By CentralBankNews.info

Angola’s central bank maintained its policy rate, the BNA rate, at 9.25 percent, and the rate on its Standing Lending Facility Liquidity at 10.25 percent, but raised the Liquidity Absorption rate by 50 basis points to 1.25 percent from 0.75 percent.

The National Bank of Angola (BNA), which last month maintained its BNA rate but cut the reserve requirement on local currency deposits to 12.5 percent from 15.0 percent, did not provide any reason for the increased liquidity absorption rate apart from saying its monetary policy committee had based the decision on an analysis on the country’s economy based on January data.

In January Angola’s inflation rate rose to 7.84 percent from 7.69 percent in December, but it was still well below the 10 percent that the central bank has long targeted. The last time Angola’s inflation rate topped 10 percent was in July 2012 at 10.02 percent and since then inflation has trended lower.

The central bank, which cut its rates by 100 basis points in 2013, said the LUIBOR overnight rate was at 4.15 percent while maturities of 3 and 12 months were 7.49 percent and 9.42 percent, respectively.

Credit to the country’s economy grew by 1.62 percent in January to a stock of 2,975,840 million kwanza, with the national currency component up by 2.4 percent and the foreign currency component up by 0.28 percent.

The central bank said the kwanza’s exchange rate was stable in January, with an average exchange rate of 97.86 against the U.S. dollar. A total of US$ 3.031 billion was traded in the foreign exchange market, of which $1.636 billion was traded in the primary market and the rest in the secondary.

In 2013 the kwanza depreciated by only 1.8 percent against the dollar and has remained stable so far this year, trading at 97.60 to the dollar today compared with 97.61 at the end of 2013.

Angola’s Gross Domestic Product rose by 7.4 percent in 2013, up from 2012’s 5.2 percent growth.

A Pair of Top Picks, a Risky Pair and an Ace in the Hole: Justin Anderson Shows His Hand

Source: Tom Armistead of The Energy Report (2/27/14)

http://www.theenergyreport.com/pub/na/paul-renken-for-2014-gains-look-to-uranium-pgms-and-gems

Since its inception in 2007, the Salman Partners’ Top Pick Index has made a 251% return. The index is a huge pot for investors in the international oil and gas space to bet on, but it’s not for the untutored. Salman Partners Analyst Justin Anderson walked The Energy Report through the risks and returns of the game. Find out how he plays his hand.

The Energy Report: Justin, welcome. Tell us about Salman Partners Top Pick Index. Why was it established?

Justin Anderson: Top Pick Index was established to contrast the performance of our company’s favorite investment ideas against a Canadian benchmark of general stocks and to see how those investment ideas performed. Analysts look at the stocks under their coverage and then they try to pick one or two stocks that they think are going to be the best performers in that group over the next 12 months.

TER: What’s the track record? Do Top Picks generally perform as advertised?

JA: So far it’s been a really good track record. Since inception in 2007, the Top Pick Index of Salman Partners has had a 251% return versus the benchmark index, which has returned 30%. Over the last two years, the Top Pick portfolio has returned 38% versus 21% in the general S&P Index.

TER: Canacol Energy Ltd. (CNE:TSX) just earned the Top Pick recommendation in December. How did that happen?

JA: Over the last half of last year, Canacol was increasingly interesting for us, especially when it made a discovery called Labrador in the Llanos Basin of Colombia. That was an important discovery, not just for the intrinsic value of the discovery itself and the potential long-term cash flow that it would add to the company, but also because it meant that Canacol was going to be able to get to the finish line with respect to some of its other assets. What I mean by getting to the finish line is that Canacol has built up a very impressive Middle Magdalena basin unconventional position, very sensitive to time and funding. This conventional discovery at Labrador unlocked some less noticeable value in its Middle Magdalena position. That got us very interested. Then, when it made an additional discovery in the Llanos Basin called Leono, that discovery by itself looked really good, but the compounding benefit to the rest of the portfolio was very strong, so we upped it to a Top Pick.

TER: What are the most exciting positives about Canacol?

JA: To use a baseball analogy, I think Canacol is not really looking for the solid base hit. It’s looking to hit a home run. This company really wants to go big. That’s exciting, when you have a management team that is aggressively looking to make a multiple big return for its shareholders. The reason it’s in that position, as I said, is that it built up this large unconventional position in Colombia. It’s a position that, in terms of acreage, is second only to Ecopetrol SA (ECP:TSX; EC:NYSE), the national oil company there. Should the unconventional Colombia space ever take off, look out. This is a company that will perform extremely well if that happens.

TER: What’s the biggest concern?

JA: I think it’s the other edge of the same sword. If the unconventional Colombian space never does take off, if some of the initial well results are not that great, then you could get in a situation where that acreage becomes less important overall. I think that’s actually the biggest risk to the company as well. The nice thing about Canacol is that it has a very robust conventional portfolio that gives you a lot more downside protection in that scenario than some other companies that may be so exposed.

TER: South America is not the most stable operating environment. What are the political and security conditions in Canacol’s main operational areas of Colombia and Ecuador?

JA: For Canacol, I think the main issue is in its heavy oil portfolio. That’s in the center of Colombia; it has a bunch of heavy oil blocks. Those blocks are very close to some previous FARC strongholds, FARC being the organization that has been agitating through violence in the country to cause a communist revolution. Because of that proximity, people have been dissuaded from ramping up development activity in the area. It has affected Canacol’s heavy oil exploration appraisal work. I think that’s the biggest risk that it’s exposed to. On the plus side, I don’t think stockholders really care about its heavy oil position at this point, and it’s of tertiary concern to the market.

TER: What about Ecuador?

JA: Ecuador is much more of a basket case than Colombia. Ecuador is problematic because it’s not just lingering terrorist groups; the government itself is the issue. That being said, the contract Canacol signed with the government of Ecuador is one that provides much lower netbacks. It is a direct service agreement with the government. It’s an isolated issue for the company; I don’t really see any risk there.

