By IFCMarkets

The decline in world stock indices onn Thursday continued for the second day in a row. This was facilitated by both economic and political news. In yesterday’s review, we noted the rapid rise in The Oil prices to the 7-month high due to a new war in Iraq. The increased risks also had a negative impact on world stock markets. The U.S. authorities are exploring options for chiming in the conflict.

Meanwhile, the U.S. economic data yesterday were much weaker than expected. The retail sales increased only by 0.3% in May. Theoretically, investment banks may lower the U.S. GDP growth forecast for the second quarter. The number of new unemployed people per week was 317 thousand. While it was expected that there would be only 310 thousand. The import prices rose in May by 0.4% YoY, for the first time since last July. It’s not a big increase, but there is still a risk of import inflation. Amid falling S&P500 and Dow, the quotations of Home Depot (HD), Bank of America (BAC), Delta Airlines (DAL) and Boeing (BA) continued to decline, we wrote about it in the previous reviews noting the negative. On Thursday, the trading volume on the U.S. exchanges increased to 5.5 billion shares – 4% below the monthly average .

The European stocks fell yesterday in spite of the industrial production growth in the EU for April, more than expected. Investors are more interested in the global and the U.S. economy performance. In addition, they negatively perceived the statements of the Bank of England’s Mark Carney that his department may raise the interest rates “before the terms the financial markets expect this to happen”. The trading volume for the Stoxx 600 stock index was 24% below the monthly average. Today, we will see in the EZ news coming out at 9:00 CET, such as: the Q1 employment and the trade balance for April. We believe that the forecasts are positive.

The U.S. futures indexes are in a neutral trend this morning. We also expect the U.S. PPI to be released for May at 12-30 CET and the consumer confidence index from the University of Michigan for June 13-55 CET. In our opinion, the forecast is positive.

This morning, we saw the strong industrial retail sales and production data for May coming out from China. This has had a positive impact on commodities (food, metals and hydrocarbons). Investors believe that the so-called “mini-stimulus” by Li Keqiang’s government intended to support the economy, have a positive effect. The Chinese Shanghai Composite stock index shows the maximum weekly growth over the past two months. The Japanese Nikkei index has also risen. An additional positive were rumors of the corporate tax possible reduction. Note that today the Bank of Japan kept the money issue at 60-70 trillion Yen per year to stimulate the economy. This contributed to a slight weakening of the Yen (USDJPY) and also supported the Japanese stocks. Note that early on Monday morning, we expect data on sales from Japanese supermarkets to come out for May. They can affect the Nikkei. China is planning to announce the volume of new loans in local currency for May.

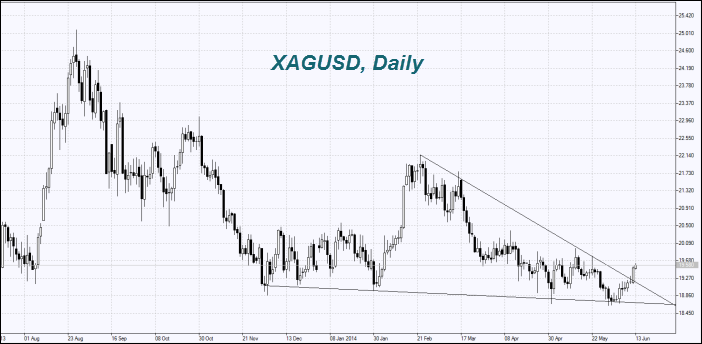

As it was expected, the Gold and Dilver showed a good growth on the correction of global stock markets.

The Oil continues to rise due to the war in Iraq. The Brent Oil reached a 9-month high. The International Energy Agency believes that the demand for the OPEC Oil will increase to 31 million barrels per day in the second half of this year, from the current 30 million. Since the total production of Iraq and Libya had fallen to less than 100 thousand barrels per day from 1.4 million last year. According to IEA, the global oil demand will increase to 94 million barrels per day in the fourth quarter of this year from 91.4 million in the first quarter. The Agency believes that can be met only by Saudi Arabia, which has 80% of the OPEC spare capacity. It is necessary, for the country to increase its production by 3 million barrels per day. The government representatives have not yet spoken on this issue. The OPEC has previously said that the need for production increase is absent. The possible increase in the demand at the end of the year should be compensated by the use of oil in developed countries.

Market Analysis provided by IFCMarkets