By CentralBankNews.info

Iceland’s central bank held its policy rates steady but warned that “the outlook for stronger domestic growth will require that the monetary stance be tightened sooner and more than previously expected.”

The Central Bank of Iceland, which maintained its benchmark seven-day lending rate at 6.0 percent in 2013 after raising it by 125 basis points in 2012, raised its forecast for growth and inflation due to the government’s debt relief measures that the bank’s expects will “boost private consumption considerably in the near future.”

The pace of the central bank’s rate tightening will depend on inflation – the central bank targets inflation of 2.5 percent – along with the government’s fiscal policy, the central bank added.

In its latest Monetary Bulletin the bank revised upwards its estimate for Iceland’s Gross Domestic Product growth in 2013 to 3.0 percent from its November forecast of 2.3 percent, helped by a strong recovery in the labour market and trade. The forecast for this year and the following two years has also been revised up so the slack in the economy will disappear earlier than expected.

Iceland’s GDP is forecast to expand by an unchanged 2.6 percent in 2014 but then grow by 3.7 percent in 2015, up from a previously-expected 2.8 percent, and by 3.0 percent in 2016, up from 2.0 percent forecast in November.

“If the forecast materializes, output growth will average 3.1 percent over the forecast horizon, which is above the 30-year average and well above the average projection for Iceland’s main trading partners,” the bank said.

Inflation in 2014 is expected to ease to an average of 2.7 percent, down from an estimated 3.9 percent in 2013, and lower than 3.2 percent forecast in November. The reason for the lower-than-expected inflation rate is because the rise in unit labour costs will be smaller than forecast by the bank provided that the wage talks concluded in December would be applied to the entire labor market.

In January Iceland’s headline inflation rate eased to 3.1 percent from 4.2 percent in December.

“The inflation outlook for the coming two years has deteriorated since the November forecast, however, as the outlook if for the slack in the economy to give way to an output gap during the period,” the central bank said.

In 2015 the bank expects inflation to average 3.4 percent, up from a previous 2.8 percent forecast, and 3.2 percent in 2016, up from 2.6 percent.

The central bank’s latest survey of market expectations from early February showed the bank’s collateralised lending rate remaining unchanged at 6.0 percent until the end of 2014, 0.5 percentage points lower in nominal terms than in the November survey.

But markets currently expect the central bank to raise its rate by 25 basis points in the first quarter of next year, rising to 6.5 percent in two years. Forward rates indicated that investors expect the bank’s policy rate to by by 50 basis points this year, 25 basis points higher than forward rates indicated in November.

The government’s debt relief package will be implemented over four years, estimated to cost 150 billion Icelandic krona, or 8.5 percent of the estimated value of Iceland’s GDP in 2013.

The central bank projects the measures will boost private consumption by 1.5 percentage points in 2014 and 2015, partly crowding out investment, but boosting GDP growth by about 0.2 percentage points. Imports will also rise, leading to a 1.0-1.5 percentage points drop in the forecast for the current account balance, putting pressure on the krona, which will boost inflation.

Iceland’s current account balance was estimated at a surplus of 3.0 percent of GDP in 2013, but this would decline to a surplus of only 0.8 percent this year, a deficit of 1.0 percent in 2015 and a deficit of 2.8 percent in 2016.

Private consumption in Iceland is now forecast to expand by 4.6 percent this year, up from an estimated 1.6 percent in 2013 and a previous forecast of 2.3 percent. In 2015 private consumption is forecast to rise by 4.3 percent, up from a previous 2.5 percent, and by 2.9 percent in 2016, up from 2.5 percent previously forecast.

“In part the effects of the debt relief package are absorbed through higher interest rates,” the bank said.

According to the bank’s quarterly macroeconomic monetary policy rule, the central bank’s policy rate will be some 0.3 percentage points higher than previously forecast in 2014, 0.6 percentage points higher in 2015 and nearly 1 percentage point higher from 2016.

“Higher interest rates therefore offset the impact of the debt relief measures on domestic demand, the exchange rate of the krona, and inflation,” the bank said in its bulletin.

However, the bank cautioned there was a great deal of uncertainty about the impact of the package due to the lack of historical precedent. Households could save more than assumed, growth and inflation will depend on how much the increased demand is directed toward imports versus domestic factors, and this will again affect the exchange rate. The government could also act to mitigate some of the negative effects of the measures, it said.

http://ift.tt/1iP0FNb

Commodities Remain The Favorite Asset

Despite the poor performance of last year, prices for raw materials remain popular in the portfolios of investment professionals in 2014, with preference to the cyclical metals. This is reflected in a survey of ETF Securities among 450 experts in commodities trading.

Commodities balance became in motion a little, only 20 % of respondents to this asset class continues to embrace the current year . Cyclic metals such as platinum and copper are the most sought after professionale investors . Also silver that was in dire straits last year , appears in the top three favorite commodities .

Risks

Besides opportunities, professionals also see risks looming for the commodity market, including the fear that the ongoing taper policy of the U.S. central bank will put a brake on the financial markets. They also point to concerns about a lower than expected growth in China and a possible slowdown in the U.S. economy.

The press release by ETF Securities can be read here: http://www.etfsecurities.com/institutional/uk/en-gb/news/commodities-back-in-favour–with-cyclical-metals-most-popular

Gold Prices Declines From Three Month High

Gold prices dropped from its highest level since November as advance in stocks reduced the demand for the metal.

Stocks were seen trading to its highest level in over two weeks, as the Federal Reserve’s (Fed) new Chairwoman Janet Yellen made her first speech before congress on Tuesday in which she hinted the Fed will go ahead with its target to slowly reduce its easing policy as the labour market recovers.

The yellow metal advanced 70% higher from December 2008 to June 2011 as the Fed injected over $2 trillion into the financial system.

Gold bounced back 6.7% amid the rise in physical demand and the Fed continues to reduce monthly bond purchases.

Gold declined 0.4% to $1,285.97 an ounce, after rising to its highest price of $1,293.93, the highest since Nov 14. The metal’s delivery for April fell 0.3% lower to $1,286 on the Comex in New York.

Stocks in China advanced on the unexpected rise in exports, which climbed to 10.6% in January, while imports rose 10% higher and the country’s traded surplus expanded.