TER: You created an unconventional portfolio for the Middle Magdalena unconventional play. Why?

JA: Unconventional positions, especially in the international locations, are extremely sensitive to initial results. You might have a very large position, but the fracking response, the geology and the capex/opex of the initial wells are going to have a major impact on the long-term development of the play—then slap political risk on top of that. We wanted to look at unconventionals in a unique way, rather than value all of that acreage in one blow. We built a stochastic or Monte Carlo model to try to capture the range of scenarios that those sensitive initial conditions could provide. That’s why we set up this separate unconventional portfolio. The effect that you get is a much more tailing effect: Either things go very poorly and you get no value or things go extremely well and you get a huge amount of value. There isn’t really much of a middle ground for these emerging unconventional plays.

TER: Why was it necessary to separate the unconventional portfolio from the other parts of your portfolio?

JA: A conventional prospect is more independent. If you have five conventional blocks, it makes sense to value them separately and then aggregate the results of those valuations, whereas with an unconventional position, you might have the same five blocks, but in this case they’re either all going to work or none of them will work. It’s much more common to see significant correlations between the successes or the failures, as opposed to a conventional portfolio, where it’s completely normal for, say, two of the five blocks to work out.

TER: Outside North America, shale development has an uneven record. Why is Canacol’s holding of 545,000 net acres of Colombian shale a positive thing?

JA: If you asked people in North America 10 years ago what would be the status of the Eagle Ford or the Montney or the Bakken, I think people would probably have been very skeptical about how those plays would perform. Ten years later, we’re seeing massive growth in these resource plays. There’s absolutely no reason why some of the best quality resources around the world won’t see the same kind of activity that those plays have seen. We’ve seen it in North America first simply because we’ve got the most stable political environment, but the rocks are the same around the world and you’re going to see the same booms in other countries.

The question simply becomes, where are we going to see the next boom? The answer to that question is, you’ve got to have great-quality rocks. We see some of that in Colombia. We see some of that in Argentina. We see some of that in places in Africa, India and China. Then the next question you have to ask is, considering those most prospective areas, where is the most likely place to see near-term capital flows? That’s really a political question. In this department, Colombia actually shines for its relative stability. Combine quality rocks with good political environment, and Colombia starts to look pretty attractive. Obviously there’s still a lot of uncertainty as to which way the tail will go in this one, but I think it’s a pretty good speculative bet.

TER: One of the problems that has affected the viability of shale oil and gas outside the U.S. is that the quality of the rocks is different in new areas, like Poland, for example, than what they were anticipating.

JA: It depends on the location. I would argue that the best rocks in the world for unconventionals outside of North America are probably in Argentina, in the Vaca Muerta. That is an extremely high-quality resource. I would say that Colombia is comparable in quality to Argentina and the Eagle Ford. It’s not as big, but the quality’s likely there. Arguably the quality is actually a more important factor for early-stage development than quantity alone.

TER: Is Canacol management looking for a buyout?

JA: I think they’re open to it. One of the great things about Canacol is its management is very down to earth. They’re there to return money to shareholders, as opposed to some companies where we see them establishing a corporate kingdom. Canacol is focused on shareholder value. If a company comes in that offers that, I think they would go for it.

TER: Parex Resources Inc. (PXT:TSX.V) is another Top Pick. Why?

JA: Parex is an interesting company. It’s a company that has a very undervalued production stream. It’s trading at multiples far below comparable companies in Canada and the U.S. Nearly all of its acreage is in the Llanos Basin of Colombia. The Llanos Basin is known for high decline rates, quick payout times and light oil.

What happens is, investors are very focused on the near-term reserve number, and they do the calculation against production and say, oh, this is a short reserve life. Then they apply a significant multiple discount to the company. The problem is you can’t just look at the reserves; in some cases you have to look at acreage as well. Parex has enough acreage where reserve adds are a foregone conclusion. It has built up such a robust position of acreage that it is going to book new reserves in the future.

Not all exploration acreage is equal. This company is sitting on exploration acreage that will become reserves. I think the market is not giving it any value for that when in fact it should be. That’s the source of the opportunity with Parex, where the actual reserves in the future will be much more than the current reserves, but you’re only paying depressed current reserve multiples to get access to the stock.

TER: The Parex stock has trended up since July of last year. You recently reiterated your Top Pick recommendation and raised your target from CA$9.30 to CA$10/share. What is the driver here?

JA: The strategy’s working. We got really excited about this name mid-2013, when Parex had some drilling success, started to diversify its portfolio and also made some acquisitions to expand its acreage running room. All of this put the company in a position to apply its operational expertise to these different plays and take advantage of that.

What we’ve been seeing over the course of the last nine months is the company executing on the strategy, adding reserves. We just saw a great reserve number recently. The stock has climbed. That’s being partially driven by reserve adds that the market seemed surprised to see.

TER: Parex is indexing its oil price to Brent instead of to West Texas Intermediate. What’s the significance of that?

JA: It probably just underscores even further the ridiculousness of the low multiple that it’s trading at because its production is more valuable than a lot of the Canadian domestic production, which is getting more depressed realized prices. When you look at the production multiples you just say, how is this possible when the company’s selling its crude to Brent prices? It just exaggerates the opportunity that much more.

TER: Africa Oil Corp. (AOI:TSX.V) is not a Top Pick; it’s a Hold. Is that because of the risky neighborhood it’s in?

JA: There are two major issues there. One overriding issue is, will it see development anytime soon of some of the impressive discoveries that it has made over there? Africa Oil is not far from Uganda, where there have been significant discoveries that no one has been able to monetize, and Africa Oil’s nearby discoveries are newer. Yes, the company is in Kenya. It’s a little bit closer to the market, but at this point, there’s still not as much oil discovered there as in Uganda. It is earlier stage. It’s going to take more time to appraise it. There’s still a lot of risk that it won’t find enough oil there to justify a major development and pipeline project.

