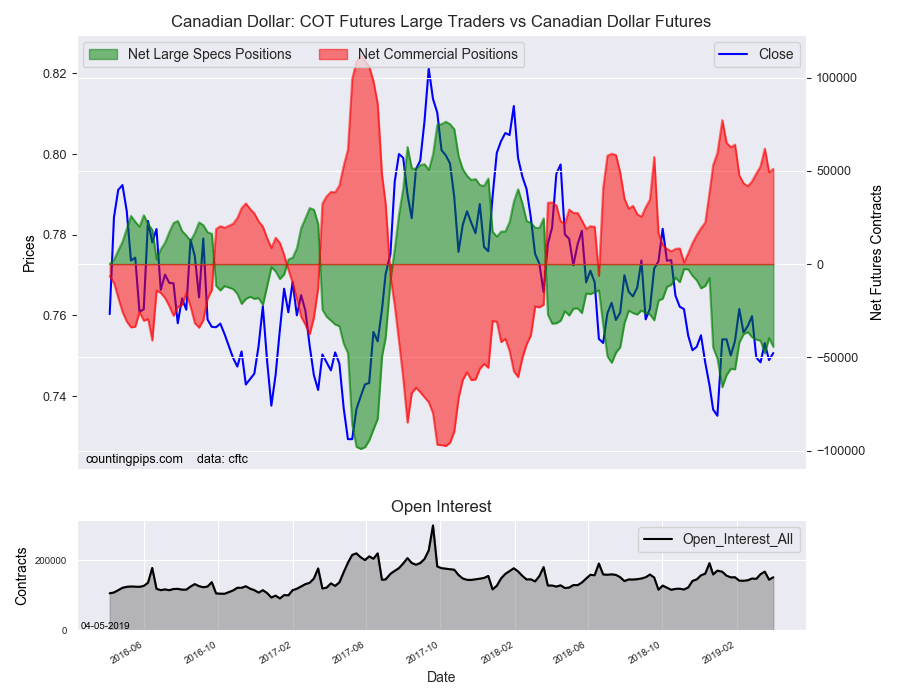

Canadian Dollar:

Canadian dollar speculators resulted in a net position of -44,323 contracts this week. This was a fall of -4,752 contracts from the previous week which had a total of -39,571 net contracts.

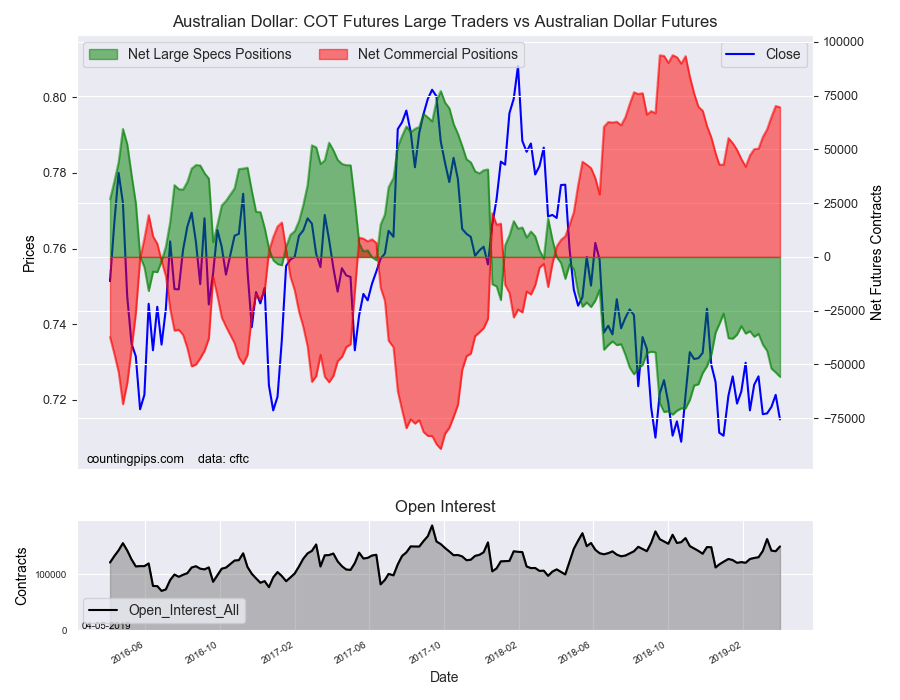

Australian Dollar:

The large speculator positions in Australian dollar futures reached a net position of -55,743 contracts this week in the data ending Tuesday. This was a weekly fall of -2,073 contracts from the previous week which had a total of -53,670 net contracts.

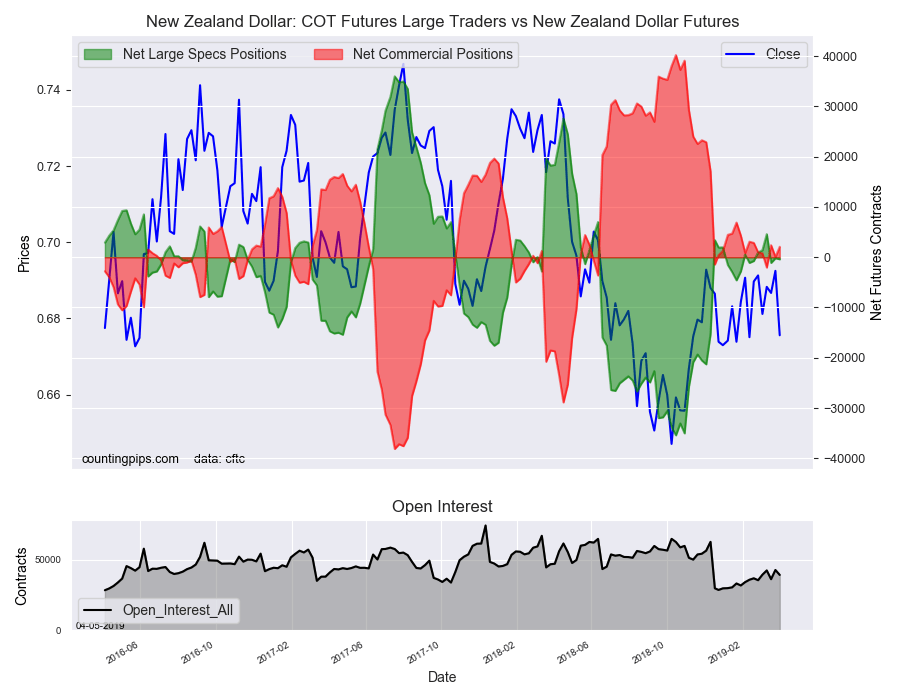

New Zealand Dollar:

The New Zealand dollar speculative standing resulted in a net position of -405 contracts this week in the latest COT data. This was a weekly decrease of -203 contracts from the previous week which had a total of -202 net contracts.

Mexican Peso:

Mexican peso speculators was a net position of 142,723 contracts this week. This was a weekly reduction of -3,611 contracts from the previous week which had a total of 146,334 net contracts.

Article By CountingPips.com – Receive our weekly COT Reports by Email

*COT Report: The COT data, released weekly to the public each Friday, is updated through the most recent Tuesday (data is 3 days old) and shows a quick view of how large speculators or non-commercials (for-profit traders) were positioned in the futures markets.

The CFTC categorizes trader positions according to commercial hedgers (traders who use futures contracts for hedging as part of the business), non-commercials (large traders who speculate to realize trading profits) and nonreportable traders (usually small traders/speculators).

Find CFTC criteria here: (http://www.cftc.gov/MarketReports/CommitmentsofTraders/ExplanatoryNotes/index.htm).