Gold- Yellen Testimony

The Federal Reserve’s (Fed) new Chairwoman Janet Yellen made her first speech before congress on Tuesday in which she hinted the Fed will go ahead with its target to slowly reduce its easing policy regardless of the recent weak jobs data.

“The economic recovery gained greater traction in the second half of last year,” according to Yellen.

“If incoming information broadly supports the Committee’s expectation of ongoing improvement in labor market conditions and inflation moving back toward its longer-run objective, the Committee will likely reduce the pace of asset purchases in further measured steps at future meetings,” according to Fed Chair Yellen.

Visit www.hymarkets.com to find out more about our products and start trading today with only $50 using the latest trading technology today.

The post Gold Prices Declines From Three Month High appeared first on | HY Markets Official blog.

Article provided by HY Markets Forex Blog

Crude Prices Trades Higher on China Trade Balance Surplus

Crude prices advanced to its highest level on Wednesday after China released its upbeat trade data for January and reports showed distillate stockpiles dropped last week in the US, the world’s biggest oil consumer.

WTI for March delivery rose 0.55% higher to trade at $100.49 per barrel on the New York Mercantile Exchange at the time of writing. While the European benchmark Brent crude for March settlement gained 0.09% to $108.78 per barrel on the ICE Futures Europe exchange.

The continuous four-week gain in the North American crude was primarily driven by the extreme cold weather in the US, increasing the demand for energy.

Crude Inventories

According to reports from the American Petroleum Institute (API), crude oil inventories added 2.13 million barrels in the last week. The reports also revealed gasoline inventories declined by 479,000 barrels, compared to the forecast of a 100,000 barrel drop.

According to the Energy Information Administration (EIA), the extreme winter weather in the US could curb the rise in oil production as the low temperatures limit drilling of new oil wells.

The EIA are expected to release reports for its oil stockpiles later in the day.

China Trade Balance

China’s trade balance expanded in January, while the country’s imports and export growth surpassed predictions.

The surplus on trade came in at $31.9 billion in January, widening from the previous figure of $25.6 billion seen in the previous month and exceeding analysts’ forecast of a $23.6 million surplus, a release from the Customs General Administration of China confirmed.

While Import growth rose to 10%, compared to 8.3% growth seen in December. Exports growth exceeded analysts expectations, rising 10.6% year-on-year in January.

Yellen Testimony

The Federal Reserve’s (Fed) new Chairwoman Janet Yellen made her first speech before congress on Tuesday in which she hinted the Fed will go ahead with its target to slowly reduce its easing policy regardless of the recent weak jobs data.

“The economic recovery gained greater traction in the second half of last year,” according to Yellen.

“If incoming information broadly supports the Committee’s expectation of ongoing improvement in labor market conditions and inflation moving back toward its longer-run objective, the Committee will likely reduce the pace of asset purchases in further measured steps at future meetings,” according to Fed Chair Yellen.

Visit www.hymarkets.com to find out more about our products and start trading today with only $50 using the latest trading technology today.

The post Crude Prices Trades Higher on China Trade Balance Surplus appeared first on | HY Markets Official blog.

Article provided by HY Markets Forex Blog

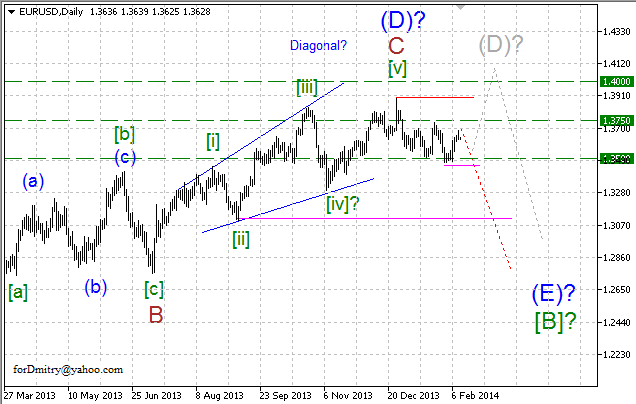

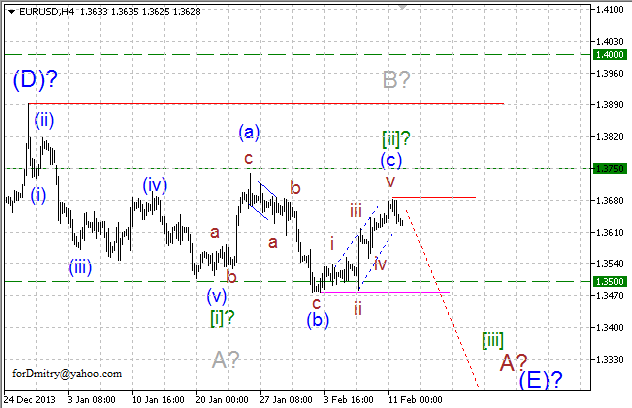

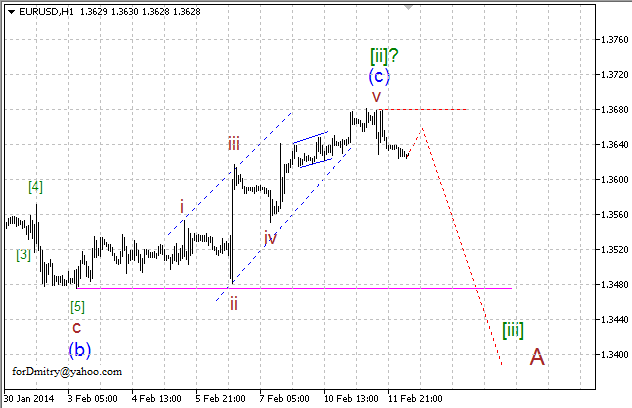

Wave Analysis 12.02.2014 (EUR/USD, GBP/USD, USD/CHF, USD/JPY)

Article By RoboForex.com

Analysis for February 12th, 2014

EUR USD, “Euro vs US Dollar”

Possibly, Euro completed ascending zigzag (D) of [B] and started forming final descending zigzag (E) of [B]. However, this assumption hasn’t been confirmed and price may yet change structure of wave (D).

Possibly, price is forming the first “leg” A of (E) of descending zigzag (E). Pair finished ascending correction [ii] of A of (E), which may be followed by descending impulse [iii] of A of (E).