The other issue is, it’s a really exciting stock. Africa Oil has done some incredible things in terms of exploration. Unfortunately, an analyst doesn’t necessarily look at how well the company is performing. We look at how we think it will perform in the future relative to the expectations, which are reflected in the stock price. From that perspective, I see a company that could go one of two ways: It’s either going to perform very well if it’s able to make some more discoveries, perhaps extend the trend a little further north and find well over a billion barrels in that basin. Alternatively, if it’s unable to open up any other basins in the area and there’s a risk of stranded oil discoveries, then the stock could get killed. A buyer of the stock is going to go one of those two ways, big upside or big downside. The question then becomes, what price are you willing to pay? The current price just doesn’t give me a compelling reason to say it’s a good bet.

TER: When do you think you’ll have a clearer picture of its prospects?

JA: I think it’s going to be over the next six months. It’s doing a ton of drilling this year, which is exciting, both in the Lokichar, where it’s had its discoveries, and outside the basin. I think the Lokichar wells are far less important than the wells outside the basin. It’s drilling on Block 9, for example, in a different basin. It’s drilling north of its discoveries and it’s also doing some work in Ethiopia. If any one of those three other play concepts that it’s tinkering around with turns out to be successful, then it’ll be an excellent story. We should know that in the next six months, but I think that all three of those other plays are very risky. Investors are taking on a big risk. If all three do not work then you could be in a tough situation with the stock.

TER: Mart Resources Inc. (MMT:TSX.V) is another hold and also another African operator. What’s the status of its Umugini pipeline?

JA: It’s under construction. It’s been unfortunately delayed by forces beyond the company’s control. Estimates are that it should be completed midyear 2014.

TER: How will the pipeline’s completion benefit Mart’s stock price?

JA: I think people appreciate that the company needs the pipeline to make the operation more robust. That is probably reflected in the stock. I don’t actually see a huge potential from the pipeline completion alone. I think the more important thing will be production. If everything goes perfectly, the pipeline gets commissioned, production goes past 20,000 barrels/day through the line and the losses are cut to under 10% or 5%, that would be a positive thing for the stock, there’s no question. It’s certainly a possible scenario. The greatest concern for me is how much capacity is behind the pipe. How much can Mart ramp up production once the pipeline is installed?

Talking to investors who hold the stock, I think there are a lot of high expectations for how much capacity is behind the pipe. If you compare that to the reserve numbers, I’m a little skeptical over how much it will be able to push through there. The other issue I have is regarding the Pioneer tax status that has come to an end for the company. It started this year. Once it chews through all the tax credits, that will start to affect the cash flows in a material way as well.

TER: How will Mart ensure the Umugini pipeline will be more secure than the one it’s using now?

JA: It will have to do the same things it’s doing now, trying to make agreements with the government about the losses. It is encouraging see recent news that it’s talking to the government and establishing a committee to review the losses. Just having two export options will be a good thing for the company. That, more than specific details of what it’s going to do to protect the pipeline, is important.

TER: You have a lot more companies than those four under coverage. What are you really excited about right now?

JA: The other one to highlight would be Gran Tierra Energy Inc. (GTE:TSX; GTE:NYSE.MKT). It has been our Top Pick for a long time. Just recently, we rated it a Buy only because we felt Parex and Canacol were even more compelling stories, but Gran Tierra remains a very exciting story. It’s made major discoveries in Peru and it’s a long-term, value-player’s dream because it’s getting a very cheap multiple on its reserves right now and has a lot of extra-exciting exploration in Peru.

TER: Justin, you’ve given us a lot to think about. I appreciate your time.

JA: Thank you.

Justin Anderson joined Salman Partners in December 2011 as an oil and gas investment analyst. He is the founder of the research company Xedge, which specialized in rigorous stochastic analysis of oil and gas exploration portfolios. Previously, he worked for the investment banking energy group at BMO Capital Markets, after having worked on energy company strategy and valuations at McKinsey & Co. Anderson completed a Bachelor of Science in mechanical engineering and a Bachelor of Science in Russian studies at the University of Calgary. He then completed a Master of Science in aeronautical engineering at MIT, with his research and thesis focus on energy economics. While at MIT, Justin founded and commercialized a high-tech company called Waybe and was an executive chair of the MIT Energy Club.

Want to read more Energy Report interviews like this? Sign up for our free e-newsletter, and you’ll learn when new articles have been published. To see a list of recent interviews with industry analysts and commentators, visit our Interviews page.

DISCLOSURE:

1) Tom Armistead conducted this interview for The Energy Report and provides services to The Energy Report as an independent contractor. He or his family owns shares of the following companies mentioned in this interview: None.

2) The following companies mentioned in the interview are sponsors of The Energy Report: Mart Resources Inc. Streetwise Reports does not accept stock in exchange for its services or as sponsorship payment.

3) Justin Anderson: I or my family own shares of the following companies mentioned in this interview: Canacol Energy Ltd. I personally am or my family is paid by the following companies mentioned in this interview: None. My company has a financial relationship with the following companies mentioned in this interview: We seek to do business with all of the companies mentioned (other than Ecopetrol) but have never done any business with them in the past. I was not paid by Streetwise Reports for participating in this interview. Comments and opinions expressed are my own comments and opinions. I had the opportunity to review the interview for accuracy as of the date of the interview and am responsible for the content of the interview.

4) Interviews are edited for clarity. Streetwise Reports does not make editorial comments or change experts’ statements without their consent.

5) The interview does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer.

6) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned and may make purchases and/or sales of those securities in the open market or otherwise.

Streetwise – The Energy Report is Copyright © 2014 by Streetwise Reports LLC. All rights are reserved. Streetwise Reports LLC hereby grants an unrestricted license to use or disseminate this copyrighted material (i) only in whole (and always including this disclaimer), but (ii) never in part.

Streetwise Reports LLC does not guarantee the accuracy or thoroughness of the information reported.