Probably, pair finished ascending correction [ii] of A. In this case, later price is expected to start descending impulse [iii] of A.

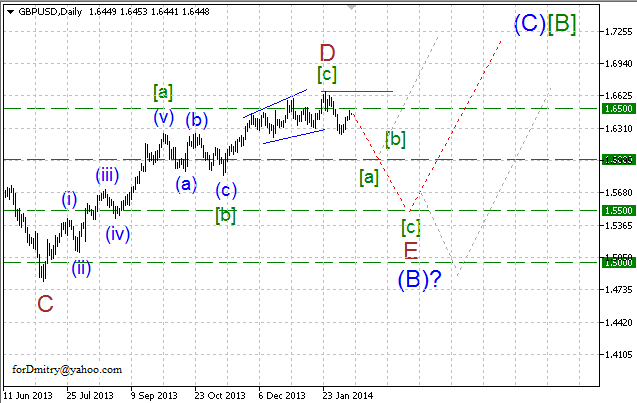

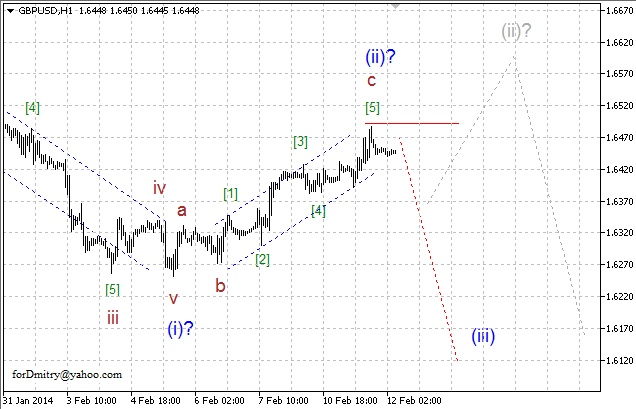

GBP USD, “Great Britain Pound vs US Dollar”

Possibly, Pound finished ascending zigzag D of (B). In this case, pair is expected to form final descending zigzag E of (B).

Probably, price started final descending zigzag E. Right now, pair is starting impulse (iii) of [a] of E.

Possibly, pair finished ascending correction (ii), which may be followed by descending movement inside wave (iii).

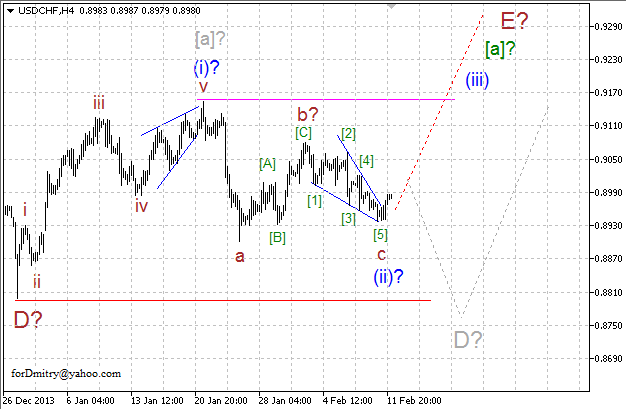

USD CHF, “US Dollar vs Swiss Franc”

Possibly, Franc completed descending zigzag D of (4) and started forming final ascending zigzag E of (4) of [C]. However, this assumption hasn’t been confirmed and price may yet change structure of wave D.

Probably, price completed descending correction (ii) of [a] of E of ascending zigzag E, which may be followed by ascending impulse (iii) of [a] of E.

Possibly, pair finished descending correction (ii) of [a], which may be followed by ascending impulse (iii) of [a].

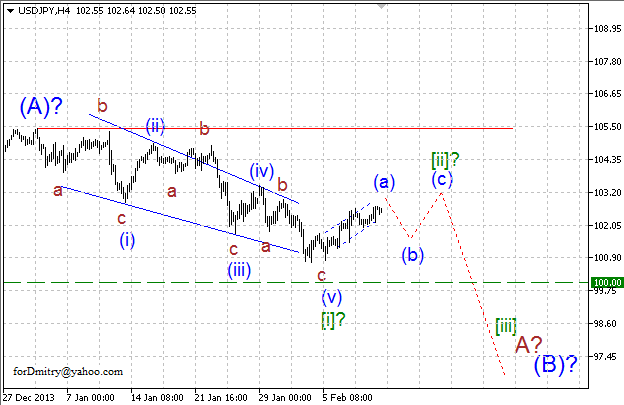

USD JPY, “US Dollar vs Japanese Yen”

Possibly, Yen finished ascending impulse (A). In this case, later price is expected to start large descending correction (B), may be in the form of zigzag.

Probably, pair finished impulse [i] of A of (B) of horizontal correction (B). Right now, price is forming local ascending correction [ii] of A, which may be followed by descending impulse [iii] of A.

Possibly, price is forming ascending correction [ii] of A in the form of zigzag, which may be followed by descending impulse [iii] of A.

RoboForex Analytical Department

Article By RoboForex.com

Attention!

Forecasts presented in this section only reflect the author’s private opinion and should not be considered as guidance for trading. RoboForex LP bears no responsibility for trading results based on trading recommendations described in these analytical reviews.

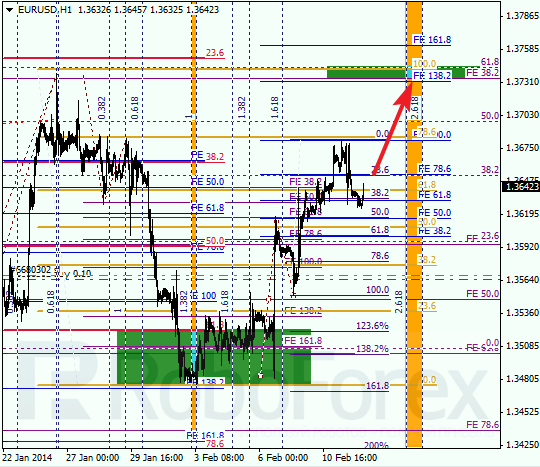

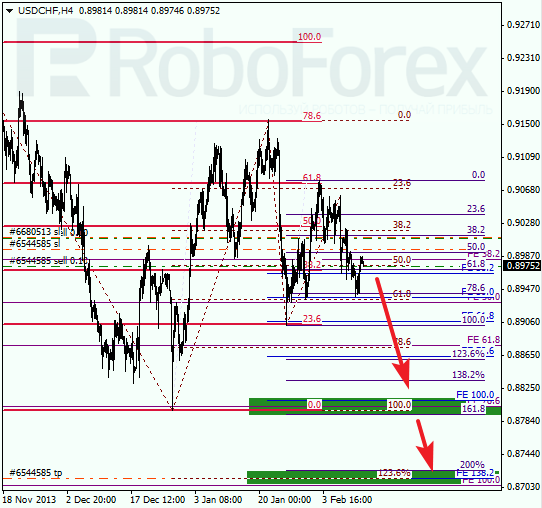

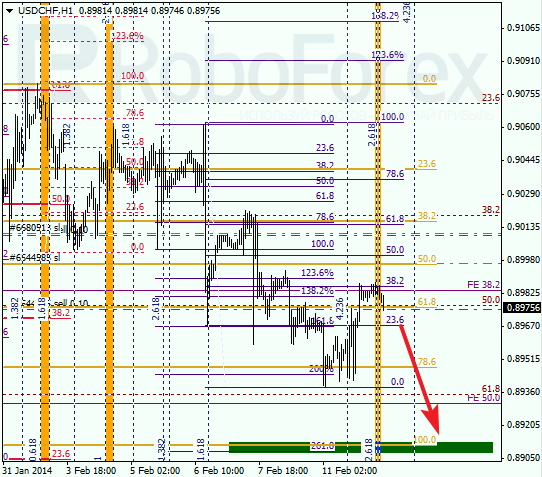

Fibonacci Retracements Analysis 12.02.2014 (EUR/USD, USD/CHF)

Article By RoboForex.com

Analysis for February 12th, 20142

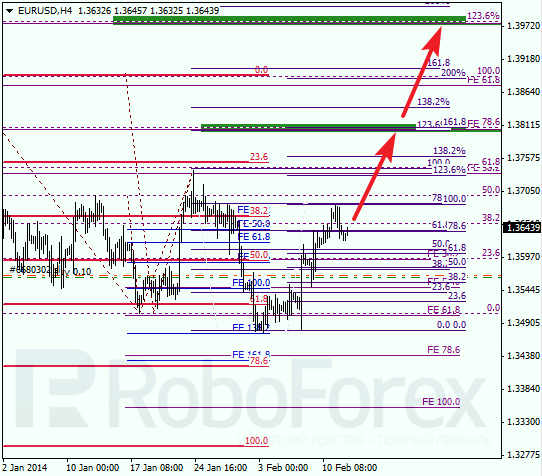

EUR USD, “Euro vs US Dollar”

After reaching one of intermediate levels, Euro started new correction. However, price may yet continue growing up. Closest important target is at level of 1.3810, which may be reached until the end of this week.

At H1 chart, correction reached local level of 38.2% and rebounded from it. Closest target is near several fibo-levels at 1.3735. According to analysis of temporary fibo-zones, this target area may be reached during the next 24 hours.

USD CHF, “US Dollar vs Swiss Franc”

Franc is also being corrected. Main targets are still in lower part of the chart. Market is expected to start new descending movement towards them during the next several hours.

At H1 chart, market reached local level of 38.2%. According to analysis of temporary fibo-zones, price may reverse. If price rebounds from this level, I’ll increase my short position.

RoboForex Analytical Department

Article By RoboForex.com

Attention!

Forecasts presented in this section only reflect the author’s private opinion and should not be considered as guidance for trading. RoboForex LP bears no responsibility for trading results based on trading recommendations described in these analytical reviews.

GBPUSD: Bullish, Risk Continues To Build On The Upside

GBPUSD: We continue to hold our bullish outlook on GBP as it looks to recover further higher. This development leaves it targeting the 1.6497 level, its Jan 30 2014 high as the next upside. Further out, resistance resides at the 1.6550 level where a breach will aim at the 1.6600 level, its psycho level. A turn above here will pave the way for a run at the 1.6667 level. Its daily RSI is bullish and pointing higher supporting this view. On the other hand, the risk to this analysis will be a return to the 1.6400 level where a breach will open the door for additional weakness towards the 1.6350 level and possibly lower towards the 1.6300 level. Further down, support comes in at the 1.6259 level. This level is expected to hold if tested thus turning GBP higher. On the whole, GBP continues to face bull threats.

Article by www.fxtechstrategy.com

World’s Most Dangerous Gorilla Dead At Age Seven

Famous American writer, Gore Vidal, wrote countless essays, novels and screenplays throughout his lengthy career. He even had a few Broadway plays and Academy Award-winning dramas under his belt.

Yet, after writing millions of words, there were only four he placed atop his list of favorites…

I told you so.

He claimed that these are the four most beautiful words in our common language.

It’s interesting, because most people loathe that expression… usually because it comes from a parent, snarky sibling, or know-it-all friend.

I myself have never been much of a fan of the phrase, and have avoided using it at all costs…

That is, until I took up shop at Wall Street Daily’s sister publication, Tech & Innovation Daily.

Since then, “I told you so” has become one of my favorite expressions. I absolutely love using it on my readers because, well… it means I’m doing my job.

And that’s why I’m writing to you today. Louis Basenese asked me to inform you of my most recent “I told you so” recommendation. It’s a stock that’s on fire as of late, and still has plenty of room to run…

Sapphire in the Rough

In October of last year, I started a series called “Tech All-Stars,” in which I profiled the top 14 stocks to own in 2014 for Tech & Innovation Daily subscribers.

One of those companies was GT Advanced Technologies (GTAT), a little-known sapphire manufacturer headquartered in New Hampshire.

Now, it’s important to note that by “sapphire,” I don’t mean the actual sapphire gemstone.

What I’m referring to is synthetic, manmade sapphire – the strongest, most scratch-resistant material on the market today. It’s virtually unbreakable. In fact, the only thing stronger and more durable is a diamond.

Synthetic sapphire is used to make vastly superior touchscreen displays. And the industry for the material is poised to reach $35 billion by 2018 (more than double its current amount), according to research firm, DisplaySearch.

That projection is certainly justified, too, if you consider the array of industries that incorporate touchscreen technology – like defense, aerospace and medical devices.