Streetwise Reports LLC receives a fee from companies that are listed on the home page in the In This Issue section. Their sponsor pages may be considered advertising for the purposes of 18 U.S.C. 1734.

Participating companies provide the logos used in The Energy Report. These logos are trademarks and are the property of the individual companies.

101 Second St., Suite 110

Petaluma, CA 94952

Tel.: (707) 981-8204

Fax: (707) 981-8998

Email: [email protected]

Stocks In Europe Trades Mixed

Stocks in Europe were seen trading mixed on Friday while traders focus on macro-data from European Union countries.

The European Euro Stoxx gained 0.02% to 3,140.00, while the German DAX index added 0.34% to 9,621.00 at the time of writing.

At the same time the French benchmark CAC 40 edged 0.10% higher at 4,400.80, while UK’s benchmark FTSE 100 lost 0.4% to 6,807.50.

Stocks in the Asian region were trading mixed on the last day of the trading week as Japan’s stocks were dragged lower by the government’s month-end data.

The German drug-makers Bayer added 0.9%, while its net income rose from 2.403 billion euros in 2012 to 3,189 billion euros in 2013.

British bookmaker William Hill confirmed its net income climbed 16% to £1.486 billion in the last 12 months, from £1.276 billion added in the previous year.

Stocks – Janet Yellen’s Testimony

The new Federal Reserve (Fed) Chair Janet Yellen delivered her testimony on monetary policy before the Senate Banking Committee as part of the Fed’s semi-annual policy report known as Humphrey Hawkins on Thursday. During the Q&A session Yellen said the US economy’s growth slowed down since her last testimony.

Yellen also said the string of data recently released, has been weal and were due to the extreme cold weather in the US.

The US Federal Reserve reduced its monthly bond purchases by $10 billion at each of its two meetings, leaving its monthly stimulus at $65 billion. The yellow metal surged 70% from December 2008 to June 2011 as the central bank added over $4 trillion into the financial system to boost growth.

Other News

In Germany, the country’s retail sales rose 2.5% higher in January, compared to 2.1% recorded in the previous month.

While in Switzerland, the Swiss Barometer increased to 2.03, rising above forecasts of 2 in February, according to reports from KOF Leading Economic Indicators.

The Statistical Office of the European Union (Eurostat) is expected to release the Consumer Price Index (CPI) data later in the day.

Visit www.hymarkets.com to find out more about our products and start trading today with only $50 using the latest trading technology today

The post Stocks In Europe Trades Mixed appeared first on | HY Markets Official blog.

Article provided by HY Markets Forex Blog

Yen Boosted By Upbeat Industrial Production Data

The Japanese yen strengthened against the US dollar on the last day of the trading week. The yen was supported by the upbeat industrial production data in January.

The yen gained 0.44% against the US dollar, trading at 101.65 yen at the time of writing.

The nation’s currency eased 13% against the greenback since April 4 2013, when Japan’s central bank introduced the stimulus program of bond purchases to boost the monetary base to 279 trillion yen by the end of 2014 to achieve the inflation target of 2%.

Yen – Japan Industrial Production

Japan’s industrial output climbed higher than expected, rising 4.0% higher in January, compared to analysts forecast of a 3.1% rise in output, data from the Ministry of Economy, Trade and Industry (METI) confirmed.

Other Data’s released by the METI showed that retail sales for the previous month climbed by 1.4% month-on-month, rising above analysts forecast of a 1.3% rise.

The unemployment remained at a five-and-a-half year low of 3.7 in January.

Japan Consumer Prices

Consumer prices in Japan continued to climb in January, while household expenditure surpassed estimates. The core Consumer Price Index (CPI), climbed at a steady pace of 1.3% year-on-year in January.

Janet Yellen’s Testimony

The new Federal Reserve (Fed) Chair Janet Yellen delivered her testimony on monetary policy before the Senate Banking Committee as part of the Fed’s semi-annual policy report known as Humphrey Hawkins on Thursday. During the Q&A session Yellen said the US economy’s growth slowed down since her last testimony.

Yellen also said the string of data recently released, has been weal and were due to the extreme cold weather in the US.

The US Federal Reserve reduced its monthly bond purchases by $10 billion at each of its two meetings, leaving its monthly stimulus at $65 billion. The yellow metal surged 70% from December 2008 to June 2011 as the central bank added over $4 trillion into the financial system to boost growth.

Visit www.hymarkets.com to find out more about our products and start trading today with only $50 using the latest trading technology today

The post Yen Boosted By Upbeat Industrial Production Data appeared first on | HY Markets Official blog.

Article provided by HY Markets Forex Blog

Fibonacci Retracements Analysis 28.02.2014 (EUR/USD, USD/CHF)

Article By RoboForex.com

Analysis for February 28th, 2014

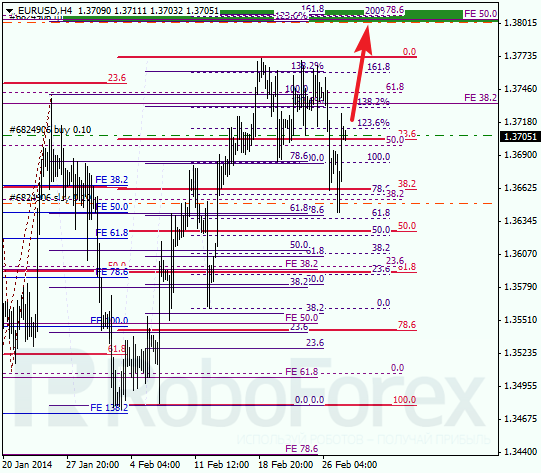

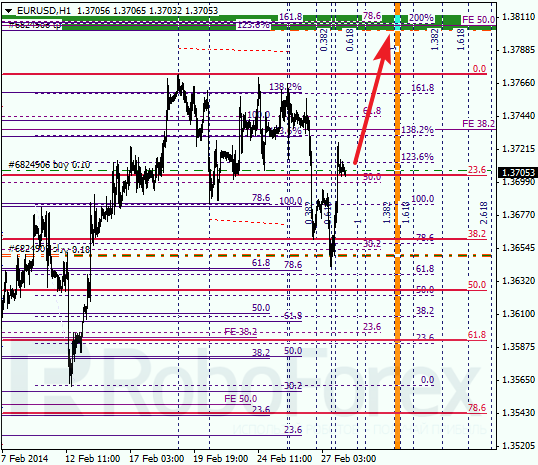

EUR USD, “Euro vs US Dollar”

Eurodollar rebounded from local level of 38.2% and started moving upwards. During correction, I opened another buy order. Target is still near several upper fibo-levels at 1.3800.

According to analysis of temporary fibo-zones at H1 chart, upper levels may be reached in the beginning of the next week. Possibly, after reaching them, price may start new and more serious correction.

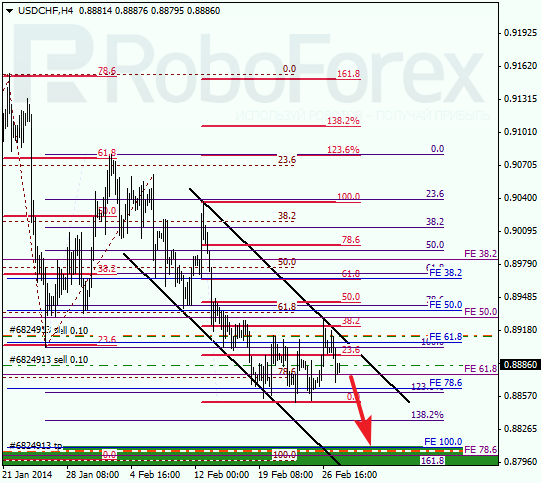

USD CHF, “US Dollar vs Swiss Franc”

Just as we expected, Franc rebounded from local level of 38.2% and upper border of descending channel. During correction, I opened one more sell order. Lower levels may be reached in the nearest future.

At H1 chart we can see, that price made a reverse right inside temporary fibo-zone. Possibly, pair may start reach new minimum on Friday. In this case, I’ll move stops into the black.

RoboForex Analytical Department

Article By RoboForex.com

Attention!

Forecasts presented in this section only reflect the author’s private opinion and should not be considered as guidance for trading. RoboForex LP bears no responsibility for trading results based on trading recommendations described in these analytical reviews.

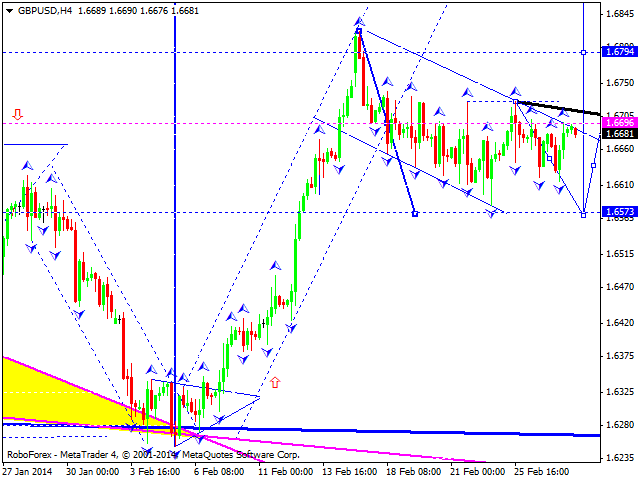

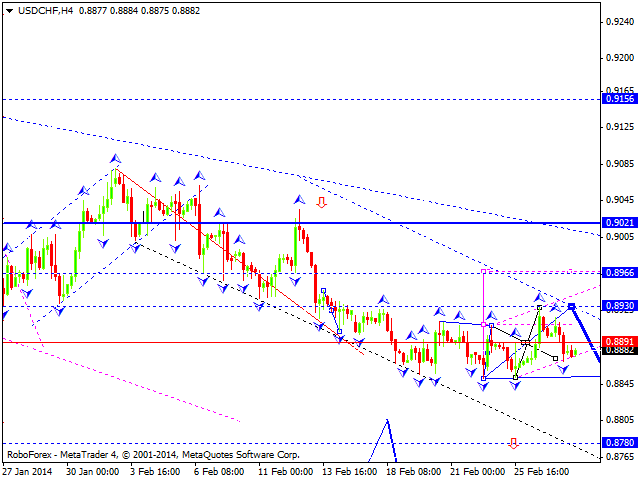

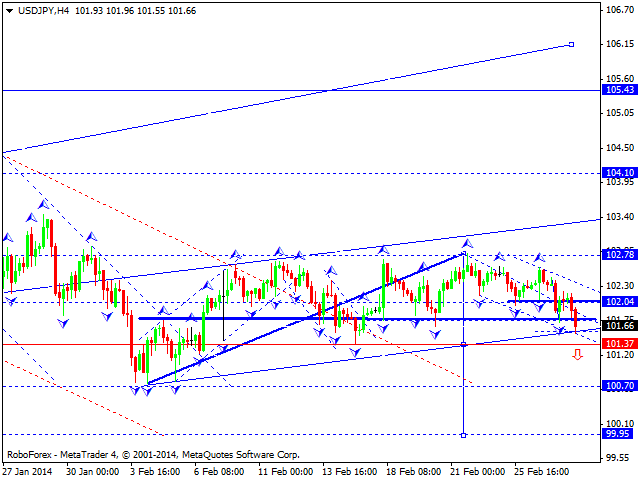

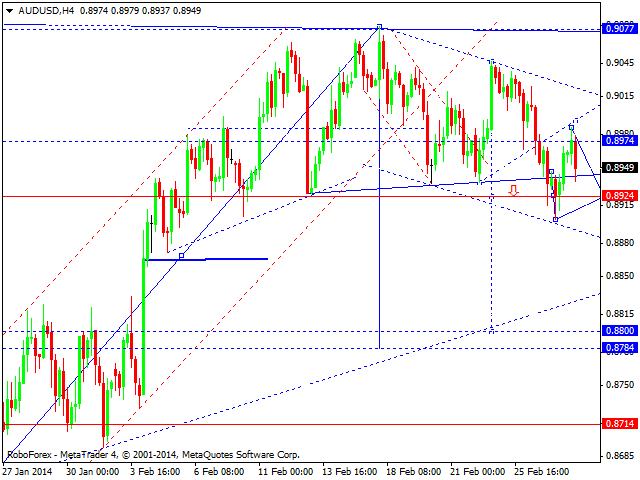

Forex Technical Analysis 28.02.2014 (EUR/USD, GBP/USD, USD/CHF, USD/JPY, AUD/USD, GOLD)