But sapphire’s most notable implementation will fall within one of the largest growth markets of the next decade: mobile technology…

The Gorilla in the Room

As it stands today, Corning’s (GLW) Gorilla Glass display technology has a stranglehold on the mobile market share, with its material implanted in over 1.5 billion mobile devices.

Gorilla Glass has made a profound impact on electronics manufacturers worldwide. It currently unveiled its fourth-generation model, dubbed Gorilla Glass 3 Antimicrobial. And though it’s 20% thinner, 40% more scratch resistant, and now kills bacteria on the go, it pales in comparison to GTAT’s sapphire screen.

In fact, GTAT’s technology is three times harder and three times more scratch resistant than the most advanced screen Corning has been able to put out to date.

So why, then, does Corning utterly dominate the mobile industry?

I think the O’Jays put it best in their 1973 hit song: “Money, money, money, money… MONEY!”

The cost (in terms of volume production) for Gorilla Glass is roughly $2 per screen. For one of GTAT’s screens, we’re talking upwards of $20.

And that’s the only problem lying at the heart of sapphire’s infancy. It’s just far too expensive at the moment. But like any investment in the technology, you can never think in terms of the here and now. You always need to think ahead of the curve.

But don’t take my word for it. Take Apple’s (AAPL)…

Gorilla Glass Heads for the Graveyard

One of the main reasons I zeroed in on GTAT back in November was the company’s established relationship with Apple – and the potential for the company to make deals with the tech giant down the road.

You see, GT Advanced already provides Apple with a sapphire cover for the iPhone 5S camera and fingerprint biometric sensor. And back in November, Apple had just increased sapphire orders from GT in what appeared to be a “trial run.”

That was great news for GTAT, as the deal boosted revenue for the company’s sapphire business to $28.9 million, or 11% of total year-to-date sales.

But when I looked a little deeper, something colossal seemed to be waiting in GTAT’s wings…

The company forecast that 2014 revenue would reach between $600 million and $800 million – with 80% of sales coming from the sapphire business.

Yet GT didn’t say exactly where the new sales boost was coming from…

But at the end of last week, Matt Margolis from 9to5mac released documents about Apple’s secretive plans with sapphire technology – and GTAT in particular.

As stated in the document, Apple signed a $578-million deal with GT Advanced Technologies to open and operate a sapphire manufacturing facility in Mesa, Arizona. (So after seven years, it looks like we’re saying goodbye to Gorilla Glass!)

The collaboration points to Apple ramping up its implementation of sapphire-crystal displays in future iPhone models.

And GTAT will need to boost its sapphire screen production to meet Apple’s needs. (At current capacity, GT Advanced can make up to 200 million screens per year. But that number will need to dramatically increase in order to put a sapphire touchscreen in every Apple product.)

When reports broke about the deal, GTAT shares shot through the roof. They jumped almost 30% by the time the market closed yesterday.

Of course, the stock is experiencing some profit-taking at this time. But that’s a good thing! Look for any weakness in GTAT as an opportunity to buy into the future of touchscreen technology on the cheap.

For more stories like this, head on over to the Tech & Innovation Daily site. We provide opportunities like GTAT on a daily basis.

Ahead of the tape,

Marty Biancuzzo

The post World’s Most Dangerous Gorilla Dead At Age Seven appeared first on Wall Street Daily.

Article By WallStreetDaily.com

Original Article: World’s Most Dangerous Gorilla Dead At Age Seven

Royal Nickel Corp: Indonesian Ore Export Ban Opens Door to the Next Generation of Nickel Mines

Source: Kevin Michael Grace of The Mining Report (2/11/14)

Nickel prices have been weak, but the recent Indonesian government announcement banning ore shipments outside the country may be the shock that reverses the trend. In this interview with The Mining Report, Mark Selby, senior vice president of business development for Royal Nickel Corp., walks through his analysis that indicates nickel price increases and inventory reductions are imminent, while demand continues to grow and over a quarter of global mine supply is shut in. He considers nickel in 2014 one of the best commodity trades in a generation. To capitalize on this unique set of circumstances, Royal Nickel’s Dumont Nickel Project follows the path of other large-reserve, large-scale mines in the copper and gold sectors that have changed the mining industry and made early investors fortunes.

MANAGEMENT Q&A: VIEW FROM THE TOP

The Mining Report: The nickel industry has been through tectonic changes in the last 10 years, including large corporate takeovers and fundamental changes in supply available to the market. Can you summarize where the nickel industry has been and where it is going?

Mark Selby: Over the past five years, we’ve seen continued robust growth in nickel demand. Over that period, global nickel demand grew in the high single-digits, while Chinese nickel demand grew at double-digit rates. Stainless steel, which is increasingly used across all sectors of the economy, accounts for approximately 70% of total nickel consumption.

Everyone is familiar with stainless steel appliances like refrigerators, but there are thousands of tons of stainless steel used in less obvious applications in the chemical, manufacturing and service sectors. A good example is just about every fast food outlet in the world, with their expanse of stainless steel counters and food prep equipment used throughout their operations. The nickel is there; it’s just not always easy for consumers to see.

There are a lot of exciting parts to the nickel story. From an economic point of view, one of the most interesting is price: nickel has historically been one of the most expensive of the common base metals (copper, lead, zinc, aluminum, etc.), which has steered its use in high-value applications such as jet engines, gas turbines, nuclear power plants and medical devices. As the Chinese economy moves up the value chain, the per capita consumption of the higher quality nickel alloys is increasing. In 2010, Chinese per capita consumption of nickel was only one third of the way to German or Japanese consumption levels, which China had already achieved in less value-added materials like carbon steel. Over this decade, we expect China to add at least a million tons more nickel demand as the economy continues on the path of industrialization.

There has been a lot of talk of a slowdown in the Chinese economy over the past few years. However, over that same timeframe, the Chinese nickel demand annual growth rate was in the mid-teens and added over 100,000 tons of nickel demand growth every year. No matter how you look at it, the demand side of the nickel story is robust. We don’t see any reasons why that will change in the near future.

TMR: Can you discuss the evolution of the supply situation in the nickel market? I am especially interested in the role of Indonesian ore and politics on nickel in the future.

MS: Back in the early 2000s, there was a whole cupboard full of undeveloped nickel projects that were idle. Most of those projects were discovered in the wake of a global nickel boom from the late 1960s-early 1970s. Those projects that were developed came on-line just in time for the global economy to slow down in the 1970s. As a result, there was a large inventory of deposits that sat idle.

When I worked at Inco, we saw the rapid growth in Chinese demand for nickel very early. It was clear to us that the development of nickel projects would not be quick enough to respond to the increase in demand. And that is what happened. Beginning in 2002-2004, and then again in 2005-2007, demand growth far outpaced supply growth. There were massive spikes in nickel prices as the industry just couldn’t keep up with the demand. Nickel prices went from $2 per pound ($2/lb) in 2001 to nearly $25/lb by 2007. That price spike in 2007 got many of these projects (which had been sitting idle for several decades) financed and into construction. Most of those projects were laterite deposits and many utilized new technologies, such as pressure acid leaching.

TMR: So, there was new mine supply, but what about the creation of the nickel pig iron (NPI) industry in China? That was a big change to the nickel industry.

MS: By 2006, Chinese stainless steel and nickel demand were growing at breakneck pace. And the nickel industry had provided little supply growth, so the Chinese did what the Japanese did in the 1960s, which was to take boatloads of soggy dirt (technically “ore”), primarily from Indonesia, and ship it to furnaces that they already built to make pig iron for carbon steel. That’s where the name “nickel pig iron” came from. The innovation was to build a low-capex, high-opex way of supplying nickel to their domestic industry. They created a Chinese ferronickel industry. Most new ferronickel plants in China use existing Rotary Kiln Electric Furnace (RKEF) technology to produce NPI. The only real operational innovation was to take the NPI all the way to stainless steel in a single facility while the NPI is molten. Even with improving technology and operational efficiency, NPI is a relatively expensive commodity to produce compared to nickel sourced from conventional mines.

The end result was a huge change in the industry. Starting in 2007 and then exploding over the next four or five years, the Chinese added a lot of capacity. For most of that time, they had a willing ore supplier in Indonesia that seemed willing to ship as much ore as the Chinese needed—despite capturing very little of the export value for the Indonesian economy.

The massive growth in NPI supply combined with the new production from the projects that came on-line in 2007 relieved the supply pressure on the market. In fact, the supply dynamics have created significant surpluses in the last two or three years, making nickel one of the least successful metals based on price appreciation.

So what does it mean for the future? We have seen the project backlog cleared out since 2007. We were already bullish for the second half of this decade based on Chinese demand growth, which we expect to continue to be robust, and a lack of new projects. This was even before the Indonesian ban.

TMR: The Indonesian ore export ban was announced in mid-January. What are the implications for the nickel market?

MS: In January, the Indonesian government announced that they would ban all unprocessed nickel ore exports. This was a tectonic shift in the nickel market. I expect this action to dramatically pull forward the shortages we expected to see anyway. Under the current conditions, by the second half of 2015 we expect severe nickel shortages to emerge and will start seeing the first signs this month. That is about how long it will take to work through the inventory once 25–30% of global nickel supply has been shut in with this export ore ban.

TMR: Is the ore for the Chinese NPI producers mostly from Indonesia?

MS: About 75% comes from Indonesia. There are two types of lateritic nickel ore from Indonesia—limonite and saprolite. The saprolite grading between 1.8-1.9% nickel is the most common ore. Notably, Indonesia is the only significant source for that higher grade material that’s available for export in any quantity.

The Philippines can supply probably 10–20% of what Indonesia’s currently supplying. The main ore there is limonite with a lower grade at 1.4-1.5% nickel. Again, whether the Philippines has the ability and the willingness to export significantly higher quantities of that material remains to be seen. We think they won’t be able to come anywhere close to that.

The only other place where you see large higher grade laterite resources is in places like New Caledonia, but that’s committed to local plants or they have long-term joint venture agreements with facilities located in Japan and Korea. Further down the list of potential alternative sources of ore to the Chinese NPI industry include places like Cuba or Guatemala, and those locations don’t have the grade or scale of resources compared to Indonesia, but what they do have is much higher transport costs to China.

TMR: What does that all mean to prices?

MS: We think we’re going to see sharply higher nickel prices to force demand in line with available supply. That happened in 2005-2007, where you literally didn’t have enough nickel—prices rose and there was demand destruction. This scenario will encourage development of lower grade saprolite deposits over time. Eventually, the Chinese will be able to use the low-grade material as ore, but because of higher energy and material inputs to that process, it likely puts a $9–10/lb floor on the global nickel price. Making NPI with 1.4% nickel saprolite is not a high-margin business.

TMR: In the past, you have mentioned the Chinese cost to produce nickel in NPI was approximately $6/lb. That is about where the metal is at present. Does that mean that your new “floor” for the metal will be closer to $9/lb once the market reaches equilibrium? What are the arguments against a price increase to that level?

MS: The first of two pushbacks I hear is that alternative sources will be found. I just discussed that. The second argument against a price increase is that they’ll build plants in Indonesia. The plants in China have much more than access to ore. They have ports, access to power and whole industrial networks available to tap into. The Indonesian ore is located in areas with minimal infrastructure, no power and very little skilled labor. Building a plant there will be expensive and slow compared to China. However, some plants will be built. In fact, Royal Nickel Corp has a relationship with Tsingshan, which is the leading stainless steel producer in China. They’ve been considering a plant for many years and they’ve finally started construction this past summer. That’s a sign of the challenges to build a NPI plant in Indonesia.

TMR: How does Royal Nickel Corp.’s (RNX:TSX) project differ from other global nickel projects?

MS: Our flagship project is the Dumont Nickel Project. It has many attractive features for an undeveloped, large nickel project. The first is deposit type. Dumont is a sulfide deposit rather than a laterite deposit. Large, undeveloped nickel sulfide deposits are rare.

Another project differentiator is location—our deposit is located in the province of Québec, which is an excellent jurisdiction in many ways. Notably, permitting is comparatively well defined and clear path. The province provides very competitive rates of $0.045 per kilowatt hour. The project location has all the essential support infrastructure nearby, including highway, railway, water and power. We’re also fortunate to be located in close proximity to a set of communities that have lots of skilled labor available at reasonable rates.