Article By RoboForex.com

Analysis for February 28th, 2014

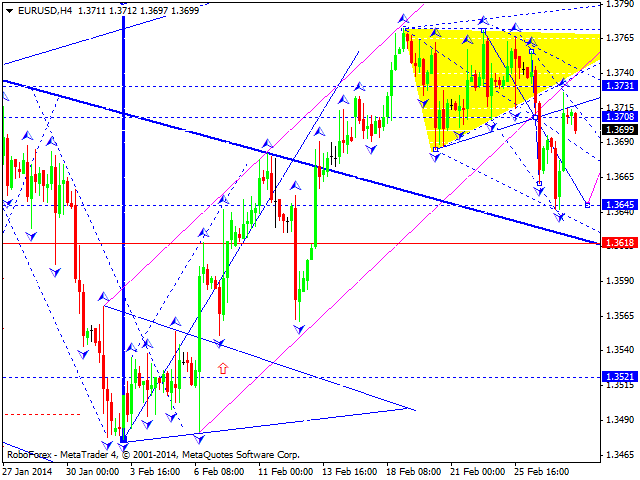

EUR USD, “Euro vs US Dollar”

Euro formed the third structure of descending wave, which may be considered as correction. We think, today price may form another descending structure to reach minimum of this wave and then continue moving upwards to reach target at level of 1.3900.

GBP USD, “Great Britain Pound vs US Dollar”

Pound is still forming consolidation channel; market may yet continue moving downwards. We think, today price may move downwards to reach level of 1.6575 and then continue growing up towards level of 1.7000.

USD CHF, “US Dollar vs Swiss Franc”

Franc completed another structure of the third ascending wave. We think, today price may form one more ascending structure to reach level of 0.8930 and then continue falling down towards level of 0.8730.

USD JPY, “US Dollar vs Japanese Yen”

Yen couldn’t continue its ascending movement towards level of 103.30 and right now is moving downwards. We think, today price may break its consolidation channel downwards and then continue falling down towards level of 100.00. Later, in our opinion, instrument may reverse and start growing up to return to level of 102.80.

AUD USD, “Australian Dollar vs US Dollar”

Australian Dollar completed the third descending weave and corrected it. We think, today price may form another descending structure to reach level of 0.8870, consolidate for a while, and then continue moving inside descending trend towards level of 0.8400.

XAU USD, “Gold vs US Dollar”

Gold completed the first descending impulse and right now is correcting it. We think, today price may return to level of 1336, form another descending structure towards level of 1303, and then return to level of 1320. Later, in our opinion, instrument may form the fourth correctional wave with target at level of 1285.

RoboForex Analytical Department

Article By RoboForex.com

Attention!

Forecasts presented in this section only reflect the author’s private opinion and should not be considered as guidance for trading. RoboForex LP bears no responsibility for trading results based on trading recommendations described in these analytical reviews.

Why Myer Still Doesn’t Understand the Internet

Roughly calculated, Myer has 66 stores nationwide, using up 792,000 square metres (sqm) of retail space. That’s thirty eight times the fence to fence area of the MCG.

David Jones (DJ), on the other hand only has a 532,000 sqm retail footprint. Roughly 26 times the fence to fence area of the MCG. DJ has 38 stores.

And Bernie Brooks, CEO of Myer, is hell bent on controlling all of this retailing space.

Well that’s if David Jones come back and take up Brookes offer…

The problem is, Brookes is hardly the leader anyone would want controlling this.

He has openly admitted that he chose not to go down the online path when the opportunity presented itself.

As he told LeadingCompany last year:

‘I focused on fixing the fundamentals of the business, the supply chain, getting the product to the customer, the IT, the visual merchandise in store and didn’t focus enough on what would be the 2011 – 2013 and the 2011 – 2014 future.

‘I don’t think people realise when you lose $66 million how close you are to actually the alternative of breaking Myer up…‘

When Bernie Brookes took over Myer in 2006, he didn’t even bother to look at setting up an online shop. He was far more interested in, in his words, ‘fixing the serious financial problems‘ at the time:

‘You may recall a lot of Australian retailers expended large amounts of money, particularly in the late 1990′s and early 2000s on those websites and they didn’t come…that premature build frightened them off.

‘They are predominantly owned by shareholders who are looking for immediacy in return, and it means if you spend $50, $60 $70 million worth of capital getting ready for three or four years’ time, they don’t see that as an attractive an investment and something that gives you money today.‘

In other words, when Brooks had the chance to make Myer a retailing leader, he instead took the road that would make him popular with shareholders of the day by giving them immediate returns. Well, sort of.

The point is, rather than build a better business when he had the chance, he travelled the easy road. And that was pandering to what he thought stock holders wanted rather than tackle an issue that would lead to longevity for the company.

The reality is that investors want long term returns. No investor just wants the business they’ve invested in to just think about the next 3–6 months. This is really just an excuse to hide the fact that Myer messed up its online strategy.

Even now Myer heads are still proving they don’t truly understand the modern retail landscape.