The metallurgy of the Dumont project is straightforward. Upgrading the ore to a concentrate by milling is a relatively simple task. While the deposit is low grade (0.27% nickel), the concentrate that will be produced is 29% nickel. That concentrate can be fed to traditional smelting and refining processes. The concentrate has very few impurities and doesn’t have a lot of byproduct credits; it’s mostly nickel. The concentrate can also be roasted to remove the sulfur. The resulting product from that process can be used by Chinese NPI makers to increase the nickel content of their lateritic ores if that is something they need in the future to keep their operations going.

TMR: The gold standard for nickel deposits is Sudbury. Is Dumont similar to Sudbury?

MS: No, it’s quite different. They’re both sulfide deposits, but Sudbury is mainly massive sulfide ore bodies. The ore contains lots of bright, yellow shiny minerals visible to the naked eye. The Dumont deposit is low-grade and disseminated. Dumont is analogous to many of the large and low-grade copper and gold deposits that have been put into production recently. Following that analogy, 10 years ago if you walked into most gold companies and said, “Most of the world’s gold is going to come from one gram a ton gold mines” or if you walked into most copper companies and said “Most of the world’s copper in 10 years is going to come from 0.3% copper deposits”, you’d be laughed out of the room.

Yet, those deposits are now very profitable mines. That is partly because of higher metals prices, but also because of technology and scale. Royal Nickel is doing for the nickel industry what has already been done by the gold and copper industries—bringing large-reserve and large-scale deposit into production.

TMR: What is the path forward? What does management think about the chances of being acquired compared to building a mine as a standalone company?

MS: Most of Royal Nickel’s management team are ex-Inco Ltd., so we have the experience to put the project into production but have also been through a round of M&A and realize that it is in shareholders’ interest to take the right price if it comes along. At the same time, we have the team to build this project into an operation. We hired our project director before we started our feasibility study. She was involved in the feasibility study and “owns” that study, so when it comes time to build, there will not be a learning curve.

To bolster the finances, we engaged Rothschild two years ago. Initially, we tried to advance the project financing based on the prefeasibility study, but it is more typical in the industry to wait until the full feasibility study is complete. Rothschild has been our project finance advisor through this entire time period. We are advancing the project as though we will bring this into production ourselves.

In terms of financing, the whole project requires approximately $1.2 billion ($1.2B) in capital expenditures, which we believe can be financed through $500-600 million ($500–600M) of project debt, offtake financing and lastly equity capital raises. We’ve been in talks with several Asian mining houses. We have good relationships with a number of companies from our Inco days, and Rothschild has brought several other possibilities to the table.

One option would be to sell 30–45% of the project and bring in a partner to finance their share of the capex. The remaining balance would be financed by a combination of debt, equity and royalty streams.

The other part of the finance package is from Resources Québec, the government of Québec fund. Resources Québec participated in our IPO and provided royalty financing to us. We sold them a 0.8% royalty about 18 months ago and we continue to expect they will be supportive going forward.

TMR: Where are you on the project timeline?

MS: The feasibility study was completed in mid-2013. The permits should all be in place by the middle of 2014. Contingent on financing, we will be ready to start construction before the end of 2104.

This is a good place to note that Québec is a mining-friendly province. Permitting in Québec is faster and lower risk than most other locations in North America. For example, in many U.S. jurisdictions, timely permitting is a big risk, many projects have taken as much or more than seven years in permitting. By comparison, Québec has permitted half a dozen mines in the last five years, and many of those mines are similar in capex and scale to Dumont.

TMR: What do you say to skeptics of a deposit with 0.27% nickel grade and 45% recoveries? Without any context, those look like tough numbers.

MS: That is pushback that we have heard in the past, and it is easy to address. Take a step back and look at the revenue per ton of ore mined. On that basis, Dumont compares favorably to several base metal deposits that were all acquired.

TMR: What are the three things that you want to get across to an investor interested in nickel and/or your company?

MS: My first point to get across to investors is that nickel in early 2014 is one of the best “long” metals trades in the last 15 years. I’ve been in the commodities sector since 2000. During that time, there have been five great commodity metal trades. Palladium is one. In the late 1990s and early 2000s, Russian supply disruptions boosted prices. Another was nickel. In 2002-2004, nickel prices went up from $2-8/lb, followed by a rally from $5-25/lb again in 2005-2007. A third was copper. Around the same time (2005-2006), everybody thought there was a million tons of copper concentrate supply coming on-line that year. Inventories got down to 60,000 tons globally on all three exchanges. Prices had stalled out at $1.50/lb, but within nine months prices shot up to $4/lb. The next was pretty much any metal that saw prices rally from 2005-2007, which was attributed to Chinese impact on the market.

The molybdenum situation from 2004-2007 is the most analogous to the current nickel market. During this period, molybdenum went from $5/lb to approximately $30/lb and stayed there for four years. At the time, many analysts of the molybdenum market ascribed the market behavior to demand and lack of substitution. Fundamentally, the real driver was a Chinese province that produced about a third of Chinese mine supply started shutting mines down for safety and environmental reasons. That took a third of Chinese supply, or about 7% of world supply, out of the market. That was enough to push the market from $5-30/lb for four years. Compare those numbers to the implications of the Indonesian ore shipment ban. About 25% of world supply of nickel went offline in January 2014. That’s the equivalent of all of the OPEC Gulf States stopping oil exports.

Another analogy would be Chile stopping copper exports overnight. Chile has just over 30% of world copper production. The importance of the Indonesian announcement does not seem to be appreciated by the investment community.

The second investor takeaway is that there are very few advanced base metals projects that have completed a feasibility study. When the development cycle turns and acquiring companies need a new base metal project, they’re going to find a very small pipeline of projects that will meet their needs. The Dumont project is one of the few base metal projects (not just nickel projects) that’s ready to go.

The third takeaway is the standout project specifics of Dumont. We are not in a remote, high altitude region needing a couple of billion dollars of infrastructure. We have all the infrastructure in place. We can build a 50,000/ton per day mine/mill now for $1.2B, which will generate $300-400M in EBITDA annually. There are very few base metals projects of that scale. It’s the third-largest nickel reserve in the world. It will be the fifth-largest nickel sulfide mine. There’s a billion tons of reserve, a billion tons of resource and there’s still a massive amount of exploration potential. The capital markets will turn for the better and we’ve got one of the few projects that’s in a position to be able to take advantage of it. Recent news like the announcements from Indonesia, once fully recognized by the market, will potentially reinforce the trend toward higher metals prices, a trend we expect to develop over the next few years.