According to the Australian, ‘Myer chairman Paul Clintock and CEO Bernie Brooks believe a merged entity can use its bulk to take on the overseas retailers, and perhaps even expand some kind of yet unspecified Myer-David Jones mishmash offshore.‘

The problem with the analysis from the Australian is it suggests that overseas retailers need to be tackled.

But as Tim Dohrmann recently told Australian Small-Cap Investigator subscribers, ‘It’s estimated that the Australia domestic retail industry brought in $225 billion in annual sales in July 2013. Within that, Australia’s online retail market was sized at just $14.1 billion…just 6.3% of all retail sales.‘

And the NAB online retail sales index expands on that further by pointing out that domestic retailers ‘continue to control the largest share of online sales – at around 73%’.

That means $10.2 billion was spent in local online shopping.

For a really clear picture, here’s our Australians spend their money online in 2013.

It appears that Myer is using international web shopping as a scape goat for not lifting their game.

My point is, Brookes and other department store heads have had the opportunity to revolutionise department store retailing in Australia. However instead of being market leaders, they’re playing catch up.

Right now, Myer has the chance to radically challenge and reshape the retail landscape…instead they would rather blame others for their problems. And they could ultimately end up out of business anyway.

The thing is, I doubt the heads of Myer have what it takes to truly grow with the new retailing world Australians are embracing.

Two days ago, the Australian Financial Review commented on how Myer is re-evaluating its ‘strategic’ plan:

‘Myer is reviewing its five point strategic plan ahead of a strategy meeting next week and the release of first half results on March 20.

‘The plan is aimed at luring shoppers to Myer’s online and bricks-and-mortar stores through better service and merchandise.‘

The strategy was established last year. That’s right, as recently as last year folks in the corner office with a view at Myer still thought it could ‘lure’ people back into stores with new floor covering and softer lighting.

But realising this might not work anymore, Brookes has said he has a willingness to invest more in online retailing and decrease spending on store refurbishments.

As an investor, that’s not reassuring. That statement reminds me of the time I dragged myself to school to sit an exam I hadn’t studied for.

Investors want to be part of innovative companies that do things because they believe in it and have a strategy for the future, rather than doing something half-heartedly. Firms willing to take financial risks. Businesses catering for the modern consumer.

And Myer is none of those.

If you push aside these news-dominating retailing big boys, there are some amazing small retailing firms worth investing in. Meanwhile, it’s clear that Myer’s management still doesn’t have a clue.

Shae Smith+

Editor, Money Weekend

Top stories from Money Morning this week…

Did it ever occur to you that the market right now looks like it did in 1985? This week, Kris Sayce told readers he has the same view of the market as legendary 1980′s analyst Paul Tudor Jones. He wasn’t comparing himself to the investing legend. He was simply saying he shares the same view, that even if you think the market could crash at some point, there’s still a lot of ways investors can make money on stocks…if you know where to look.

Electric cars are cool again. There are reports that Apple [NASDAQ:AAPL], the hippest tech leader around, is about to launch into the electric car market. Sam Volkering, editor of Revolutionary Tech Investor and Tech Insider explores what is means when Apple jumps into the electric car market…

And this…

Kris is convinced the Aussie market will reach 15,000 over the next four years. Sound crazy? Hear him out first here…

Most stock traders still don’t ‘get’ this market

The financial worriers are back.

Down goes the Australian stock market – by 0.5%.

And down goes the Australian dollar – by more than a cent against the US dollar since the start of the week.

What’s caused it? A drop in business spending.

The market thinks that’s bad news. But it’s not, it’s good news. Just not in the ‘bad news is good news’ kind of way.

Here, let us explain…

First off, here’s how the Sydney Morning Herald reported the latest news:

‘The Reserve Bank is facing a new headache as a big drop in company spending adds to the evidence that the rest of the Australian economy is struggling to take up the slack from the slowdown in mining.

‘The Australian Bureau of Statistics reported business spending expectations for the three months to December fell by a greater than expected 5.2 per cent.‘

Analysts had expected businesses to forecast spending of $139 billion, while the actual number was $124.9 billion.

You know what that means don’t you? That’s right, interest rates if they move at all, are only going in one direction, down. Yet the market hasn’t figured that out yet.

Currency traders get it, stock traders don’t

In recent weeks the market has fallen for the spin from the Reserve Bank of Australia (RBA). That’s the idea that the interest rate cutting cycle is over.

That’s why the Aussie dollar stopped falling and bounced back two weeks ago. But with the latest business forecast for lower spending, the Aussie dollar is on the way down again.

Why? Because currency traders must reckon interest rates will stay low and perhaps go lower.

That should be good news for stocks. But surprisingly, the Australian stock market fell too.

It’s funny. Because it seems as though stock investors have forgotten all about the impact of low interest rates on stocks. They’ve forgotten that when interest rates are low, it forces investors to look for alternative investments.

The natural beneficiary of this are stocks…in particular dividend-paying stocks.

That’s why it doesn’t make any sense that stock prices would fall. We can only think that most investors have forgotten about the impact that low interest rates have on stocks.

Clearly most investors have short memories.

Now, we’re not saying that dividend stocks will put in the same type of gains that you saw from late 2012 through to 2013. Our bet remains that growth stocks are the best place to put your money in 2014.

But it does suggest that with the Aussie dollar on a downward move again, currency traders have worked out what stock investors have missed.

Recession yes; falling stocks? Maybe not

Of course, as we mentioned earlier this week, the level of the currency doesn’t really matter when it comes to Aussie stock prices.

Looking back over the past 10 years the correlation between the Aussie dollar and Aussie stocks has been minimal at best.

What’s more important is the direction of interest rates. And despite all the recent talk of the end of the interest rate cutting cycle, we’re still sticking to our call that the RBA will cut rates to below 2% before the year is out.

If that happens, it should help boost stock prices over the coming year, pushing them towards our near-range target of 7,000 points. After that, even bigger gains are on the cards.