TMR: Thanks for speaking with us, it has been interesting.

MS: It has been a pleasure.

Mark Selby is senior vice president of business development at Royal Nickel Corp. Selby has over 20 years of experience in finance and corporate development at various companies, including Quadra Mining, Inco and Purolator Courier. Most recently, Selby served as vice president, business planning & market research, at Quadra Mining.

Readers interested in learning more about the global supply/demand dynamics of the nickel market in light of the Indonesian ore ban should look to the presentation sectionof the Royal Nickel Corp. website for additional information and analysis.

Want to read more Mining Report interviews like this? Sign up for our free e-newsletter, and you’ll learn when new articles have been published. To see a list of recent interviews with industry analysts and commentators, visit our Streetwise Interviews page.

DISCLOSURE:

1) Kevin Michael Grace conducted this interview for The Mining Report and provides services to The Mining Report as an independent contractor. He or his family own shares of the following companies mentioned in this interview: None.

2) Royal Nickel Corp. paid The Mining Report to conduct, produce and distribute the interview.

3) Royal Nickel Corp. had final approval of the content and is wholly responsible for the validity of the statements. Opinions expressed are the opinions of Royal Nickel Corp. and not Streetwise Reports or The Mining Report or its officers.

4) The interview does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legaldisclaimer.

5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned and may make purchases and/or sales of those securities in the open market or otherwise.

Streetwise – The Gold Report is Copyright © 2014 by Streetwise Reports LLC. All rights are reserved. Streetwise Reports LLC hereby grants an unrestricted license to use or disseminate this copyrighted material (i) only in whole (and always including this disclaimer), but (ii) never in part.

Streetwise Reports LLC does not guarantee the accuracy or thoroughness of the information reported.

Streetwise Reports LLC receives a fee from companies that are listed on the home page in the In This Issue section. Their sponsor pages may be considered advertising for the purposes of 18 U.S.C. 1734.

Participating companies provide the logos used in The Gold Report. These logos are trademarks and are the property of the individual companies.

101 Second St., Suite 110

Petaluma, CA 94952

Tel.: (707) 981-8999

Fax: (707) 981-8998

Email: [email protected]

China Demand Helps Push Gold to 2-Week High

Those who trade gold pushed the price of the precious metal to its highest level in two weeks on Feb. 10, and the demand of Chinese buyers was a major factor that was cited as helping the commodity enjoy this gain.

Some market experts also noted the lackluster state of the recent jobs reports released by the U.S. Department of Labor. The data issued by this government agency indicated that in January, American employers created a net 113,000 positions. These figures were released after December failed to create a significant number of jobs in the nation.

The recent support that Chinese consumers have provided to the gold market after returning from the New Year holiday may be part of a broader trend, according to Bloomberg. Data provided by the China Gold Association revealed that last year, there was a 41 percent spike in the nation’s demand for the precious metal.

China’s demand for gold strong in 2013

The CGA stated that in 2013, there was a 57 percent surge in the total weight of gold bars purchased by the nation’s consumers, The Wall Street Journal reported. During the year, people in China bought 375.7 tons worth of these items.

“This was a large magnitude of increase for gold bars, and it might show the Chinese people’s strong desire for gold as an investment,” Hu Yanyan, gold analyst for Everbright Futures, told the news source.

In addition, consumers in the world’s second-largest economy purchased 716.5 tons worth of gold jewelry, which was 43 percent more than in 2012, according to the media outlet. These people continued the trend of more robust gold consumption when they recently stepped up their purchases after returning from the recent holiday, which lasted a week, Bloomberg reported.

This resurgence was noted by Abhishek Chinchalkar, who works for Mumbai-based AnandRathi Commodities Ltd. As an analyst, told the news source. He said that these individuals helped ensure that the price of gold would not decline below a certain level. As the precious metal has had low values lately, many analysts have predicted that many Chinese consumers will have a strong desire for the commodity.

“The U.S. dollar is likely to rise more this year, which means that gold prices will keep falling,” Ms. Hu, who works for Everbright, told the news source.

While the demand of people in China is one major factor that market experts have cited as helping gold prices to rise to a two-week high on Feb. 10, the future testimony of Janet Yellen, chair of the Federal Reserve, was noted as contributing to this appreciation. Chinchalkar told Bloomberg that the statements made by her when meeting with Washington lawmakers starting on Feb. 11 would be crucial.

Yellen testimony could be key

The guidance that Yellen gives to Congress could provide crucial insight on her view of quantitative easing. She persistently supported the use of robust stimulus in the past. These bond purchases have repeatedly been identified as having an impact on the price of gold, so her approach to this form of stimulus could have a substantial impact.

Yellen assumed her role earlier this month, and before she was sworn in, the Federal Open Market Committee announced specific plans to taper after two separate meetings. The central bank had been purchasing $85 billion of debt-based securities every month, but the Fed announced in December that in the following month, this figure would be lowered to $75 billion per month. In February, the pace was lowered to $65 billion per month.

The Fed has increased its balance sheet to more than $4 trillion over the last several years. These bond purchases, and also those made by central banks across the world, have contributed significantly to the size of the global money supply. Amid this robust stimulus, some have voiced concerns about potential inflationary pressures.

These worries have driven many global market participants to seek out gold as a hedge against the risk that the price level will increase significantly. As a result, the pace at which the Fed buys bonds going forward could have an impact on the inflation concerns of global market participants.

Economic data and tapering

Some market experts have predicted that the Fed will not be able to rapidly dial down its bond purchases due to the weak nature of the economic data provided for the U.S., according to BullionVault. For example, major financial services firm UBS has stated that the global asset market values cannot be priced as they would if tapering was anticipated to happen at a more accelerated rate, due to the lackluster reports recently provided by the Labor Department.

Lowering these bond purchases too quickly could result in the removal of key support that has been helping the labor market mend. However, using a more conservative timeline for lowering this stimulus could motivate those who trade gold to sell it.

The post China Demand Helps Push Gold to 2-Week High appeared first on | HY Markets Official blog.

Article provided by HY Markets Forex Blog