If that’s not good news we’re not sure what is. But at least the market hasn’t fallen into the ‘bad news is good news’ trap. The market reacted exactly how you’d expect it to react. That tells us the market still isn’t looking far enough into the future, which means it’s still a great opportunity to buy into stocks.

So when the RBA starts making noises about cutting rates or actually goes ahead and cuts them (perhaps as early as next Tuesday), you can expect stocks to put in a good run as growth investors consider the positive impact of lower interest rates, and income investors begin to scout out the best dividend stocks on the market.

Our old buddy Dan Denning says 2014 is the year that the Aussie economy goes into its first recession in 22 years. We won’t argue with that. The one thing we will say is that Aussie stock prices may have already built in that possibility.

China still dominates

So rather than a recession creating bad news for stocks, it could have the opposite effect as investors begin to look past the expected bad news and look ahead to a recovery, especially as China’s economy keeps growing.

In short, when reading the headlines, it’s hard to look past them. But if you take a moment to think things through, you can start to look past the report’s surface, and instead focus more on the consequences of the news.

The consequences of a poor near-term outlook are likely to mean interest rates stay lower than most people think, and that should mean good news for stocks.

Cheers,

Kris+

PS: You can quiz me on my bullish stock market views in person at the upcoming World War D conference in Melbourne at the end of next month. I’ll be on the stage with global finance gurus Dr Marc Faber, Jim Rickards, and Satyajit Das. You can find out more here about what I consider to be the best money and finance conference in Australia this year. Click here for the revealing trailer…

GBPUSD moves sideways between 1.6582 and 1.6730

GBPUSD moves sideways in a trading range between 1.6582 and 1.6730. Support is at 1.6582, a breakdown below this level will confirm that the uptrend from 1.6252 had completed at 1.6822 already, then deeper decline to 1.6400 area could be seen. Resistance is at 1.6730, above this level will signal resumption of the uptrend from 1.6252, then the following upward movement could bring price to 1.7000 zone.

Provided by ForexCycle.com

The Importance of Buying Stocks at the Right Price

Think to yourself – have you ever made an investment loss which you could have sold for a profit?

If you answered yes to this question, you’re not alone. 99.9% of investors have done the same thing.

Even the best investors make mistakes. But they’re successful because they learn from their mistakes.

One of my investment mentors said to me, ‘it’s the absence of big losses, not the big gains, that makes an investor truly successful‘.

This quote transformed my life as an investment analyst.

It made me truly understand the importance of capital preservation. I then became obsessed with understanding the true risks behind each company.

I can assure you that 99% of investors don’t understand the real concept of risk (even after they lose money). This is why many people continue to repeat their mistakes as they spend all their time thinking about the reward, and rarely think about the risks.

Well, I take protecting your capital seriously. My goal as resource analyst for Diggers & Drillers is two-fold: 1) Helping my readers make money and; 2) Helping them protect their capital.

In fact this is what Diggers & Drillers investment director Kris Sayce wrote in a previous weekly update:

‘Let me address one point made by subscriber John where he wrote, ‘OK [the previous] recommendations mainly fell over but it was due to being a victim of the times.’

‘John may be fine with stocks that turn into losers, but I’m not. While it’s impossible to pick a winner every time, we’re not happy with the idea that investors should be ‘victims of the times’.‘

Too many analysts and investment advisors take that view. They lap up the praise when a stock idea goes well, and then claim they are a ‘victim of the times’ when a stock idea goes bad.

There are plenty of great investors who have blown themselves up by not properly considering the risks.

Look at Jesse Livermore; he could have been one of the greatest investors of all time (some even argue that he is). Livermore started with nothing and by 1929 had an estimated net worth of US$100 million (or over one billion dollars in today’s value)…before going on to losing it all due to ignoring his risk principles.

Stock markets are volatile. Prices can quickly rise and fall. As a result, we publish what we call a ‘buy-up to price’ with each recommendation in Diggers & Drillers. I take the buy-up-to price seriously, and so should you.

A buy-up-to price is similar to what Warren Buffett calls his ‘margin of safety’.

A ‘margin of safety’ is a share price that an investor should pay which is significantly below its intrinsic value. This will minimise the risk of investment losses and maximise the opportunity for gains.

The ‘buy-up-to price’ isn’t a randomly selected share price. From the hours of research I spend analysing stock recommendations, I attempt to comprehensively understand the investment risks.

As such, the buy-up-to price reflects the maximum price you should pay for taking on the level of investment risk.

Let me briefly explain my thought process when recommending the buy-up-to price.

In the February issue of Diggers and Drillers, I recommended a small-cap energy company. In the report I flagged the key risks investors should keep in mind before buying the stock.

At the time of recommending the stock, with the share price closing at a few cents, I set a buy-up-to price slightly higher.

Considering the risk for reward, this was the margin of safety I recommended readers buy in at. But the share price shot higher overnight and, based on that price, the risk far outweighed the reward.

Sure, possible future events could double the stock’s share price, but equally readers could lose up to 50% of their investment if nothing happens. And if readers bought at the higher price (which none should have done, following my buy-up-to price), which is more than 20% above my suggested maximum buy price, they’ve just increasing their risk.

For readers to invest in this new recommendation on the off chance that it dips to or below the maximum buy price, one option is to set a limit order at or below the buy-up-to price. Online share trading platform will give easy instructions for placing limit orders.

Considering the high volume and share price rally, I wouldn’t be surprised if the share price did fall below the maximum buy-up-to price. That little bit of patience could make a huge difference in protecting investor’s capital.

I hope that makes things clear and that you understand the importance of buy-up-to prices. It’s a strategy that Kris implemented nearly four years ago in Australian Small-Cap Investigator, and they have worked to good effect to make sure you don’t overpay for a stock.

Next week I will discuss some of the investment strategies for the Diggers and Drillers buy list, such as knowing when to sell, an important part of any investor’s strategy that is often overlooked.

Jason Stevenson+

Contributing Editor, Money Morning

Ed note: The above article is an edited extract from Diggers and Drillers.